Key Takeaways

A handful of misfits saw the 2008 crash coming and bet the house

The 2008 financial collapse was foreseeable, yet almost no one foresaw it. Michael Lewis tells the story through a small band of outsiders, fewer than twenty people worldwide, who spotted the rot in subprime mortgages and bet against the entire system. Among them: Steve Eisman, a caustic hedge fund manager who saw finance as a moral crusade; Michael Burry, a one-eyed doctor with Asperger's who read bond prospectuses no one else read; and three amateurs running Cornwall Capital from a Berkeley garage with $110,000.

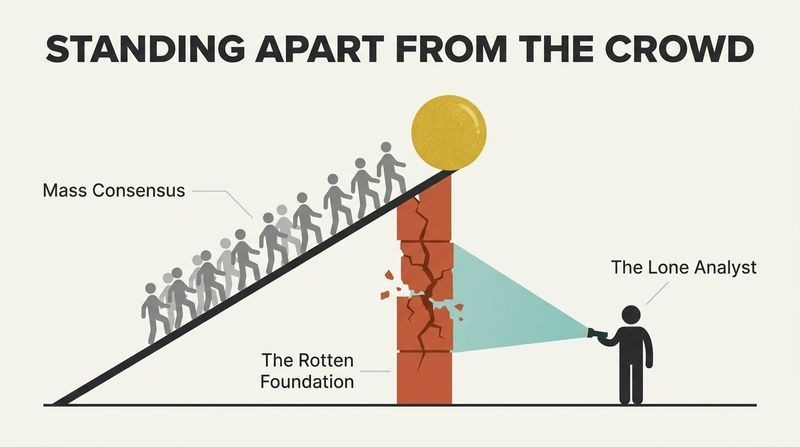

What unites them is that they were all, in Lewis's telling, deeply strange. Being right required standing apart from mass hysteria, believing most financial news was wrong, and most important people either lying or deluded, without going insane.

What's striking is the epistemology here: the crash was not hidden, it was public information nobody bothered to read. This echoes research on "information avoidance" in behavioral economics, where people actively steer away from data that threatens comfortable beliefs. Lewis frames outsider status as an analytical asset, resonant with Thomas Kuhn's observation that paradigm shifts usually come from the margins. The selection bias caveat matters, though: for every prescient contrarian, countless others bet against booms and were wrong. Survivorship makes genius look inevitable in hindsight. The real lesson is structural, not heroic: a system this opaque guaranteed someone, somewhere, would eventually find the flaw.

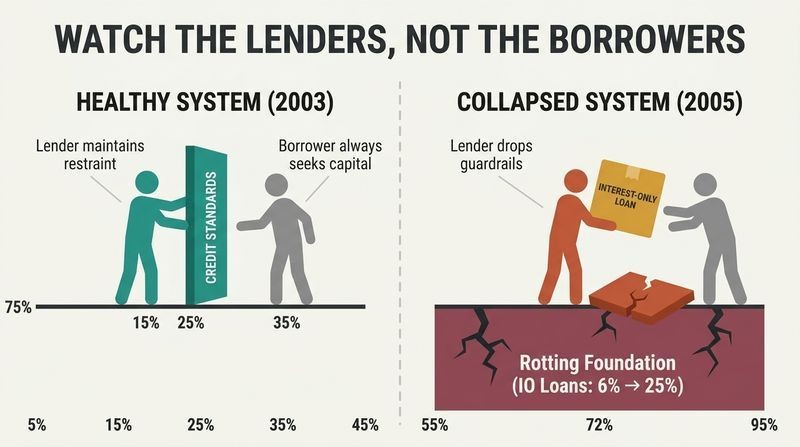

Watch the lenders, not the borrowers, when credit standards collapse

Michael Burry's core insight was that borrowers will always grab a good deal for themselves. Restraint is the lender's job, and when lenders lose it, disaster follows. By 2003 borrowers had clearly lost discipline. By 2005 lenders had too. Burry tracked the decline by reading actual mortgage bond prospectuses, noticing that interest-only adjustable-rate loans jumped from under 6% of a pool in early 2004 to over 25% by late 2005, even as average credit scores stayed flat. The pools were rotting while the surface metrics looked stable.

The worst product was the interest-only negative-amortizing adjustable-rate mortgage, where a borrower could pay nothing and watch their debt grow. Only someone with no income would want it. The question was why anyone would lend it.

