Key Takeaways

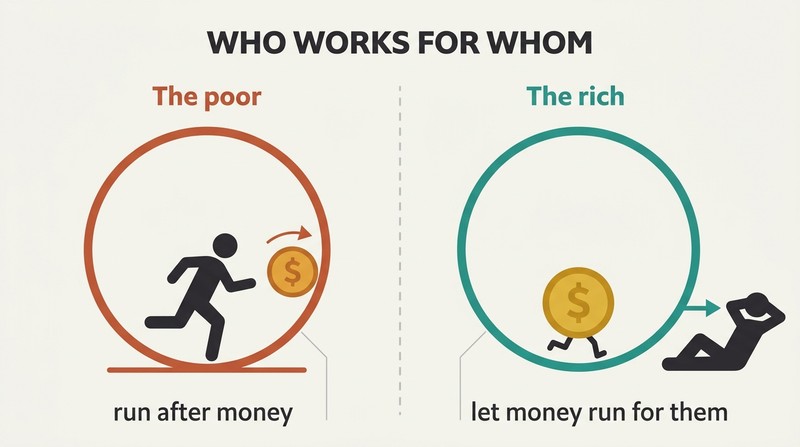

The poor work for money; the rich make money work for them

The core fault line of the book. Kiyosaki frames his entire philosophy around two father figures: his biological father, a PhD and Hawaii's superintendent of education who died with unpaid bills, and his best friend's father, an eighth-grade dropout who became one of the richest men in Hawaii. The educated dad chased pay raises and job security. The rich dad built assets that generated income whether he showed up or not.

Fear and desire run most lives. As a nine-year-old earning ten cents an hour, Kiyosaki learns that the cycle of get up, work, pay bills repeats because two emotions drive it: fear of not having money and the craving for what money buys. Most people never pause to ask whether a job is actually a long-term solution to a long-term problem.

What's striking is how Kiyosaki reframes a salary not as security but as a sedative for fear. The insight echoes behavioral economics: humans are loss-averse, so the dread of an unpaid bill overpowers the abstract goal of wealth. Yet the binary is overstated. Many salaried professionals build wealth through index funds and retirement accounts without ever owning a business. The dichotomy works better as a provocation than a literal law, nudging readers to examine whether their paycheck owns them rather than the reverse.

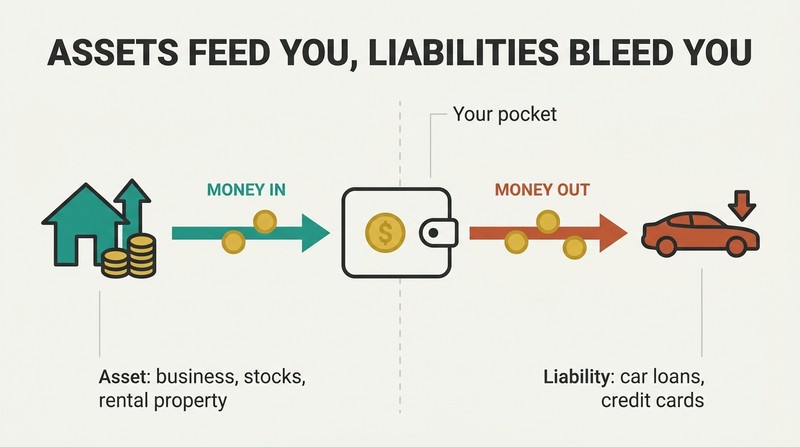

Buy assets that feed you; everything else is a liability

The one rule that matters most. Kiyosaki strips wealth down to a single distinction most adults get wrong: an asset puts money in your pocket, a liability takes money out. The rich accumulate assets. The poor and middle class accumulate liabilities they mistakenly believe are assets. He insists definitions live in cash flow, not dictionary jargon.

Assets he counts include:

1. Businesses that run without your presence

2. Stocks and bonds

3. Income-producing real estate

4. Notes and royalties from intellectual property

5. Anything that produces income or reliably appreciates

The income statement (money in, money out) must be read alongside the balance sheet (assets versus liabilities). The story is told by where the cash flows. In roughly 80 percent of families, the plot is hard work funneled into liabilities rather than assets.

The simplicity is the point and the weakness. Accountants rightly object that Kiyosaki's definitions ignore standard practice, but his cash-flow lens is pedagogically brilliant for beginners who glaze over at balance sheets. The deeper value lies in redirecting attention from income (what you earn) to cash flow (what you keep working for you). It anticipates the FIRE movement's obsession with passive income. The blind spot: appreciation and leverage carry real risk, and treating all debt as villainous oversimplifies how the wealthy actually deploy borrowed money strategically.

