Key Takeaways

Wake up daily declaring: I'm an investor hunting today's deal

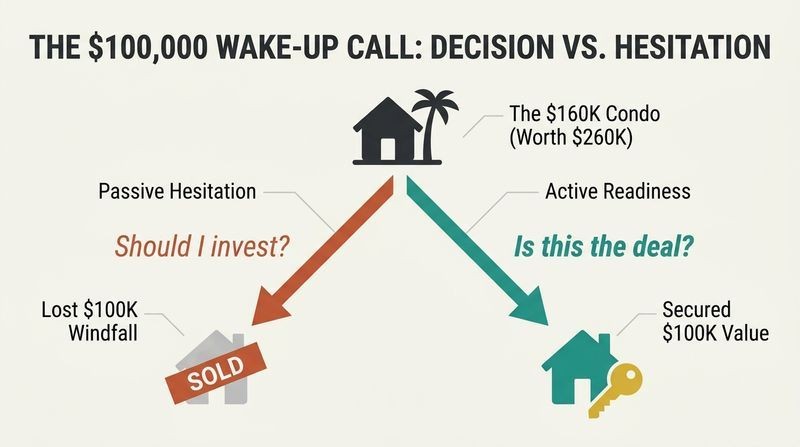

The $100,000 wake-up call. Gary Keller, founder of Keller Williams, once toured a beachfront condo listed at $160,000 that was clearly worth $260,000. He hesitated, said "we'll think about it," and called days later. The agent laughed: it had sold the next day. He had lost a $100,000 windfall through one moment of indecision. The lesson reframed his entire identity. He had been asking "Should I invest?" when the right question was "Is this the deal?"

True investors adopt a permanent mental posture. Every morning they affirm that today could be the day an opportunity surfaces and a deal gets made. This readiness is not arrogance, it is preparation that lets them act decisively when others dither and lose the prize.

What's striking is how Keller frames identity before action, echoing behavioral psychology's finding that self-concept drives behavior more reliably than willpower. James Clear's work on identity-based habits makes the same case: you act in accordance with who you believe you are. The condo story also illustrates the cognitive bias of "omission regret," where inaction haunts us more than mistakes. There is mild risk here too: an identity of constant readiness could tip into the impulsive speculation Keller warns against elsewhere. The discipline is that readiness must be paired with strict criteria, otherwise eagerness becomes recklessness dressed up as confidence.

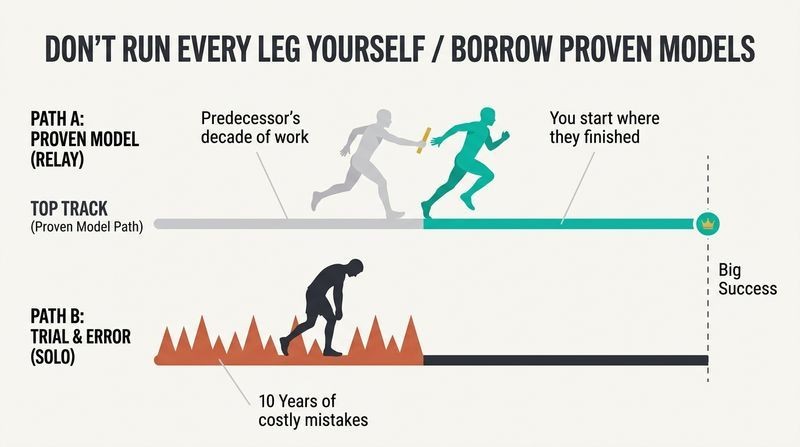

Borrow proven models so you skip a decade of costly mistakes

Big Goals plus Big Models equal Big Success. Keller's core formula is that ambitious targets become achievable only when paired with proven systems built from the best practices of high achievers. He compares it to a relay race: a good model hands you the baton mid-race, letting you start where predecessors finished rather than running every leg yourself.