Burry's maxim inverts the usual moral framing of the crisis, which blamed reckless homeowners. Placing responsibility on lenders aligns with the economics of moral hazard: when originators sold loans off immediately, they bore none of the default risk, so prudence became irrational. This is the agency problem in pure form. The deeper point extends beyond finance: in any system, watch the party with the power to say no. When gatekeepers stop gatekeeping (whether banks, auditors, or regulators) the incentive structure has already failed. Burry's edge was not prophecy but literacy. He simply did the credit analysis that should have happened before the loans were made.

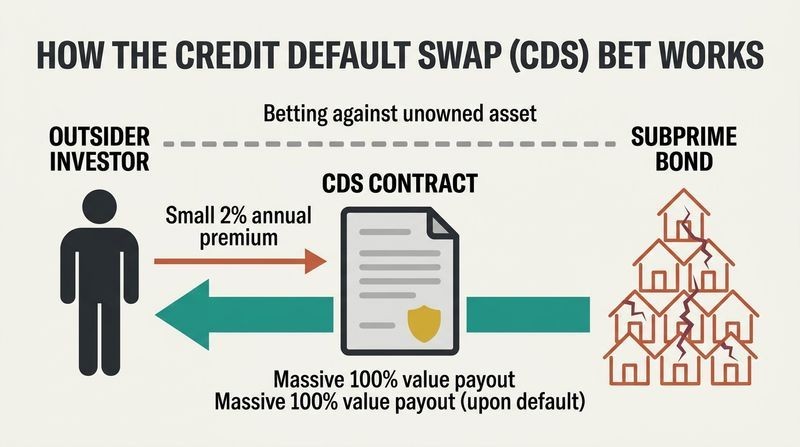

The credit default swap let outsiders bet against bonds they didn't own

You cannot short a house, and subprime bonds were too small and scattered to borrow and sell short. Burry's breakthrough in 2005 was realizing a credit default swap (CDS) could solve this. A CDS is essentially an insurance policy on a bond: you pay a small annual premium, say 2%, and if the bond defaults, you collect its full value. Your loss is capped at the premiums; your gain can be many multiples.

This solved the timing problem too. Subprime loans carried teaser rates fixed for two years before resetting sharply higher, so defaults would spike around 2007. A CDS let Burry lay his bet in 2005 and simply wait. He pestered Wall Street firms until Deutsche Bank and Goldman Sachs created the contracts, then bought over a billion dollars' worth.

The CDS is the pivotal instrument of the whole saga, and its asymmetry (limited downside, enormous upside) is what made the trade irresistible to contrarians. It resembles a lottery ticket priced by people who misjudged the odds. What's underappreciated is how the instrument's very existence changed the market it described: because CDS supply was theoretically infinite, bets could dwarf the underlying loans. This is the difference between insurance and gambling that regulators failed to grasp. Nassim Taleb's work on convex payoffs illuminates why such asymmetric bets are so powerful when tail risk is systematically underpriced, and why markets so rarely offer them at fair value.

The CDO was a machine for turning junk bonds into gold-rated ones

When Wall Street ran out of subprime bonds to sell, it invented the collateralized debt obligation (CDO). Take a hundred of the riskiest triple-B-rated slices of different mortgage bonds, pile them into a new tower, and persuade the rating agencies that this repackaged junk was a diversified portfolio. Roughly 80% of that new tower would then be blessed as triple-A, supposedly as safe as US Treasuries. Lewis calls it a machine that turned lead into gold, or a credit-laundering service.

The logic was absurd. All hundred bonds sat on the same economic floodplain. If subprime loans in Florida went bad, so would those in California, for the same reasons at the same time. The claimed diversification was fiction. A mere 7% loss in the underlying loans could wipe out the entire CDO.

The CDO exemplifies how complexity becomes a weapon. Lewis's insight that opacity is profitable inverts the standard defense of financial innovation as efficiency-enhancing. Here innovation deliberately manufactured confusion so trading desks could extract fees from the argument over value. The correlation error at the heart of it (assuming subprime pools were independent when they were nearly identical) is a failure Gaussian copula models made mathematically respectable. Felix Salmon later called that formula the one that killed Wall Street. The broader lesson transcends finance: when a product's complexity exceeds anyone's ability to price it, the complexity itself is the fraud, whether or not any law was broken.

