Key Takeaways

Where your money comes from matters more than how much

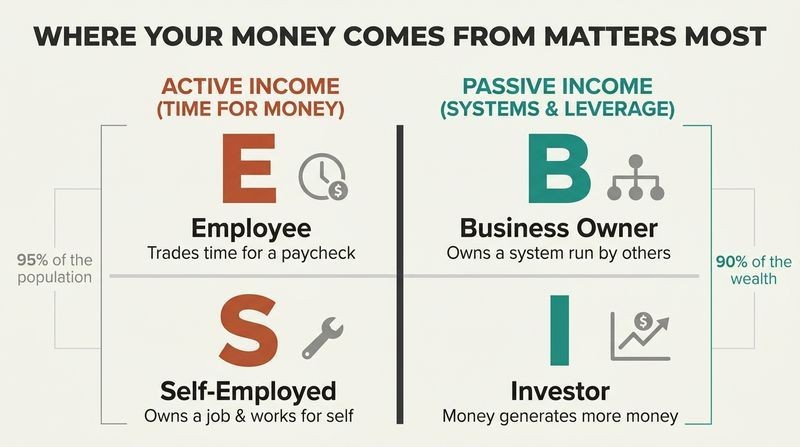

Income source defines your financial life. Kiyosaki's central tool is the CASHFLOW Quadrant, a simple diagram split into four ways people earn. The left side holds the Employee (E), who trades time for a paycheck, and the Self-employed (S), who owns a job and gets paid for personal effort. The right side holds the Business owner (B), who owns a system run by other people, and the Investor (I), whose money generates more money.

The same person can earn from any quadrant. A doctor can be an employed E at a hospital, an S in private practice, a B owning a clinic staffed by other doctors, or an I living off rental income. What separates the rich isn't profession but which quadrant feeds them.

What's striking is how the quadrant reframes a question schools never ask: not what you do, but how you get paid. The framework echoes economist Robert Reich's distinction between routine workers and symbolic analysts, yet Kiyosaki adds a sharper edge by tying income source to tax treatment and freedom. The model's weakness is its binary moralizing, implying the left side is a trap. In reality, many thrive as employees, and plenty of business owners go bankrupt. Still, as a diagnostic lens for asking where leverage comes from, the quadrant remains unusually clarifying for people who never considered they had a choice.

Build pipelines, not buckets, so income flows without you

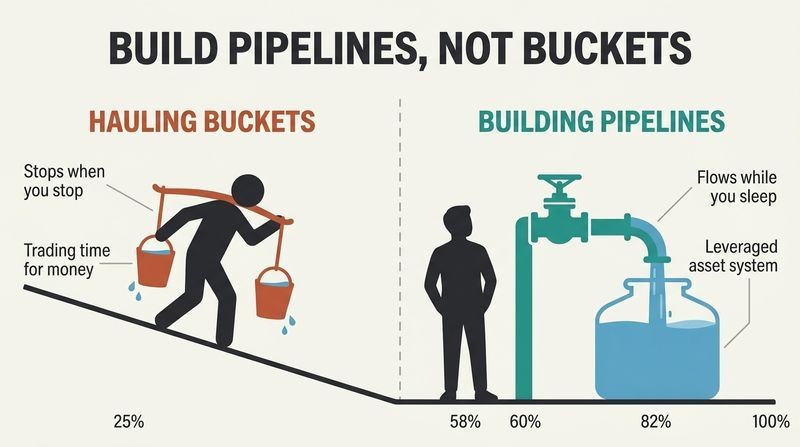

The parable of two water haulers. Kiyosaki retells a story his mentor told him at age twelve. A village needs water, so two men win contracts. Ed grabs buckets and hauls water by hand, earning immediately but trapped in endless labor. Bill writes a business plan, raises capital, hires a crew, and builds a pipeline. Bill earns a fraction per bucket but delivers billions of buckets whether he works or not. Ed works harder forever; Bill becomes free.

The lesson drives the whole book. Kiyosaki says he constantly asks himself: am I building a pipeline or hauling buckets? Employees and the self-employed haul buckets, their income stopping the moment they stop. Business owners and investors build pipelines that pump cash while they sleep.