A proven model is simply a repeatable method that produces predictable results. To build this book, the authors interviewed over 100 investors who each owned at least $1 million in real estate, averaging roughly 50 rental units and over $100,000 in annual cash flow. The collective wisdom became five models. The question that matters most is not "whose mistakes" you learn from, but whether they are your own or someone else's.

This is essentially modeling theory, which Keller credits to Tony Robbins, but its deeper roots run through Albert Bandura's social learning research and the apprenticeship traditions of every craft guild in history. The relay-baton metaphor is apt, yet there is a survivorship-bias caveat worth naming: interviewing only millionaires reveals what winners did but not how many imitators followed identical models and still failed. The models capture necessary conditions, not sufficient ones. Markets, timing, and temperament vary. Still, the principle that deliberate imitation beats blind trial and error is robust, and it counters the romantic myth of the lone, intuitive genius investor.

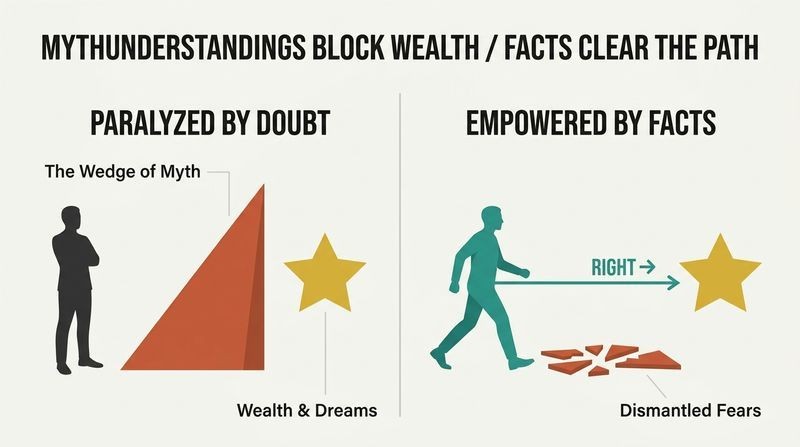

Your fears about investing are MythUnderstandings, not facts

Eight beliefs stand between you and wealth. Keller coins "MythUnderstandings" (part myth, part misunderstanding) for the doubts that paralyze would-be investors. Three concern how you see yourself: that your job will fund your wealth, that you do not need wealth, and that you simply cannot do it. Five concern investing itself: that it is complicated, requires rare knowledge, is risky, demands market timing, or that all good deals are taken.

He dismantles each. Mike Tyson earned over $400 million and still went bankrupt, proving a high income is not wealth. Barbara Mattson, a nurse drowning in medical bills, used a $20,000 disability settlement to buy rental property instead of paying debt, and built a $9 million portfolio. Fear, Keller argues, is a wedge that doubt drives between you and your dreams.

The reframe of fear as misinformation rather than rational caution is psychologically shrewd. Cognitive behavioral therapy operates on precisely this premise: distorted beliefs, not external reality, generate most self-limiting behavior. The Tyson example is devastating precisely because it severs the intuitive link between income and security that most people never question. Worth noting, though, that some of these "myths" contain partial truths. Investing genuinely can be risky for the unprepared, and timing does matter. Keller's rhetorical move is to redefine these as solvable through knowledge rather than reasons to abstain, which is empowering but occasionally understates the real learning curve novices face.

Build wealth on Capital first, not Consumption left over

The Money Matrix flips your priorities. Keller distinguishes being rich (having money, often from a job that stops paying when you stop working) from being financially wealthy (owning assets that generate income whether you work or not). The Money Matrix sorts every dollar into four roles: Capital (invested to grow), Cash Flow (income from investments), Cash (reserves), and Consumption (spending on things that do not grow).

Investors fund Capital first, then live on what remains. Consumers spend first and invest whatever is left, which is usually nothing. The result is what Keller calls Shadow Wealth: the appearance of prosperity (big house, nice car) with no underlying assets, leaving someone one pink slip from disaster. Sir John Templeton reportedly lived on half his income early on, gaming how much he could invest.