Rating agencies rubber-stamped garbage because issuers paid their fees

The whole edifice rested on Moody's and Standard & Poor's, and Eisman discovered they were the weakest link. Their employees were underpaid nine-to-fivers, the ones who could not get Wall Street jobs. Crucially, they were paid by the very banks whose bonds they rated, creating a race to the bottom: demand real data, and the bank takes its business to the competitor. When Eisman asked what happened to defaults if home prices fell, S&P's model could not even accept a negative number.

Wall Street trading desks openly gamed the models. They learned the agencies used a pool's average credit score, so they mixed hopeless borrowers with immigrants who had high "thin-file" scores (short credit histories) to hit the magic average of 615 and maximize triple-A output.

The issuer-pays model is a textbook conflict of interest, and its persistence reveals regulatory capture. What's remarkable is not corruption but institutional mediocrity: the agencies were not evil masterminds but outgunned functionaries. This maps onto Hannah Arendt's banality-of-evil framing, where catastrophe emerges from thoughtlessness rather than villainy. Eisman's frustration that the prestige hierarchy was inverted (a Moody's downgrade moves markets, yet analysts flee to the banks they rate) points to a genuine design flaw in capitalism's information infrastructure. Post-crisis reforms like Dodd-Frank attempted fixes, but the fundamental payment structure survived largely intact, suggesting the incentive problem is more durable than any single scandal.

Incentives beat intelligence: smart people do dumb things when paid to

Michael Burry built his investment philosophy on Charlie Munger's talk about the power of incentives, illustrated by cases like ophthalmologists rediscovering a risky eye surgery only after Medicare slashed cataract reimbursements. Burry saw the same force everywhere, so he structured his fund, Scion Capital, to charge only expenses rather than the standard 2% management fee. He ate only if his investors made money.

The subprime machine ran on perverse incentives at every link. Loan originators sold loans off instantly, so default risk was not theirs. CDO managers like Wing Chau were paid on volume, not performance, so a bad CDO paid as well as a good one. Traders booked years of future profit up front. Everyone in the chain got rich making decisions that would eventually detonate.

Munger's dictum (show me the incentive and I'll show you the outcome) is the book's quiet organizing principle. It reframes the crisis from a story of greed, which is constant, to one of misaligned incentives, which are designable. This is the economist's rejoinder to moralizing: you cannot legislate virtue, but you can restructure payoffs. The originate-and-sell model severed the feedback loop between decision and consequence, the same failure behind many organizational disasters, from Boeing to Enron. The uncomfortable extension is that most of us respond to incentives more than we admit, and self-serving justification follows automatically. Burry's fee structure was a rare act of deliberately aligning his interests against his own convenience.

Turning partnerships into public companies made Wall Street reckless

In Lewis's epilogue, he traces the whole disaster back to one structural change: the transformation of Wall Street partnerships into public corporations, which his old boss John Gutfreund pioneered at Salomon Brothers in 1981. When partners gambled their own money, they showed restraint. Once firms went public, the ultimate risk shifted to shareholders who had no idea what the traders were doing, and eventually to taxpayers.

Lewis argues no partnership would have leveraged itself 35 to 1, held $50 billion in toxic CDOs, or gamed the rating agencies, because the long-term expected loss would never justify the short-term gain. Public ownership turned each firm into a black box built on blind faith rather than trust, where a few proprietary traders could generate more than the entire firm's profits, meaning everyone else lost money.

This is Lewis's deepest structural claim, and it doubles as a theory of institutional accountability. When decision-makers are insulated from the consequences of their bets, prudence evaporates, an application of the "skin in the game" principle Nassim Taleb would later formalize. The partnership model imposed unlimited personal liability, the ultimate feedback mechanism. Its abandonment socialized risk while privatizing reward, precisely the pattern that culminated in taxpayer bailouts. One nuance worth noting: public capital also fueled the liquidity and scale that made modern markets function, so the reform is not costless. But Lewis's core point stands, that ownership structure quietly shapes behavior more than any compliance manual ever could.

Wall Street synthesized fake loans because demand outran real borrowers

Eisman's epiphany came at a Las Vegas dinner beside Wing Chau, a CDO manager who bought the riskiest slices Eisman was betting against. When Chau said he loved short-sellers because "without you I don't have anything to buy," Eisman finally understood the machine. There were not enough real Americans with bad credit to satisfy investor appetite, so Wall Street used credit default swaps to synthesize copies of the worst bonds, replicating them a hundred times over.