The pipeline metaphor captures the economic concept of scalability, where revenue decouples from hours worked. It resonates with what venture investors call leverage and what software founders prize in zero-marginal-cost distribution. The deeper insight is psychological: bucket-hauling feels safer because reward is immediate and visible, while pipeline-building requires tolerating months of apparent failure before payoff. Behavioral economists call this present bias. The story's limitation is that it glosses over how brutal pipeline-building actually is. Most pipelines never get built; most startups die. Bill's success looks inevitable in hindsight, a survivorship bias the fable quietly relies on to make its point land cleanly.

Your house is a liability, not the asset banks claim

Assets feed you, liabilities eat you. Kiyosaki redefines the two words in plain cash-flow terms: an asset puts money in your pocket, a liability takes money out. By this test, the family home most people call their largest asset is actually a liability, draining cash through mortgage, taxes, maintenance, and insurance.

The banker isn't lying, just not telling the whole truth. When a banker calls your house an asset, they omit whose asset. Your mortgage appears as a liability on your balance sheet and as an asset on the bank's. An $80,000 loan at 8% over 30 years can cost roughly $131,000 in interest, closer to 160% than 8%. Even a paid-off house keeps costing you taxes and upkeep, so it never truly generates income.

This redefinition is Kiyosaki's most provocative and most contested claim. Accountants rightly note that a house is an asset on a conventional balance sheet because it holds market value. Kiyosaki sidesteps this by adopting a strict cash-flow definition, which is internally consistent but unconventional. The valuable core survives the quibble: a primary residence rarely produces income and often masks ongoing costs people underestimate. Research on homeowner wealth shows forced savings through mortgage paydown does build equity, complicating his blanket dismissal. The reframe's real gift is forcing readers to ask of every purchase a single ruthless question: does this put money in or take money out?

Wealth is measured in time, not dollars

Count days, not net worth. Kiyosaki defines wealth as the number of days you could maintain your lifestyle without anyone in your household physically working. If your expenses run $1,000 a month and you have $3,000 saved, your wealth is roughly 90 days. By this metric you are wealthy only when passive income from your assets permanently exceeds your expenses.

Rich and wealthy are different. Kiyosaki and his wife were millionaires by 1989 because their business generated income, but not truly wealthy until 1994, when investment cash flow alone covered all living costs indefinitely. He warns that many high earners operate at financial red line, spending everything as fast as it arrives, so a fat paycheck buys zero days of real freedom.

Defining wealth as time rather than money is the book's most quietly radical idea, and it aligns with the financial independence movement's later formalization of the same concept as the crossover point, where passive income surpasses expenses. It also echoes Vicki Robin's Your Money or Your Life, which reframes spending as hours of life energy traded. The framing exposes the hedonic treadmill: lifestyle inflation can leave a surgeon poorer in days than a frugal teacher. One caution is that passive income is rarely as passive or as stable as the tidy formula suggests; markets crash, tenants leave, and businesses require tending, which can shrink those carefully counted days overnight.

Crossing quadrants is identity change, not a career move

It is who you become, not what you do. Kiyosaki insists the hard part of moving from employee to business owner is internal. His educated father, a brilliant government official, understood business intellectually but could not handle it emotionally; when his ventures lost money, he retreated to the security of employment. Changing quadrants, Kiyosaki says, is as profound as a caterpillar becoming a butterfly, and even your friendships shift.

Money is a drug. His mentor refused to pay him as a boy so he'd never get addicted to working for a paycheck. The pattern you use to acquire money becomes an addiction that's hard to break. The frame he repeats is BE-DO-HAVE: who you must BE shapes what you DO, which determines what you HAVE.

Kiyosaki's emphasis on identity prefigures what behavior-change researchers now treat as the most durable lever. James Clear argues lasting change flows from identity (becoming the kind of person who invests) rather than from goals. Carol Dweck's work on fixed versus growth mindsets explains why his educated father, accustomed to being the smartest in the room, froze when failure threatened his self-image. The drug metaphor is more than rhetoric; neuroscience links predictable income to dopamine-regulated reward circuits, which makes a steady paycheck genuinely habit-forming. The framework's limit is that it can blur into victim-blaming, treating structural barriers like debt loads and wage stagnation as mere mindset problems.

Owning a system beats being the system

An S owns a job; a B owns a system. The test Kiyosaki offers: could you leave your business for a year and return to find it more profitable? A true business owner can, because competent people run a system they own. A self-employed dentist cannot, because when the dentist vacations, the income vacations too. The S often IS the system.

You don't need a better burger. Nearly everyone can grill a tastier hamburger than McDonald's, yet only McDonald's built the system that served billions. Kiyosaki names three routes to owning a system: build your own C-corporation from scratch, buy a proven franchise, or join a network marketing organization for a low entry cost. Each removes variables so you can focus on developing people.