The Money Matrix restates "pay yourself first" but sharpens it by distinguishing four destinations for money rather than the usual binary of save versus spend. The Shadow Wealth concept anticipates research from The Millionaire Next Door, which found that many genuine millionaires drive used cars and live modestly while high earners often accumulate liabilities. Behavioral economists call the underlying trap "lifestyle creep" or hedonic adaptation: spending rises to meet income, so satisfaction resets. The framework's power is sequencing. By making Capital the first claim on income rather than the residual, it converts investing from an act of leftover willpower into a fixed, automatic priority.

Track net worth weekly and ask: how do I grow this?

Net worth is the scoreboard. During years of breakfast meetings with his mentor Michael, Keller learned to keep a one-page personal balance sheet listing assets minus liabilities. Each meeting ended with one question: how can you make that number grow? Forbes ranks the wealthy by net worth, not income, because net worth is the truest measure of financial standing.

Tracking it over time revealed which decisions helped and which hurt. A new car was an asset, but a depreciating one that lowered net worth. Real estate was an appreciating asset that raised it. Keller realized his own home was an "accidental asset," with each mortgage payment quietly building equity. The shift from accidental assets to intentional investments is what turns an earner into an investor.

The discipline of frequent measurement aligns with a well-documented principle from management and behavior change: what gets measured gets managed. Weighing yourself daily, logging expenses, or tracking net worth all leverage the feedback loop that makes abstract goals concrete. The mentor's single recurring question is a clever forcing function, channeling attention toward growth rather than mere observation. One nuance: net worth can be a noisy weekly signal given market swings and illiquid real estate valuations, which risks emotional overreaction. The deeper value is less the precise number than the habit of connecting daily financial choices to a long-term trajectory.

Real estate is the most able investment: ten built-in advantages

Why real estate beats the alternatives. Keller argues no other vehicle has lifted average people's net worth like property ownership. He catalogs its advantages with a memorable list of "-able" traits. Real estate is accessible (easy to finance), appreciable (historically about 6.1% annually, outpacing inflation), leverageable, rentable, improvable, and livable.

Leverage is the quiet multiplier. Put $30,000 down on a $150,000 house that appreciates 6.1%, and your $9,150 gain is measured against your $30,000 stake, not the full price, yielding over 30% return. It is also tax-favored in three ways (deductible expenses, depreciation, and deferral via 1031 exchanges) and remarkably stable, with a standard deviation around 4% versus the stock market's 16.8% over 1973 to 2003. Trammell Crow put it bluntly: the way to wealth is debt.

The leverage math is the engine of the entire book and deserves scrutiny. Leverage magnifies gains and losses symmetrically. The same mechanism that turns 6% appreciation into 30% returns turns a 6% decline into a 30% wipeout of equity, as 2008 demonstrated brutally after this 2005 book was written. Keller's stability data predates the housing crash, so the "slow to fall" claim warrants caution. That said, the structural tax advantages and the ability to force value through improvements remain genuinely distinctive to real estate. The honest synthesis: real estate's advantages are real, but "low risk" depends entirely on buying right and holding through cycles.

Master Criteria, Terms, and Network: what, how, and who

The Dynamic Trio of investing. Keller distills all real estate investing into three focus areas. Criteria define what you buy: the non-negotiable facts like location, type, and price range that filter opportunities and identify predictable value. Terms define how you buy it: the negotiable elements like price, down payment, interest rate, and closing costs that turn an opportunity into a profitable deal. Network defines who helps you: the agents, contractors, lenders, and mentors who provide leverage.

The sequence matters. Criteria identify potential deals, Terms determine the real ones, and your Network supports them all. As investor Dyches Boddiford put it, deals are not found, they are made. You make your money going in, by buying right, not by hoping the market rescues a bad purchase later.