This is why the losses dwarfed the actual subprime loans. A single Long Beach Savings bond could be referenced by countless synthetic CDOs. The real home loans existed, Lewis writes, mainly so their fate could be gambled upon. The side bets became bigger than the thing itself, multiplying the systemic damage far beyond the original mortgages.

The synthetic CDO is where the story turns from mispricing to something closer to systemic sabotage. Lewis's fantasy-football analogy is apt: drafting a player does not create a second real player, but a synthetic bond did create real losses out of thin air. This decoupling of financial claims from underlying assets is the essence of what makes derivatives systemically dangerous, amplifying rather than distributing risk. It connects to Hyman Minsky's financial instability hypothesis, where stability breeds ever more speculative structures until collapse. The moral vertigo Eisman experiences (realizing his own bets fed the monster) captures a genuine ethical trap: opposing a corrupt system can inadvertently sustain it.

The biggest loss in Wall Street history came from betting on safety

Howie Hubler, Morgan Stanley's star bond trader, correctly bet against risky triple-B subprime bonds. But to finance the premiums, he sold insurance on $16 billion of "safe" triple-A CDOs, collecting tiny premiums he considered free money. He assumed some subprime bonds would fail but not all. He was wrong. Because the underlying bonds were nearly identical, their correlation was not the 30% the rating agencies assumed but effectively 100%. When one collapsed, all collapsed.

Hubler lost roughly $9 billion, the single largest trading loss in Wall Street history. His firm's risk reports had filed his $16 billion bet under "triple-A," as if it were Treasury bonds. CEO John Mack never once sat down with him. Hubler resigned and kept his tens of millions in earlier bonuses.

Hubler's story is the crisis in miniature: complexity so great that the traders deceived themselves, not just customers. The correlation blunder is the mathematical heart of the whole collapse, and it recurs across risk management failures because tail events cluster in ways historical data cannot capture. Morgan Stanley's value-at-risk model, which weighted recent placid price movements, literally could not see the risk, an indictment of backward-looking quantitative tools that Taleb's black-swan critique anticipated. What lingers is the accountability vacuum: the man responsible for history's largest trading loss walked away rich. That asymmetry, private gains and socialized losses, is the book's enduring indictment of the incentive structure.

When you win by betting the system fails, victory feels like grief

Being right brought the short-sellers little joy. Eisman compared 2008 to being Noah on the ark: safe, but staring out at a flood drowning everyone. In 2007 he had enjoyed shorting "bad guys"; in 2008 the entire financial system was at risk, and no one wants that. Danny Moses, FrontPoint's head trader, suffered what felt like a heart attack on September 18, 2008, as markets froze, echoing the panic attacks he had after fleeing the World Trade Center on 9/11.

Michael Burry, who doubled his investors' money, received no thanks, only silence and lawsuits. He discovered he had Asperger's syndrome, which explained his ability to read prospectuses no one else would. Vindicated and rich, he felt something vital had died inside him, and he shut down his fund.

The emotional aftermath complicates the triumphalist narrative of the clever contrarian. Winning a zero-sum bet against systemic collapse produces survivor's guilt, not celebration, a psychological reality often absent from finance writing. Burry's Asperger's diagnosis reframes his edge as neurodivergence: his obsessive focus and immunity to social consensus were precisely what let him see what herd-driven peers could not. This resonates with growing recognition that cognitive diversity strengthens group decision-making, and that markets punish the very independence they occasionally reward. The bleaker truth is that the winners and losers alike ended rich, and taxpayers absorbed the flood, which is why moral clarity dissolved even for those who were right.

Analysis

The Big Short belongs to a rare genre: the forensic thriller that doubles as economic pedagogy. Lewis's structural achievement is teaching readers exotic instruments (credit default swaps, CDOs, synthetic CDOs) by embedding them in the psychologies of eccentric protagonists, so the finance becomes character-driven drama. This is his signature move, perfected in Liar's Poker and Moneyball: find the outsiders who saw what insiders missed, and let their strangeness illuminate a system's blindness.

