Key Takeaways

You can buy real estate with no cash, credit, or credentials

Creative finance is the whole game. Pace Morby grew up third of twelve kids, moved 26 times before age 19, and watched his self-employed dad quietly use seller financing just to keep a roof overhead, never to build wealth. Morby flipped 7,000 houses as a contractor before realizing he was a service provider, not an investor. Once he learned creative finance, he never used his own money or credit again, eventually transacting over $250 million and acquiring 1,000-plus doors.

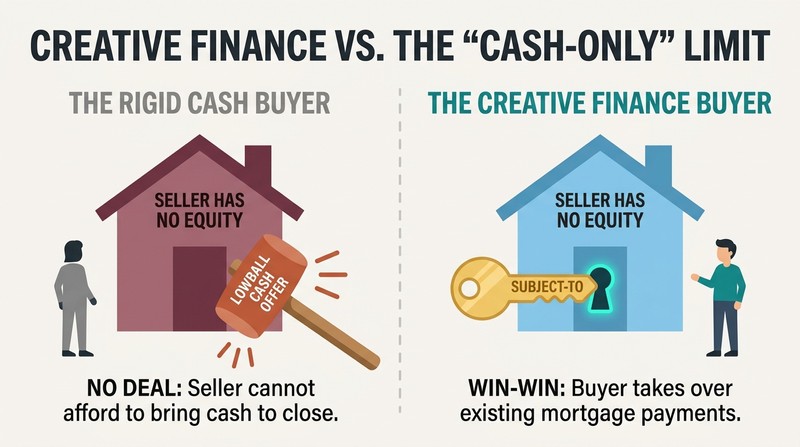

The three ways to make money in real estate are wholesale, fix-and-flip, and buy-and-hold. Creative finance amplifies all three because you can solve problems cash buyers cannot. Instead of arriving with a lowball cash offer (a hammer looking for nails), you carry a full toolkit of structures that fit each seller's situation.

What's striking is how this reframes the barrier to entry. Traditional gurus echo Dave Ramsey: save, qualify, buy with cash. Morby inverts it, arguing the bank-and-Realtor system is an optional middleman. The claim has real grounding (assumable loans and seller carrybacks are centuries old), but readers should note the asymmetry: these tools shine in specific conditions like low-rate existing mortgages and motivated sellers. The promise of zero-down deals is real but rarer than the YouTube highlight reel suggests, a caveat Morby himself flags.

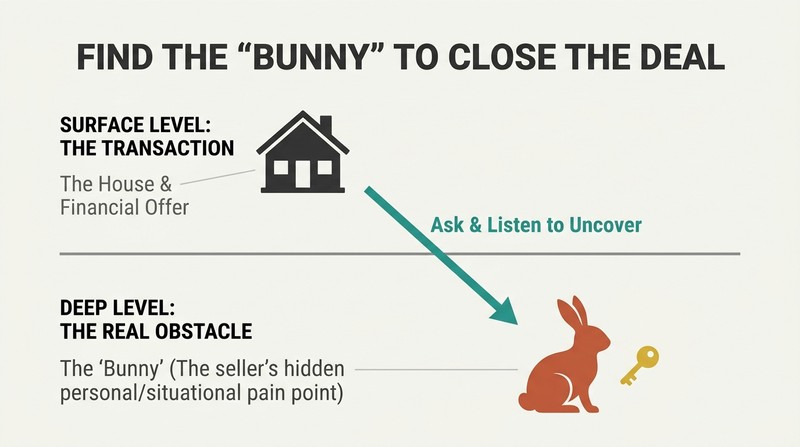

Find the bunnies: it's never about the house, always the person

Solve the hidden problem and the deal follows. On his first lead, Morby met Janney, a retired teacher with a $165,000 offer already in hand. He couldn't beat it, so he simply asked if he could help with anything. Her real obstacle? Three giant Flemish rabbits she couldn't rehome. Morby called his mom, who hauled them to her farm. Two weeks later Janney sold to him at his lower number, $150,000, because he was the only buyer who listened.

Every seller has a 'bunny,' an emotional or situational pain point that determines who they sell to and on what terms. A reason (I want to move) is surface level. The bunny is the deeper situation driving the decision. Your job is detective work: ask enough questions to uncover it, then re-home their problem.