The system-over-product insight is the book's most commercially durable lesson, and it maps cleanly onto Michael Gerber's E-Myth, which Kiyosaki cites: most small businesses fail because the technician who loves the craft mistakes doing the work for building the enterprise. Ray Kroc's genius was never the burger but the replicable operating system and the underlying real estate. The framework usefully separates entrepreneurship from self-employment, a distinction many aspiring founders miss. Where Kiyosaki's enthusiasm runs ahead of evidence is network marketing, which he frames as a democratized franchise; independent research shows the vast majority of participants earn little or lose money, a caveat worth holding alongside his optimism.

See money with your mind, since 95% is invisible

The eyes deceive; the numbers reveal. Kiyosaki recalls buying a Waikiki condo at 27 that lost $100 a month, seduced by a nice paint job and a promise that prices always rise. His mentor tore the deal apart with questions about cap rates, vacancy, and cash flow, then sent him back to renegotiate the terms until the same property produced $80 a month in profit. The price never changed; the structure did.

Financial literacy is the eyesight. Average investors invest 95% with their eyes and emotions and only 5% with their minds. Training your mind to read financial statements lets you see deals, risk, and cash-flow direction that others miss. As he puts it, your profit is made when you buy, not when you sell.

The claim that money is seen with the mind dovetails with expertise research showing that chess masters and radiologists perceive patterns invisible to novices, what cognitive scientists call chunking. Financial literacy functions the same way: statements become a language that renders risk legible. Kiyosaki's deeper point, that emotion hijacks judgment, anticipates Daniel Kahneman's findings on how fear and greed distort decisions. The buy-side profit principle is genuine value-investing orthodoxy, echoing Benjamin Graham's margin of safety. The vulnerability is that the same confidence in reading deals can curdle into overconfidence; the very skill that spots opportunity can blind investors to tail risk, as 2008 reminded a generation of property bulls.

The rich pay less tax because they earn differently

Tax law rewards the right side. Kiyosaki argues employees are effectively 50/50 partners with the government, taxed heavily and at the source through withholding before they ever see their pay. The only tax break offered to high-earning employees is to take on more mortgage debt. Business owners and investors, by contrast, earn through entities and assets that the tax code treats far more kindly.

Earn, spend, then be taxed. An employee's sequence is earn, taxed, spend. Route income through a corporation first and the sequence becomes earn, spend, taxed, expensing legitimate costs before the government takes its cut. He cites making a million in capital gains and deferring the tax through a real estate exchange. The 1986 Tax Reform Act, he notes, gutted shelters for employees and professionals while leaving the B and I sides largely intact.

This is among Kiyosaki's most factually grounded arguments, and tax scholars broadly agree the code favors capital over labor, a structural feature documented by economists from Thomas Piketty to the architects of the carried-interest debate. The earn-spend-taxed reframe captures a real asymmetry in how pass-through entities and capital gains are treated. The honest caveat Kiyosaki underplays is that these advantages require genuine business activity, real risk, and competent advisors; deductions are not free money, and the IRS distinguishes legitimate expenses from disguised personal consumption. His framing can tempt readers toward aggressive interpretations. The sound takeaway is structural literacy: the same dollar is taxed differently depending on which quadrant produced it.

Diversification is protection for people who don't know investing

Focus, don't scatter. Kiyosaki argues that diversification is a strategy for not losing rather than for winning, and that genuinely rich investors concentrate their efforts. He cites Warren Buffett, who deliberately rejects standard diversification dogma, arguing that concentration can lower risk by forcing an investor to understand a business deeply before buying. Security-minded people gravitate to diversification, blue-chip stocks, and mutual funds precisely because they don't want to study the game.

Become an expert at one problem. The fast track comes from mastering one type of financial problem, not dabbling in many. Bill Gates solved software distribution, Buffett solved business valuation, and Kiyosaki and his wife specialized in small apartment buildings. Outside their niche, they hand money to specialists they trust rather than pretending to know everything.

The focus-versus-diversify debate exposes a genuine fault line in finance. Kiyosaki and Buffett champion concentration, but the counterweight is overwhelming academic evidence, from Harry Markowitz's Nobel-winning portfolio theory to index-fund pioneer John Bogle, that diversification reliably improves risk-adjusted returns for investors without an edge. The reconciliation lies in a word Kiyosaki uses but underweights: skill. Concentration rewards those with informational or analytical advantage and punishes everyone else. For the typical investor, broad index funds remain the rational default. His real contribution is reframing diversification not as universally wise but as a deliberate trade of upside for safety, a choice that should be conscious rather than reflexive.