The book's central argument is that the 2008 crisis was not a bolt from the blue but the predictable product of misaligned incentives layered atop willful complexity. Every link in the chain (originators, banks, rating agencies, CDO managers, regulators) was paid to not understand what it was doing. Lewis's most provocative and least-discussed thesis appears in the epilogue: the root cause was the 1980s conversion of Wall Street partnerships into public corporations, which transferred risk from those making decisions to shareholders and ultimately taxpayers. This structural diagnosis is more durable than the moralizing about greed that dominated post-crisis discourse.

The book's limitations are worth naming. Its heroes are selected by outcome, so their genius may be partly survivorship bias; the countless contrarians who bet wrong go unmentioned. Lewis is more storyteller than systems analyst, and readers seeking policy prescriptions or macroeconomic rigor will find gaps. Gillian Tett's Fool's Gold and the Financial Crisis Inquiry Report offer more institutional depth.

Yet the enduring value is epistemological. The crisis was hidden in plain sight, documented in prospectuses available for a hundred dollars a year that virtually no one read. Lewis's deepest lesson is not about mortgages but about knowledge itself: complexity functions as camouflage, incentives corrupt cognition, and the capacity to stand apart from consensus, however socially costly, is the rarest and most valuable trait in any market or institution.

Review Summary

The Big Short exposes the 2008 financial crisis through the stories of investors who foresaw and profited from it. Lewis skillfully explains complex financial concepts, revealing how greed, ignorance, and flawed incentives led to the subprime mortgage collapse. Readers praised the book's engaging narrative and clear explanations, though some criticized its focus on those who profited. The book highlights systemic issues in the financial industry and raises questions about whether enough has changed to prevent future crises.

People Also Read

Glossary

Credit Default Swap (CDS)

Insurance policy on a bondA contract functioning as insurance on a bond. The buyer pays a small annual premium, and if the underlying bond defaults, the seller pays the buyer its full value. It allowed investors like Michael Burry to bet against subprime mortgage bonds they did not own, with losses capped at premiums and gains potentially many times larger.

Collateralized Debt Obligation (CDO)

Repackaged tower of risky bondsA security built by pooling around a hundred of the riskiest triple-B slices of different mortgage bonds into a new tower, then persuading rating agencies to rate roughly 80% of it triple-A. Lewis describes it as a machine that laundered junk into apparent gold, hiding risk through complexity rather than reducing it.

Synthetic CDO

CDO made of credit swapsA CDO composed not of actual mortgage bonds but of credit default swaps referencing them. Because swaps could be created without limit, synthetic CDOs replicated the worst bonds many times over, multiplying systemic losses far beyond the value of the real underlying home loans.

Tranche

Risk-ranked floor of bondsA layer within a mortgage bond or CDO, imagined as a floor in a tower. Lower floors (triple-B, the mezzanine) absorb the first losses but pay higher interest; upper floors (triple-A) pay less but were considered safest. Investors chose which floor of risk to occupy.

Thin-file FICO score

High score, short credit historyA credit score based on a brief borrowing history. Immigrants who had never defaulted because they had never borrowed often had surprisingly high thin-file scores. Wall Street exploited this to raise a loan pool's average score to the target of 615, maximizing the triple-A bonds it could produce.

Originate and sell model

Make loans, sell risk offA lending approach where firms made mortgage loans then immediately sold them to Wall Street banks for packaging into bonds. Because originators kept none of the default risk, they had no incentive to lend responsibly, creating the moral hazard at the heart of the subprime boom.

Ick investing

Buying stocks that repel investorsMichael Burry's term for taking a special analytical interest in stocks that provoke an instinctive negative reaction. He hunted unusual situations, often court rulings or scandals, that scared off other investors and thus created mispriced opportunities, as with the Avant! Corporation.

FAQ

What's The Big Short about?

- Focus on 2008 crisis: The Big Short by Michael Lewis explores the events leading up to the 2008 financial crisis, with a particular focus on the housing market and subprime mortgage crisis.

- Key players profiled: It highlights the stories of investors like Michael Burry, Steve Eisman, and Greg Lippmann, who foresaw the collapse and bet against the housing market.

- Complex financial instruments: The book explains complex financial products such as mortgage-backed securities, collateralized debt obligations (CDOs), and credit default swaps (CDS).

Why should I read The Big Short by Michael Lewis?

- Insight into financial systems: The book offers a critical examination of the financial systems and the greed and ignorance that led to the crisis.