This is the book's emotional core, and it aligns with negotiation research from Chris Voss and Stuart Diamond, who argue that perceived empathy and discovering the counterpart's true motivation outperform aggressive price anchoring. Morby's anecdote also illustrates the endowment effect: sellers value their homes beyond market logic because of memory and identity. The risk is performative empathy curdling into manipulation, a line Morby walks by genuinely solving problems. Used sincerely, the bunny hunt converts adversarial haggling into collaborative problem-solving, which is why he closes when others walk.

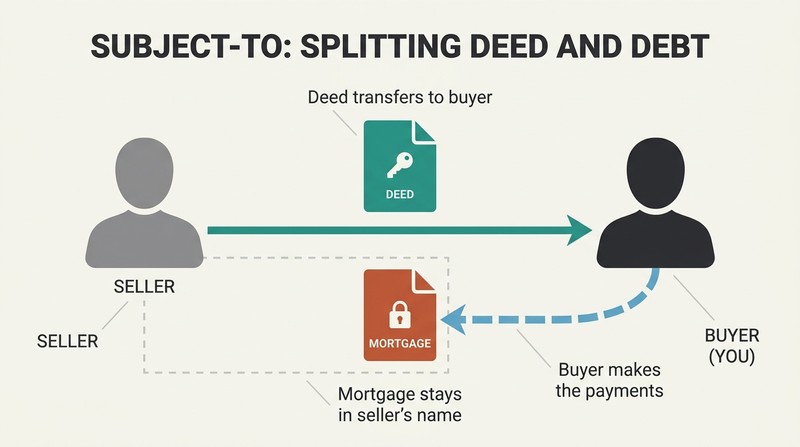

Subject-to lets you take over a mortgage without bank approval

Subject-to means buying subject to the existing financing. Rather than paying off the seller's loan, you take over their monthly payments while the mortgage stays in their name and the deed (ownership) transfers to you. An escrow officer named Eileen Brown taught Morby this after he kept disqualifying sellers with no equity. Suddenly the leads he was trashing became gold.

Ownership and debt are not the same thing. Morby uses a grocery analogy: when you swipe a credit card at the store, you own the food (you have the receipt) even though the bank fronted the money. In real estate, the deed is your receipt and the mortgage is the debt. To structure a sub-to deal: confirm the loan terms, calculate equity, choose your exit, cover any arrears, decide how much cash to hand the seller, and have an attorney paper it.

Subject-to is powerful and genuinely underused, but it carries the book's biggest hidden risk: the due-on-sale clause, which lets the lender demand full repayment when title transfers. Morby addresses mitigation through proper insurance handling and trusts, yet readers should weigh this seriously, especially in rising-rate environments where lenders have more incentive to call loans. The strategy also leaves the seller's credit tied to a stranger's payment discipline. Done with airtight servicing and documentation, it works; done sloppily, it can harm both parties.

Offer more, not less, when a seller will take payments

The F-150 story unlocks seller financing. Morby's beloved truck had 320,000 miles and a $5,000 Blue Book value. Listed on Craigslist for $10,000, it drew zero calls. His wife suggested adding three words: 'will take payments.' He was flooded with offers and sold it for $12,500. Lesson: buyers who can't pay a lump sum can pay monthly, and they'll pay a premium for the privilege.

With seller financing, the seller becomes the bank. Morby tells sellers, 'You get the price you want, I get the terms I need.' He once offered $40,000 over asking on a deal because at $0 down and 0% interest, structured over decades, the property would net roughly $1,000 a month and close to $1 million in lifetime profit. The math favors monthly cash flow over upfront cost.

The F-150 parable is brilliant teaching because it ports a complex financial concept into a universal experience. Economically, it exploits the spread between sale price and present value: paying more nominal dollars spread over time, at low or zero interest, can cost less in real terms once inflation and cash flow are factored in. This is the same logic dealerships use to sell cars on monthly payment rather than sticker price. The caution: paying above market only pencils out if the terms (rate, length, down payment) are genuinely favorable, so the storytelling must never substitute for underwriting.

Walk sellers backward to their real net to turn no into yes

Most sellers fixate on a price, not their walkaway money. When Morby called Marvin, a golfer whose wife had Alzheimer's, Marvin first said he wasn't interested in terms, then named $240,000. Morby never argued. He gently walked Marvin through commissions (around 6%), closing costs, and other fees, showing that listing traditionally would leave roughly $220,000 in his pocket, money that would then sit in a bank earning almost nothing while inflation eroded it. By contrast, seller financing at the full $270,000 with interest made Marvin an investor earning monthly income.