Be the bank, never the banker, to create money

Play the role banks play. Kiyosaki's favorite move: buy a house worth $100,000 for $80,000, then sell it for the full $100,000 on owner-financed terms with low down payment and easy monthly payments. He pockets a $30,000 IOU that pays him interest, exactly as a bank earns interest on loans, while the buyer assumes taxes, maintenance, and upkeep. He calls this creating money from almost nothing.

The game is who is indebted to whom. The more people indebted to you, the wealthier you are; the more you owe others, the poorer. He bought 87 acres for $115,000, sold the house and 30 acres for $215,000 on terms, kept 57 acres debt-free, and walked away with land plus profit. His rule: if you take on debt and risk, make sure you get paid.

The be-the-bank strategy is real estate's seller-financing and lease-option toolkit, legitimate techniques that shift Kiyosaki from borrower to lender and let him capture the interest spread banks normally pocket. The framing as creating money is loose; he is really capturing arbitrage between a wholesale purchase and a retail financed sale, plus the time value lenders monetize. The model works beautifully in his telling because every buyer pays reliably and every property appreciates. Reality intrudes through defaults, foreclosures, illiquidity, and market downturns, the very risks 2008 inflicted on leveraged property players. The durable insight is the mindset shift from being someone's debtor to engineering positions where others owe you.

Take baby steps and underachieve daily toward huge dreams

Great leaps fail; baby steps compound. Kiyosaki warns against the crash-diet approach to money, the all-at-once effort that collapses within weeks. Drawing on goal coach Raymond Aaron, he advises dreaming enormous dreams but setting deliberately small daily goals. Instead of an hour at the gym, commit to twenty minutes, so you feel underwhelmed rather than overwhelmed and actually keep going.

Three habits separate the lasting rich from the temporarily rich. A study of people who rose from poverty found they shared long-term vision, delayed gratification, and harnessing compound growth. Families who fell from wealth in three generations showed the opposite: short-term thinking, craving instant gratification, and abusing compounding through debt. Knowledge compounds like money, so each small learning step multiplies over years.

This is the book's most behaviorally sound prescription, anticipating the habit science later popularized by BJ Fogg's tiny habits and James Clear's atomic habits, both of which show that shrinking a behavior below the threshold of resistance is how habits actually stick. The delayed-gratification finding echoes Walter Mischel's marshmallow experiments, which linked the capacity to wait with long-term life outcomes, though that research has since been nuanced by studies showing trust and economic stability heavily shape a person's willingness to wait. Kiyosaki's framing of knowledge as compounding is especially valuable, since it reframes slow learning not as falling behind but as quietly accumulating exponential advantage that becomes visible only years later.

Treat disappointment as tuition, and never run from mistakes

Few get rich because few tolerate disappointment. Kiyosaki spent two years as the worst salesman at Xerox, perpetually near firing, because his mentor had pushed him into sales precisely to cure his shyness and fear of rejection. The skill he learned mattered less than the emotional muscle: turning disappointment into an asset rather than a wall that stops you forever. People who say I'll never do that again have let disappointment end their learning.

Practical rules for failing well. Expect disappointment so you stay calm and think clearly. Keep a mentor on call for financial emergencies, as he did when a seller changed terms at closing and three phone calls taught him negotiation tactics he still uses. Be kind to yourself, and above all tell the truth rather than run, the lesson his father drilled in after a childhood mistake.

Kiyosaki's reframing of disappointment as tuition aligns with resilience research and Angela Duckworth's work on grit, which finds that sustained effort through setbacks predicts achievement better than talent. His insistence that emotional intelligence dominates financial intelligence draws explicitly on Daniel Goleman, and the claim holds up: the ability to act calmly under loss is what separates investors who buy in downturns from those who panic-sell. The mentor-on-call practice is a smart externalization of self-regulation, outsourcing composure to a trusted voice when your own emotions hijack judgment. The honest tension is that not every failure carries wisdom; sometimes a bad deal is just a bad deal, and knowing when to quit, as he concedes, is its own intelligence.