- Engaging storytelling: Michael Lewis uses a narrative style that combines humor and drama, making complex financial topics engaging and relatable.

- Understanding risk and accountability: It encourages readers to think critically about risk, accountability, and the consequences of financial decisions.

What are the key takeaways of The Big Short?

- Importance of skepticism: The book emphasizes the need for skepticism in financial markets, as many investors failed to question the assumptions underlying the housing boom.

- Consequences of greed: It illustrates how greed and a lack of regulation led to widespread financial malpractice, resulting in a global economic crisis.

- Value of independent analysis: The success of characters like Michael Burry highlights the importance of conducting independent analysis rather than relying solely on market consensus.

What are the best quotes from The Big Short and what do they mean?

- “How can a guy who can't speak English lie?” This quote reflects the absurdity of the financial system, where complex instruments were sold without proper understanding.

- “The market can remain irrational longer than you can remain solvent.” This underscores the risks of betting against the market; even if correct, it may take time for the market to reflect reality.

- “The truth is, the financial system is a lot more fragile than we think.” This serves as a warning about the inherent vulnerabilities in financial systems.

Who are the main characters in The Big Short?

- Michael Burry: A hedge fund manager who predicted the housing market collapse and invested in credit default swaps to profit from it.

- Steve Eisman: An outspoken investor who recognized the flaws in the subprime mortgage market and sought to expose the corruption within it.

- Greg Lippmann: A Deutsche Bank trader who played a crucial role in developing the market for credit default swaps.

What are mortgage-backed securities (MBS) in The Big Short?

- Definition of MBS: Mortgage-backed securities are financial instruments created by pooling home loans and selling shares in that pool to investors.

- Risk and return: Investors receive payments based on the cash flows from the underlying mortgages but also take on the risk of borrower defaults.

- Role in the crisis: The proliferation of MBS, especially those backed by subprime loans, significantly contributed to the financial crisis.

What are collateralized debt obligations (CDOs) in The Big Short?

- Definition of CDOs: CDOs are complex financial products that pool various types of debt, including mortgage-backed securities, and slice them into tranches with different risk levels.

- Tranche structure: Tranches are rated based on risk, with senior tranches receiving higher ratings and lower interest rates, while junior tranches carry higher risk.

- Impact on the crisis: Many CDOs were composed of subprime mortgage-backed securities, and when defaults rose, the entire structure collapsed.

How did the rating agencies contribute to the crisis in The Big Short?

- Flawed rating models: Agencies like Moody's and S&P used models that failed to accurately assess the risk of subprime mortgage-backed securities.

- Conflict of interest: The agencies were paid by the firms whose products they rated, compromising their objectivity.

- Consequences of misrating: Overrating risky securities led to massive investments in subprime mortgages, resulting in significant financial losses.

What is a credit default swap (CDS) in The Big Short?

- Definition of CDS: A credit default swap is a financial derivative that allows an investor to transfer the credit risk of a borrower to another party.

- Mechanics of CDS: The buyer pays a premium to the seller, who compensates the buyer in the event of a default on the underlying debt.

- Role in the crisis: CDS became a tool for speculating against the housing market, allowing investors to profit from the collapse of subprime mortgages.

How did the financial crisis affect ordinary Americans, according to The Big Short?

- Widespread foreclosures: The housing market collapse led to millions of foreclosures, displacing families and causing financial hardship.

- Economic recession: The crisis triggered a global recession, resulting in job losses and reduced consumer spending.

- Loss of trust: The crisis eroded public trust in financial institutions, leading to calls for reform and greater oversight.

How did the characters in The Big Short react to the unfolding crisis?

- Skepticism and anger: Characters like Eisman and Burry expressed skepticism and anger towards the financial system, feeling ignored.

- Profit from the collapse: Those who recognized the crisis, such as the Cornwall Capital team, took positions that allowed them to profit.

- Moral dilemma: Some grappled with the moral implications of profiting from a disaster that caused widespread suffering.

What lessons can be learned from The Big Short by Michael Lewis?

- Need for regulation: The book highlights the importance of regulatory oversight in preventing financial crises and protecting consumers.

- Value of critical thinking: It encourages questioning prevailing narratives in financial markets and conducting independent research.

- Awareness of systemic risks: The book serves as a reminder of the interconnectedness of financial systems and potential systemic risks.

About the Author

Other books by Michael Lewis

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.