Your house is a liability dressed up as your proudest asset

The most controversial claim in the book. Kiyosaki argues that the family home, widely treated as a person's largest investment, drains money every month through mortgage, property taxes, maintenance, and utilities. He once drew his educated father a diagram showing cash flowing out the expense column, sparking a heated argument.

The hidden costs he itemizes:

1. People refinance repeatedly, paying for a home over their entire working lives

2. Property taxes can balloon (his in-laws faced $1,000 a month after retiring)

3. Homes do not always appreciate

4. Money locked in a house cannot grow in an investment portfolio

5. The biggest loss is the missed education of becoming a sophisticated investor

He is not against owning a home. He simply buys assets first, then lets their cash flow pay for luxuries.

This claim launched a thousand debates. Technically, a primary residence is a liability under Kiyosaki's cash-flow definition, and the 2008 housing collapse vindicated his warning that homes do not always rise. Yet he understates forced savings: a mortgage compels equity building that undisciplined savers would never achieve, and imputed rent is real value. Economists would call a paid-off home a consumption asset rather than an investment asset. The takeaway endures less as financial gospel than as an antidote to treating a mortgage as automatic wealth creation.

Keep your day job, but relentlessly mind your own business

Profession and business are not the same. Kiyosaki recounts Ray Kroc asking MBA students what business McDonald's was in. The answer they laughed off was real estate, not hamburgers: Kroc systematically bought the land beneath each franchise, making McDonald's one of the world's largest property owners. Your profession is what pays the bills. Your business is your asset column.

Build assets while employed. Kiyosaki worked at Xerox by day while buying real estate and small-cap stocks on the side, eventually out-earning his salary through his holding company. He warns against confusing a fancy car or golf clubs with assets (a new car loses roughly 25 percent of its value the moment you drive off the lot). The rich buy luxuries last, funded by income their assets already produce.

The McDonald's anecdote is a masterclass in seeing the real engine beneath a visible product, a lesson that extends to Amazon's cloud revenue funding its retail business. Kroc's land strategy is well documented. The advice to keep a day job while building assets is sober and underrated in an era romanticizing the quit-everything entrepreneur. Where Kiyosaki could go further: minding your own business demands surplus capital and time, luxuries the genuinely poor lack. The framework assumes a margin many readers must first manufacture through frugality before any asset column can grow.

Corporations let the rich earn, spend, then pay tax last

The sequence is everything. Employees earn, get taxed, then live on what remains. A corporation earns, spends on legitimate expenses, and pays tax only on what is left. Kiyosaki calls this one of the biggest legal advantages the rich exploit, and he traces income tax history to make the point: taxes were originally sold to the masses as a way to punish the rich, but government appetite pushed the burden onto the middle class.

Corporations offer two shields:

1. Tax advantages (expenses paid with pre-tax dollars, lower corporate rates)

2. Protection from lawsuits (the wealthy control assets while owning little personally)

He credits financial IQ to four domains: accounting, investing, understanding markets, and the law. The law, wrapped around the other three, is what turns walking into flying.

The historical framing is sharp: both Britain and the US introduced income tax as a temporary, rich-only levy that crept downward, a pattern public-finance scholars confirm. The corporate-veil and pre-tax expense advantages are real, though Kiyosaki glosses over how much income and complexity it takes before incorporation pays off, and aggressive structures invite audit risk. Modern readers should note tax law has tightened since the 1990s. The enduring lesson is not a specific loophole but a mindset: the tax code rewards business owners and investors over wage earners, and that asymmetry is learnable.

Work to learn skills, not to earn the biggest paycheck

Chase education over salary early. Kiyosaki quit a high-paying Standard Oil shipping job to join the Marines and learn leadership, then took a job at Xerox specifically to conquer his terror of selling. He recommends young people pick work for the skills it builds, not the wage it pays. A pilot with 100,000 flight hours has skills worthless outside aviation; overspecialization traps you.

The skills that compound. He tells of a gifted Singapore writer with a master's degree who refused to learn sales, insulted by the suggestion. Kiyosaki pointed to her own notes: she had written best-selling author, not best-writing author. The difference between talent and wealth is often one missing skill. The vital ones: sales, marketing, communication, and the management of cash flow, systems, and people.

The best-selling versus best-writing distinction is a genuinely memorable reframe of why competence and compensation diverge. Research on career capital (Cal Newport's work) supports the thesis: rare and valuable skills, not passion alone, create leverage. Kiyosaki's generalist gospel (know a little about a lot) clashes with deep-specialization advocates, and the truth is contextual: surgeons and software architects get rich by going deep. His real target is the person who hides technical brilliance behind an inability to sell or lead. For them, the prescription is precise and powerful: one new skill can multiply income.