Analysis

Rich Dad's Cashflow Quadrant is a thesis-driven personal-finance manifesto built around a single elegant diagram and a contrarian premise: that financial freedom depends less on how hard you work or how much you earn than on which of four structural positions generates your income. Written as the sequel to Rich Dad Poor Dad, it braids autobiography (homelessness in 1985, financial freedom by 1994), parable (the water pipeline), and a seven-step action plan into an accessible argument aimed at employees and professionals contemplating a leap to ownership and investing.

The book's enduring value lies in its reframing power. By redefining assets and liabilities in cash-flow terms, measuring wealth in days rather than dollars, and insisting that crossing quadrants is an identity transformation rather than a job change, Kiyosaki gives lay readers a vocabulary for questions schools ignore. Its BE-DO-HAVE psychology and emphasis on emotional intelligence over technical knowledge are genuinely ahead of their 1998 publication, anticipating later habit and mindset literature.

The weaknesses are equally real and worth flagging for readers. The rich dad figure may be a composite or fictional device, the real estate examples assume a perpetually rising market and reliably paying buyers, and the enthusiasm for network marketing and aggressive tax positioning outruns the evidence. Kiyosaki's anti-diversification stance contradicts mainstream portfolio theory and is safe only for investors with genuine edge. His framing can also slide into implying that financial struggle is purely a mindset failure, underweighting structural forces like wage stagnation, debt, and luck.

Read critically, the book is best treated as a perspective-shifting lens rather than an operating manual. Its core gifts are durable: think in systems, build assets that pay you, master one domain deeply, tolerate disappointment, and never confuse a paycheck with security. Those principles survive the hype, the dated economics, and the salesmanship that surrounds them.

Review Summary

Cash Flow Quadrant received mixed reviews. Many praised its insights on financial education and mindset shifts, finding it eye-opening and potentially life-changing. Readers appreciated Kiyosaki's explanations of different income sources and paths to financial freedom. However, some criticized the book for being repetitive, lacking practical advice, and oversimplifying complex financial concepts. Critics also noted Kiyosaki's controversial views on formal education and his self-promotion throughout the book. Overall, readers found value in the book's core ideas but had varying opinions on its execution and applicability.

People Also Read

Glossary

CASHFLOW Quadrant

Four ways people earn incomeKiyosaki's central framework dividing income earners into four types: Employee (E) and Self-employed (S) on the left side, who trade time and effort for money, and Business owner (B) and Investor (I) on the right side, who earn from systems and assets that generate money. The quadrant you primarily earn from reflects your core values, mindset, and relationship to security versus freedom.

Asset and Liability (Kiyosaki's definition)

In versus out cash flowKiyosaki strips these accounting terms to cash-flow basics: an asset is anything that puts money into your pocket, and a liability is anything that takes money out. By this test a personal residence counts as a liability because it drains cash through mortgage, taxes, and upkeep, while rental property generating positive cash flow counts as an asset.

BE-DO-HAVE

Identity precedes action precedes resultsA formula Kiyosaki borrows to argue that wealth begins with who you must BE (your thoughts, beliefs, and identity), which determines what you DO (your actions), which produces what you HAVE (your results). He contends most people fixate on doing and having while ignoring the internal being that actually drives lasting change.

Seven Levels of Investors

Ranking of investor sophisticationA scale Kiyosaki adapted from John Burley, ranging from Level 0 (nothing to invest) through borrowers, savers, smart-but-untrained investors, long-term investors, sophisticated investors, up to Level 6 capitalists who create investments using other people's money and time. He warns that Level 4 cannot be skipped on the path to higher levels.

Be the bank, not the banker

Earn interest like lenders doKiyosaki's strategy of taking the lender's role rather than the borrower's. By buying property below market and reselling it on owner-financed terms, an investor collects interest payments and creates an asset, just as a bank does, while transferring ownership costs and risk to the buyer. The underlying game, he says, is who is indebted to whom.

Financial red line

Spending equals income monthlyKiyosaki's term, borrowed from engine mechanics, for living at maximum financial strain where monthly income and expenses are nearly equal regardless of how much you earn. Just as redlining an engine shortens its life, operating finances at the red line leaves no margin and makes people one setback away from bankruptcy.

FAQ

What's Rich Dad's Cashflow Quadrant about?

- Financial Freedom Focus: The book explores achieving financial freedom by understanding different income sources through the CASHFLOW Quadrant.

- Quadrant Categories: It categorizes individuals into four types: Employee (E), Self-employed (S), Business owner (B), and Investor (I).