Ignore the first objection and educate instead. Morby's anchoring move is letting the seller talk himself down to the disappointing cash number, then presenting terms as the obvious upgrade. As he puts it, a man convinced against his will holds the same opinion still, so you guide rather than argue.

This is consultative selling at its finest, mirroring the SPIN selling method where you surface the cost of the status quo before presenting your solution. The walkaway-money reframe is also behavioral economics in action: sellers anchor on gross list price and ignore transaction friction, a form of mental accounting error. Morby weaponizes that gap honestly by making the invisible visible. The ethical strength here is that the seller often genuinely nets more; the danger is that the same techniques could pressure vulnerable sellers, which is why his emphasis on serving over closing matters.

Take the next step, not every step; learn by closing deals

Action beats information. Both of Morby's mentors refused to give him a full education. Bethany Willis fed him just enough to make his first call, then his next. Eileen Brown told him not to phone her with hypotheticals, only real deals: go create problems, and I'll solve them. He compares it to baseball, where skill comes from at-bats, not from watching YouTube. You strike out more than you hit, and that's the game.

You don't need to know the whole staircase, just the next stair. Morby warns against 'ask-holes' who collect answers but never act, and prescribes a two-questions-per-day limit: ask, apply, make mistakes, repeat. He notes you have no real data on yourself until you've done something 91 days straight, and your first deal might land on day one or day 1,002.

This maps cleanly onto modern learning science: deliberate practice and just-in-time learning outperform front-loaded theory because skills consolidate through retrieval and feedback, not passive consumption. Entrepreneurship research (Saras Sarasvathy's effectuation) similarly shows successful founders act with available means and iterate rather than plan exhaustively. The 91-day figure is more motivational than empirical, but the underlying point is sound. The constructive caution: 'learn by doing' in real estate involves real financial and legal stakes, so the next-step philosophy works best paired with cheap, low-risk reps like door knocking before high-stakes contracts.

Make cash flow your North Star and match exits to your buy box

People buy real estate for five reasons: cash flow, depreciation (a tax deduction as the building ages, roughly 3.636% yearly over 27.5 years), appreciation, mortgage paydown by tenants, and leverage. Morby is a cash flow investor first: he wants more coming in than going out every month, then treats the other four as bonuses.

Your exit strategy must fit your personal buy box, not a generic ideal. Morby compares it to a restaurant menu and offers eight exits, including wholesale (assigning a contract for a fee), wraps (reselling a financed property at higher terms and pocketing the spread), lease options, sub-tail (buy sub-to then flip retail), rentals, group homes, vacation rentals, and corporate rentals. His rule: if you wouldn't happily own 1,000 versions of a deal, don't do even one. Buy where it's warm, where people relocate and renovate, and start local.

The five-reasons framework is standard real estate canon, but Morby's contribution is insisting on cash flow as the primary filter rather than speculative appreciation, a discipline that protects against downturns. His '1,000 versions' heuristic is an elegant decision rule borrowed from systems thinking: optimize for repeatability, not one-off wins. Worth noting is the tension he openly acknowledges, that lease options he once favored left appreciation on the table when markets surged. The honest lesson: no single exit is universally best, and matching strategy to temperament and local market beats chasing whatever worked for someone on social media.

The Morby Method cracks the big-down-payment objection

When a seller demands a huge down payment, blend two sources. The Morby Method combines a lender's money with a seller carryback. In a Florida deal, a seller named Bill insisted on $400,000 total and a 50% down payment because he needed $200,000 for his estranged daughter's wedding and a down payment on her first home, his way of finally showing up as a father. Rather than dismiss him as greedy, Morby got a $200,000 loan to cover the down payment and had Bill seller-finance the remaining $200,000.

The principle: a stubborn seller is usually protecting one tool to solve an emotional problem. Bill's equity was the single thing he'd done right in his life. Negotiating against that tool fails. Instead, you structure around it, often borrowing 70-80% from a lender and 20-30% from the seller so everyone wins.