Pay yourself first, even when the bills are screaming

Invert the order of payment. Most people pay everyone else (government, creditors, landlord) and pay themselves whatever scraps remain, which is usually nothing. Rich dad funneled money into his asset column before paying bills, even when short on cash. The pressure of unpaid creditors then became fuel, forcing him to generate new income rather than dip into savings.

The discipline is the engine. Kiyosaki frames this as building mental money muscles: letting the bullies (tax collectors, bill collectors) scream pushes you to invent income instead of caving. The rule, drawn from The Richest Man in Babylon, is not about irresponsibility. It pairs with two safeguards: keep expenses and consumer debt low so the bills you face are small, and never liquidate investments to pay them. He calls self-discipline the single biggest factor separating the rich from everyone else.

Pay yourself first is now standard personal-finance orthodoxy, popularized by automatic 401(k) contributions, and behavioral science backs it: automating savings before discretionary spending defeats present bias. Kiyosaki's twist (deliberately courting creditor pressure as motivation) is psychologically risky and not for everyone. For the financially fragile it could trigger ruin, not resourcefulness. The safer reading is the safeguard he buries: keep fixed obligations low enough that paying yourself first never actually jeopardizes solvency. As pure mindset, the idea that constraint breeds creativity has real support in studies on how scarcity can sharpen focus.

Five inner enemies sabotage even the financially literate

Knowledge is not enough. Kiyosaki names five obstacles that keep educated people poor:

1. Fear (of losing money)

2. Cynicism (the Chicken Little voice yelling the sky is falling)

3. Laziness (often disguised as being too busy)

4. Bad habits (paying yourself last)

5. Arrogance (ego plus ignorance, pretending to know what you don't)

Antidotes from the stories. On fear, he invokes Texans who brag about losing big and the Alamo turned into a rallying cry: winners let failure inspire them. On cynicism, his friend Richard backed out of a $42,000 Phoenix condo after a non-investor neighbor scared him; it later rented for over $1,000 a month. On laziness, the cure is a little greed, asking how can I afford it rather than declaring I can't afford it, which shuts the brain down.

This is the book's emotional core, and it aligns with modern findings that financial behavior is driven more by psychology than math (Morgan Housel's work makes the same case). The Chicken Little point is essentially a warning against taking advice from people with no skin in the game, a theme Nassim Taleb later formalized. The how can I afford it reframe is a clever cognitive tool: open questions activate problem-solving where closed statements end it. The weakness is survivorship bias in the success stories; for every Richard who missed a winner, someone avoided a genuine loss by listening to caution.

Sophisticated investors get their money back, then keep the asset free

Be an Indian giver with capital. Kiyosaki's term for the ideal investment: get your money back fast, then own the income-producing asset essentially for free. He bought a foreclosed condo for $50,000 with a $50,000 cashier's check, rented it to snowbirds for $2,500 a month in winter, and recovered his cash in about three years, leaving an asset that pays him indefinitely. With stocks, he moves money in before a catalyst, pulls his original stake out once it rises, and lets the free shares ride.

Focus, don't diversify, to get rich. He argues balanced portfolios are for people playing not to lose. Edison, Gates, and Soros were focused, not balanced. Put a lot of eggs in a few baskets, limit risk to money you can afford to lose, and expect home runs on only two or three of every ten investments.

The return-of-capital obsession mirrors how venture capitalists and real-estate syndicators actually think, prioritizing recovery of principal so remaining upside is house money. It is genuinely sophisticated. The focus-over-diversification advice, however, directly contradicts mainstream portfolio theory, where diversification is the only free lunch. Kiyosaki is describing wealth creation (concentration) rather than wealth preservation (diversification), and conflating the two is dangerous for novices. His own admission that he loses on two or three of ten deals reveals the survivorship math: this approach demands tolerance for failure and capital most readers cannot afford to vaporize.

Money is just an idea; financial intelligence creates it from almost nothing

Wealth starts in the head, not the wallet. Kiyosaki rejects the belief that it takes money to make money as the thinking of the financially unsophisticated. His closing example: a friend struggling to save $400,000 for four children's college bought a $79,000 Phoenix foreclosure for just $7,000 down. He sold it three years later for $156,000, rolled the gain tax-deferred into a mini-storage facility, then into a larger project throwing off over $3,000 a month, all feeding the college fund.