- Mindset Differences: The left side (E and S) focuses on job security, while the right side (B and I) emphasizes wealth creation and financial independence.

- Path to Change: Kiyosaki encourages moving from the left to the right side of the Quadrant for financial freedom.

Why should I read Rich Dad's Cashflow Quadrant?

- Transformative Insights: The book challenges conventional beliefs about job security and wealth, offering new perspectives on money.

- Practical Guidance: It provides actionable steps and strategies for achieving financial independence.

- Relatable Examples: Kiyosaki shares personal anecdotes and lessons from his "rich dad," making the concepts easy to understand and apply.

What are the key takeaways of Rich Dad's Cashflow Quadrant?

- Quadrant Understanding: Recognizing where you currently stand in the Quadrant helps identify your path to financial freedom.

- Financial Education Importance: Kiyosaki stresses the need for financial education to navigate money management and investing complexities.

- Mindset Shift: A significant takeaway is shifting from seeking job security to pursuing financial freedom through entrepreneurship and investing.

What is the CASHFLOW Quadrant in Rich Dad's Cashflow Quadrant?

- Four Income Sources: The Quadrant categorizes income sources as Employee (E), Self-employed (S), Business owner (B), and Investor (I).

- Left vs. Right Side: The left side (E and S) is about job security, while the right side (B and I) focuses on wealth through business and investments.

- Path to Financial Freedom: Understanding the Quadrant helps individuals identify their current financial situation and steps to improve it.

How does Rich Dad's Cashflow Quadrant define an asset and a liability?

- Asset Definition: An asset is something that puts money into your pocket, like rental properties or dividend-paying stocks.

- Liability Definition: A liability takes money out of your pocket, such as debts and expenses that do not generate income.

- Understanding Importance: Kiyosaki emphasizes understanding these definitions to make informed financial decisions, as many mistakenly consider liabilities as assets.

How can I transition from the E or S quadrant to the B or I quadrant according to Rich Dad's Cashflow Quadrant?

- Education and Learning: Financial education is crucial for making informed decisions and understanding the market.

- Start Small: Begin with small steps towards entrepreneurship or investing to gain experience and confidence.

- Seek Mentorship: A mentor who has successfully transitioned can provide valuable guidance and support.

What are the three kinds of business systems mentioned in Rich Dad's Cashflow Quadrant?

- Traditional C-type Corporations: These require developing your own system and significant effort to run effectively.

- Franchises: Operating under an established system reduces the risk of starting a new business from scratch.

- Network Marketing: Joining an existing system offers a low-cost entry point and potential for passive income.

What is financial intelligence according to Rich Dad's Cashflow Quadrant?

- Money Management Understanding: It involves managing money effectively, including making, keeping, and growing it over time.

- Distinguishing Facts from Opinions: Recognizing the difference is crucial for sound investment decisions.

- Long-Term Perspective: Financial intelligence includes understanding risks and rewards associated with different strategies.

What are the seven levels of investors discussed in Rich Dad's Cashflow Quadrant?

- Level 0: Nothing to Invest: Living paycheck to paycheck with no money to invest.

- Level 1: Borrowers: Relying on borrowing, leading to a cycle of debt.

- Level 2: Savers: Using low-risk, low-return vehicles, missing better opportunities.

- Level 3-6: Ranging from "Smart" Investors to Capitalists, each level shows increasing sophistication and wealth creation.

How does Rich Dad's Cashflow Quadrant suggest managing risk in investing?

- Education is Key: Understanding the market and financial principles is crucial for managing risk.

- Start Small and Learn: Small investments allow learning from mistakes without significant risk.

- Diversification and Strategy: Focus on well-researched investments with a clear strategy to mitigate risk.

What are some common misconceptions about money discussed in Rich Dad's Cashflow Quadrant?

- Job Security Misconception: True security comes from owning assets, not job security.

- Home as an Asset: Homes are often liabilities due to ongoing expenses, not assets.

- Investment Risks: Investing isn't inherently risky; lack of education poses the real risk.

What are the best quotes from Rich Dad's Cashflow Quadrant and what do they mean?

- “True freedom requires financial freedom.”: Financial independence is essential for overall freedom in life.

- “Profit is made when you buy.”: Successful investing starts with informed purchasing decisions.

- “Indebtedness equals poverty.”: Debt limits financial freedom; strive for independence.

Rich Dad Series

About the Author

Other books by Robert T. Kiyosaki

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.