The Morby Method is essentially layered financing, conceptually similar to mezzanine debt in commercial real estate where a senior loan and a junior seller note stack to fill a capital gap. Its ingenuity is psychological as much as financial: it converts an apparent dealbreaker into a structuring exercise. The recurring theme that sellers cling to equity because it represents identity or redemption is a genuinely fresh lens, echoing research on loss aversion and self-concept. The practical caveat is complexity: more parties and notes mean more documentation, more due-on-sale exposure, and more that can unravel in escrow.

Knock doors and harvest the dead leads everyone else trashes

Leads come from only five paths: direct to seller, direct to market or agent, referral partners, wholesalers' dead leads, and working for someone else. About 60% of Morby's deals come from dead leads, properties other investors disqualified because there was no equity or the seller wanted too much.

Door knocking is the cheapest, fastest, least-regulated channel. As carriers crack down on cold texts and calls, nobody can stop you from knocking, even on 'no solicitation' homes, because you're asking them to sell, not buy. The data: a rookie lands roughly one appointment per 50 doors, a veteran one per 25, and door-knocked deals net around $25,000 versus $13,000 to $15,000 from cold calls because in-person trust gives more negotiating room. Morby even found handwritten sticky notes pull twice the callbacks of slick printed door hangers.

The handwritten-note finding is a small gem confirmed by persuasion research: perceived effort and personalization increase response rates, the same reason handwritten envelopes get opened. The 'no solicitation' reframe is clever legal jujitsu, though its durability varies by municipality. What deserves scrutiny is the romanticized economics; door knocking trades money for time and emotional labor, and rejection rates near 98% per door filter out most people regardless of the payoff. Morby's deeper point holds: distribution and consistent lead flow, not deal-making genius, separate working investors from spectators.

Disarm a seller's six fears before they even voice them

Sellers ask the same questions, so answer them preemptively. Morby anticipates the six recurring fears: What if you stop paying? Is this even legal? What if the market crashes? What if you die? Can I buy it back? Can I rent it from you? His master safeguard is the performance deed, a document held at the title company that automatically returns the property to the seller within roughly 24 hours if a payment is missed, no lawsuit required.

Underwrite on cash flow, not value. When sellers fear another 2008, Morby explains he buys based on the rent a property produces, not its price, and rents historically rise even when values fall. He buys based on monthly numbers, layers in third-party stories as social proof, and writes every figure on a legal pad so the deal is transparent. Education, not persuasion, closes the deal.

Pre-empting objections is textbook inoculation theory from social psychology: raising and refuting a concern before the other party fully forms it reduces its persuasive power. The performance deed is the linchpin that makes sub-to ethically defensible, converting an abstract trust exercise into an enforceable safety net. The 'rents don't fall' claim is broadly supported by historical data but not absolute; certain markets saw rent softening during severe local shocks. Still, the discipline of underwriting to cash flow rather than speculative value is exactly what kept disciplined investors solvent through past crashes.

Split every deal three ways into a financial war chest

Allocate profits before you spend them. Morby's three-part system divides each deal's proceeds: pay yourself (living expenses), set aside marketing and overhead (employees, bills), and fund the war chest (emergencies, evictions, defaults). On a $10,000 assignment he might take $3,000 personally, reserve $3,000 for marketing, and bank $4,000 for reserves.

Target three months of payments plus repair reserves per property. If a property carries a $1,000 monthly payment, he wants roughly $3,000 plus $2,500 for minor renovations sitting in reserve before he relaxes. When a deal doesn't fully fund the war chest upfront, he builds it from monthly cash flow, siphoning a couple hundred dollars a month until it's whole. He warns new investors against blowing early profits on a Rolex or new car; structure the money first.

This is profit-first accounting applied to real estate, echoing Mike Michalowicz's principle that allocating money into purpose-specific accounts before spending prevents the cash-flow death spiral that kills undercapitalized operators. The reserve discipline is what lets Morby promise sellers he'll never miss a payment, which in turn makes the performance deed a theoretical rather than practical risk. The often-overlooked truth here is that creative finance's low entry cost can seduce beginners into overleveraging; reserves are the unglamorous infrastructure that converts a fragile portfolio into a durable one. Boring, essential, and frequently skipped.

Treat competitors as collaborators and lead with value first

Collaboration compounds faster than competition. Morby hangs out with rivals, swaps buyers and deals, and runs over sixteen income streams, partnering on nearly every one. His business partner Cody Barton won him over with a simple value-first pitch: I'll bring you leads, you close them, take the majority. That offer grew into a cold-call center, apps, and a wholesale business together.