Each dollar is a choice about your future. Spend it foolishly and you choose poor; spend it on liabilities and you join the middle class; invest it in your mind and assets and you choose wealth. He turned $5,000 into a $1 million asset producing $5,000 monthly in under six years, insisting the science of making money is learnable and starts small.

The $7,000-to-college-fund story is the book's most concrete proof of concept, and tax-deferred exchanges (Section 1031) are a legitimate, powerful tool. Yet it leans heavily on a rising Phoenix market; the same moves in a downturn could have wiped the friend out, illustrating how Kiyosaki underweights luck and timing. The deeper, defensible claim is that financial creativity, leverage, and continuous learning compound far faster than wage-and-save thrift. As a philosophy it is empowering; as a guarantee it is overconfident. The honest middle ground: education lowers the capital and luck required, it does not eliminate them.

Analysis

Rich Dad, Poor Dad is less an investment manual than a work of financial philosophy disguised as memoir. Published in 1997, it endures because it attacks a target most personal-finance books ignore: the unexamined script of go to school, get a safe job, buy a house. Kiyosaki's rhetorical engine is the two-father parable, a device that lets him stage every money belief as a debate between security and freedom. Whether the rich dad literally existed has been questioned for decades, but the framework's pedagogical power does not depend on his historicity.

The book's lasting contributions are conceptual, not technical. The asset-versus-liability reframe, the cash-flow lens, the insistence that financial literacy is a fifth literacy schools refuse to teach, and the psychological diagnosis of fear, cynicism, and laziness as the true barriers to wealth all reorient how a reader perceives money. These ideas seeded an entire genre, from FIRE blogs to passive-income gurus.

Its weaknesses are equally clear. Specific tactics (no-money-down real estate, focused over diversified portfolios, courting creditor pressure) range from dated to reckless for the financially fragile, and the success stories ride a 1990s bull market that flatters the author's judgment while obscuring luck and survivorship bias. Critics note Kiyosaki sells seminars and games, making the book partly a funnel. Accountants reject his definitions outright.

Yet the central provocation holds up against modern behavioral finance, which increasingly agrees that wealth is driven by behavior, mindset, and patience rather than raw intelligence or income. Read as gospel, the book is hazardous. Read as a mindset-shifting argument that financial education is learnable, that the rich play by different and legal rules, and that every dollar is a vote for your future self, it remains one of the most influential money books ever written, precisely because it makes readers uncomfortable with advice they never thought to question.

Review Summary

Readers praise "Rich Dad Poor Dad" for its eye-opening insights into financial literacy and wealth-building strategies. Many credit the book with changing their perspective on money and motivating them to take control of their finances. However, some critics argue that the advice is oversimplified and potentially risky. Despite mixed opinions, the book remains highly influential, sparking discussions about financial education and challenging traditional views on work and wealth.

People Also Read

FAQ

What's "Rich Dad Poor Dad" about?

- Overview: "Rich Dad Poor Dad" by Robert T. Kiyosaki is a personal finance book that contrasts the financial philosophies of Kiyosaki's two father figures: his biological father (Poor Dad) and his best friend's father (Rich Dad).

- Core Message: The book emphasizes the importance of financial education, financial independence, and building wealth through investing in assets, real estate, and starting businesses.

- Rich vs. Poor Mindset: It highlights the differences in mindset between the rich and the poor, particularly in how they view money, work, and education.

- Financial Literacy: Kiyosaki stresses the need for financial literacy and understanding the difference between assets and liabilities to achieve financial success.

Why should I read "Rich Dad Poor Dad"?

- Financial Education: The book provides insights into financial education that are often not taught in traditional schools, helping readers understand how to manage money effectively.

- Mindset Shift: It encourages a shift in mindset from working for money to having money work for you, which is crucial for achieving financial freedom.

- Practical Advice: Kiyosaki offers practical advice on investing, entrepreneurship, and building wealth, making it a valuable resource for anyone looking to improve their financial situation.

- Inspiration: The book is motivational, inspiring readers to take control of their financial future and pursue their dreams of financial independence.

What are the key takeaways of "Rich Dad Poor Dad"?

- Assets vs. Liabilities: Understanding the difference between assets (which put money in your pocket) and liabilities (which take money out) is crucial for building wealth.

- Financial Literacy: Financial education is essential for making informed decisions about money and investments.

- Work for Money vs. Money Works for You: The rich focus on creating systems and investments that generate passive income, rather than solely relying on earned income.

- Mind Your Own Business: Focus on building and managing your own assets and investments, rather than just working for someone else.

What are the best quotes from "Rich Dad Poor Dad" and what do they mean?