Be a Go-Giver, not just a go-getter. Borrowing from Bob Burg and John David Mann's book, Morby insists service drives success in a relationship business. He gives away creative-finance knowledge that others sold behind $25,000 to $50,000 paywalls, and that generosity loops back as deals and partnerships. His operating questions when meeting someone new: What are you struggling with, and how can I help? In a 30-person mastermind, everyone's daily research becomes shared horsepower, a shortcut for all.

The collaboration thesis runs against the scarcity instinct most investors bring to a competitive market, and it's backed by network science: dense, generous networks generate more opportunity flow than guarded ones, because reciprocity and weak ties surface deals no individual could find alone. Adam Grant's research on 'givers' outperforming 'takers' over long horizons supports the claim directly. The realistic nuance Grant also found is that givers can be exploited without boundaries, so the model works best when paired with Morby's value-first filter that screens for people who reciprocate rather than merely extract.

Analysis

Wealth without Cash is a hybrid: part memoir, part tactical manual, part motivational sermon, structured around eighteen chapters that alternate between technique and investor case studies. Its genre is the creative-finance entrepreneurship book, and its distinctive move is welding cold mechanics (subject-to, seller carrybacks, performance deeds, the Morby Method) to a warm human thesis: real estate is a problem-solving and relationship business, not a transaction business. The recurring 'bunnies' metaphor is the connective tissue, and it elevates the book above the typical no-money-down genre that trades in hype.

The summarization challenge is density and repetition. Morby circles the same handful of structures from many angles, and the value lives in the accumulated case studies more than in any single framework. A faithful distillation must preserve the emotional logic (uncovering the seller's true situation) alongside the financial logic (underwriting to cash flow, structuring entry fees, choosing exits).

Intellectually, the book sits in an interesting tension with mainstream personal finance. Where Dave Ramsey preaches debt avoidance and cash purchases, Morby argues that leverage, when controlled and cash-flow-positive, is the engine of generational wealth. Both can be right for different risk profiles. The book's genuine blind spots are under-weighted: the due-on-sale clause is a structural risk that could cascade in a high-rate environment, and the seller whose credit and name stay attached to the loan bears asymmetric downside if the investor falters. Morby mitigates these with reserves, insurance, and documentation, but the YouTube-fueled zero-down fantasy he sells is rarer than his framing implies, a point he concedes in passing.

The most transferable ideas extend beyond real estate. 'Take the next step, not every step' is a sound philosophy for any skill acquisition. The walkaway-money reframe is consultative selling. The Go-Giver ethos is network science. Stripped of the niche tactics, the book is a case study in how empathy, action bias, and disciplined capital allocation convert into wealth, which is why it resonates with readers who will never knock a single door.

Review Summary

Wealth without Cash receives mostly positive reviews, praised for its insights on creative real estate financing. Readers appreciate the practical strategies, real-life examples, and Pace Morby's engaging storytelling. Many find it eye-opening and valuable for aspiring investors. Some criticize its focus on full-time investing, while others note occasional difficulty in comprehension. Overall, reviewers commend the book for its educational value, unconventional approach, and potential to create wealth through creative financing methods in real estate.

FAQ

What is Wealth without Cash by Pace Morby about?

- Creative finance focus: The book teaches how to invest in real estate using creative finance strategies like subject-to, seller financing, lease options, and hybrids, allowing investors to buy properties without cash, credit, or traditional bank loans.

- Mindset and legacy: Morby emphasizes the importance of mindset shifts, service, and accountability, framing real estate as a path to generational wealth and long-term financial freedom.

- Comprehensive guide: It covers everything from finding and evaluating deals to negotiating, legal considerations, exit strategies, and scaling a real estate business.

Why should I read Wealth without Cash by Pace Morby?

- Transparent, actionable advice: Morby is praised for his transparency and willingness to share replicable strategies for both beginners and experienced investors.

- Unlock hidden opportunities: The book reveals creative finance methods often kept behind paywalls, enabling readers to buy properties without traditional financing hurdles.

- Avoid costly mistakes: Real investor stories and lessons help readers sidestep common pitfalls and accelerate their learning curve.

What are the key takeaways from Wealth without Cash by Pace Morby?

- Creative finance unlocks deals: Using subject-to, seller financing, and other methods allows investors to solve more seller problems and close more deals.