- "The rich don’t work for money." This quote emphasizes the importance of creating passive income streams rather than solely relying on a paycheck.

- "It’s not how much money you make. It’s how much money you keep." This highlights the importance of managing expenses and investing wisely to build wealth.

- "The single most powerful asset we all have is our mind." Kiyosaki stresses the value of financial education and continuous learning to improve financial intelligence.

- "The love of money is the root of all evil." vs. "The lack of money is the root of all evil." This contrast shows the different perspectives on money between the rich and the poor.

How does Robert T. Kiyosaki define assets and liabilities in "Rich Dad Poor Dad"?

- Assets: According to Kiyosaki, assets are things that put money in your pocket, such as investments, real estate, and businesses.

- Liabilities: Liabilities are things that take money out of your pocket, like mortgages, car loans, and credit card debt.

- Common Misconception: Many people mistakenly consider their home an asset, but Kiyosaki argues it is a liability unless it generates income.

- Financial Literacy: Understanding this distinction is key to building wealth and achieving financial independence.

What is the significance of the "CASHFLOW Quadrant" in "Rich Dad Poor Dad"?

- Quadrant Overview: The CASHFLOW Quadrant categorizes income sources into four types: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I).

- Quadrant Differences: Each quadrant represents a different approach to earning money, with the right side (B and I) focusing on passive income and wealth-building.

- Path to Financial Freedom: Kiyosaki encourages moving from the left side (E and S) to the right side (B and I) to achieve financial freedom.

- Mindset and Skills: Success in the B and I quadrants requires a different mindset and skill set, emphasizing financial education and entrepreneurship.

How does "Rich Dad Poor Dad" suggest overcoming fear and doubt in financial decisions?

- Fear of Losing Money: Kiyosaki acknowledges that everyone fears losing money, but emphasizes that managing fear is crucial for financial success.

- Learning from Failure: He encourages viewing failures as learning opportunities and using them to build resilience and financial intelligence.

- Taking Calculated Risks: The book advocates for taking calculated risks and not letting fear prevent you from pursuing investment opportunities.

- Mindset Shift: Developing a mindset that embraces challenges and sees them as opportunities for growth is essential for overcoming fear.

What role does financial education play in "Rich Dad Poor Dad"?

- Foundation of Wealth: Financial education is the foundation for building wealth and achieving financial independence.

- Understanding Money: It involves understanding how money works, how to manage it, and how to make it work for you through investments.

- Continuous Learning: Kiyosaki emphasizes the importance of continuous learning and staying informed about financial markets and opportunities.

- Empowerment: Financial education empowers individuals to make informed decisions and take control of their financial future.

How does "Rich Dad Poor Dad" address the concept of "working for money" vs. "money working for you"?

- Traditional Path: Many people follow the traditional path of working for money, relying on a paycheck for financial security.

- Passive Income: Kiyosaki advocates for creating systems and investments that generate passive income, allowing money to work for you.

- Financial Freedom: Achieving financial freedom involves building assets that provide income without active involvement.

- Mindset Change: Shifting from a mindset of working for money to having money work for you is key to achieving long-term financial success.

What is the "Rich Dad" philosophy on taxes and corporations in "Rich Dad Poor Dad"?

- Tax Advantages: The rich use corporations to take advantage of tax benefits and protect their wealth.

- Legal Loopholes: Corporations offer legal loopholes that allow the rich to minimize taxes and maximize profits.

- Financial Education: Understanding tax laws and corporate structures is part of financial education and wealth-building.

- Playing Smart: Kiyosaki emphasizes the importance of playing smart and using the system to your advantage, rather than being exploited by it.

How does "Rich Dad Poor Dad" suggest building a strong financial foundation?

- Start Early: Begin building your financial foundation early to take advantage of compound interest and long-term growth.

- Invest in Assets: Focus on acquiring income-generating assets, such as real estate, stocks, and businesses.

- Financial Discipline: Practice financial discipline by managing expenses, avoiding unnecessary debt, and reinvesting profits.

- Continuous Education: Continuously educate yourself about financial markets, investment strategies, and wealth-building techniques.

What are the steps to achieving financial freedom according to "Rich Dad Poor Dad"?

- Set Clear Goals: Define your financial goals and create a plan to achieve them, focusing on building assets and passive income.

- Increase Financial Literacy: Continuously improve your financial literacy through education, reading, and learning from mentors.

- Take Action: Actively seek investment opportunities and take calculated risks to grow your wealth.

- Build a Network: Surround yourself with like-minded individuals and mentors who can support and guide you on your financial journey.

Rich Dad Series

About the Author

Other books by Robert T. Kiyosaki

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.