- Action beats perfection: Morby stresses taking the next step rather than waiting to know every step, making it easier to start and learn as you go.

- Service and collaboration matter: Building trust, serving sellers’ needs, and collaborating with other investors are central to long-term success.

What is creative finance according to Wealth without Cash by Pace Morby?

- Alternative acquisition methods: Creative finance includes subject-to, seller financing, lease options, executory contracts, and hybrids, all designed to bypass traditional bank loans.

- Accessible to all: These methods require little to no cash, credit, or credentials, making real estate investing possible for almost anyone.

- Problem-solving toolkit: Creative finance gives investors more tools to solve seller problems and structure win-win deals.

What are the main creative finance strategies explained in Wealth without Cash by Pace Morby?

- Seller financing: The seller acts as the bank, carrying the loan with little or no money down, ideal when the property is owned free and clear.

- Subject-to deals: The investor takes over existing mortgage payments without paying off the loan, gaining ownership while the loan remains in the seller’s name.

- Lease options and executory contracts: Lease options allow leasing with the option to buy, while executory contracts (land contracts) let buyers pay over time before receiving legal title.

How does Pace Morby define and structure a subject-to deal in Wealth without Cash?

- Take over payments: A subject-to deal involves taking over the seller’s mortgage payments without qualifying for a new loan.

- Key steps: Obtain the mortgage statement, calculate equity, plan your exit strategy, and negotiate any cash to the seller.

- Legal protection: Use attorneys or title companies experienced in subject-to deals to prepare contracts and protect all parties.

Why are sellers open to creative finance deals according to Wealth without Cash by Pace Morby?

- Walkaway money and speed: Sellers often want to avoid Realtor fees, bank complications, or foreclosure, and creative finance can offer higher net returns or faster closings.

- Problem-solving approach: Morby shows that educating sellers and structuring deals to meet their needs can turn initial “no” into “yes.”

- Ongoing income: Some sellers prefer steady monthly payments and personalized solutions over a lump sum.

What are the main exit strategies for making money with creative finance in Wealth without Cash by Pace Morby?

- Wholesale deals: Assign contracts to cash buyers or homestead buyers for assignment fees.

- Wraps and lease options: Wrap the seller’s financing with your own terms to a new buyer, or lease with an option to buy, collecting option fees and higher rents.

- Sub-tail and rentals: Acquire properties subject-to and sell retail, or hold as rentals, group homes, or vacation rentals for steady cash flow.

How do I find and evaluate real estate deals using Pace Morby’s methods in Wealth without Cash?

- Lead generation: Use direct-to-seller marketing, agent relationships, referrals, wholesalers’ dead leads, and working for others to find deals.

- Driving for dollars and door knocking: Physically search for distressed properties and build trust with sellers through in-person contact.

- Comping and underwriting: Analyze deals by finding accurate comps, calculating ARV, and underwriting for cash flow, equity, and exit strategies.

What are the key concepts of comping and underwriting in Wealth without Cash by Pace Morby?

- True comps matter: Match subdivision, property type, size, and features, avoiding outdated or irrelevant comps for accurate property valuation.

- Underwriting for profit: Calculate ARV, wholesale maximum allowable offer, and all entry fees (arrears, closing, renovations, holding costs) to ensure profitability.

- Manual over auto-comping: Use tools like BatchLeads and BiggerPockets, but prioritize manual comping for accuracy and credibility.

How does Pace Morby recommend funding deals if you have little or no money in Wealth without Cash?

- Private money lenders: Borrow from individuals seeking returns, secured by promissory notes and deeds of trust, with rates typically between 8–15%.

- Hard money loans: Use short-term, higher-interest loans focused on the deal’s value, not your credit, for fix-and-flips or bridge financing.

- Professional presentations: Present deals with clear numbers, comps, and exit strategies, and always use proper legal documents to build trust with lenders.

How does Pace Morby advise building and scaling a real estate investing business team in Wealth without Cash?

- Start with virtual assistants: Hire VAs for lead generation, cold calling, and follow-up, paying based on skill and providing training.

- Add acquisition and disposition managers: Acquisition managers close deals, while disposition managers sell them; both can be paid on commission.

- Systematize and scale: Build a scalable system with clear roles, accountability, and property management for rentals or Airbnbs as your business grows.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.