Reducing a complex domain to three variables is the mark of useful expertise, mirroring how chess masters chunk board positions into patterns rather than tracking individual pieces. The insistence that profit is locked in at purchase, not at sale, inverts the amateur's hope-driven mindset and aligns with Warren Buffett's "margin of safety" inherited from Benjamin Graham. What elevates this trio is that Network was a surprise discovery for the authors. The lone-wolf investor is a myth. Behavioral research on weak ties and social capital confirms that opportunity flow correlates strongly with relationship breadth, making the people dimension less sentimental and more mechanically central than most investing guides admit.

Be a shopper, not a buyer: never compromise your criteria

The Five Laws of Lead Generation. Finding deals is a numbers game where, as Keller says, the quality is in the quantity. His laws govern the hunt: never compromise (only pursue properties meeting your Criteria and sellers meeting your Terms), be a shopper not a buyer (better to miss a good one than buy a bad one), timing matters (aim to be the first or last to make an offer), it is a numbers game, and be organized and systematic.

Experienced investors follow a 30:10:3:1 ratio: of 30 properties worth a look, 10 warrant serious investigation, 3 deserve offers, and 1 becomes a deal. Beginners may need to examine three to five times as many. A buyer always leaves the store with something. A shopper happily walks away empty-handed.

The shopper-versus-buyer distinction is a quietly profound piece of emotional engineering. It reframes saying no as success rather than failure, neutralizing the action bias that pushes novices into mediocre deals just to feel productive. The 30:10:3:1 funnel resembles sales pipeline math and venture capital deal flow, where elite firms reject 99% of pitches. The discipline of celebrating rejection runs counter to human loss aversion and the sunk-cost fog that descends after weeks of searching. One practical tension: the "never compromise" rule assumes you can reliably distinguish a great deal from a merely good one, a judgment that itself requires the volume of looking the laws prescribe.

Buy It Right, Pay It Down, Pay It Off to build real wealth

Two engines drive real estate wealth. Equity Buildup grows your net worth through two forces: price appreciation and debt paydown (your tenants' rent retiring your mortgage). Cash Flow Growth provides unearned income when rent exceeds all costs. Keller's motto sequences the journey: buy it right (lock in profit and a margin of safety going in), pay it down (accelerate equity), and pay it off (unleash full cash flow once the mortgage vanishes).

His multiyear model shows the power. Starting in 1983, buying one median-priced home at a 20% discount with 20% down every two years, then annually, an investor could turn $271,800 in down payments into over $1.6 million in equity within 20 years, plus $303,000 in accumulated cash flow. Equity is what matters most.

The model's elegance is that it requires no genius, only consistency and patience, which is both its strength and its vulnerability. It assumes steady 5% appreciation, reliable tenants, and the discipline to keep acquiring for two decades, conditions that real life interrupts with vacancies, repairs, recessions, and personal emergencies. The footnote acknowledgment that the model ignores depreciation tax benefits and income tax liabilities is honest. What the framework captures beautifully is the compounding flywheel: cash flow funds the next down payment, which generates more cash flow. This is the same self-reinforcing loop behind dividend reinvestment, just amplified by leverage and a tenant paying your debt.

Pick one niche, master it, and resist chasing shiny strategies

Niche to get rich. Once you find a working strategy, Keller warns against abandoning it out of boredom, greed, or the lure of a faster scheme. He frames the dilemma as Stick or Switch. Repetition is the mother of mastery, and switching strategies throws you back to the bottom of the learning curve as a novice making novice mistakes.

Investors who specialize, whether in single-family homes, foreclosures, or a specific neighborhood, develop the speed and pattern recognition to spot deals others miss. Keller invokes the learning curve: long flat stretches of effort before a sudden zone of accelerated skill. Most quitters abandon ship just before that breakthrough. The investors he profiles, like Don DeRosa who mastered one acquisition method before learning a second, built fortunes through focused repetition.

The advice to specialize before diversifying aligns with the deliberate-practice research of Anders Ericsson, where expertise emerges from focused repetition on a narrow domain rather than scattered dabbling. The learning curve description, with its frustrating plateau before breakthrough, matches what skill-acquisition researchers call the "latency period." There is genuine wisdom in warning against strategy-hopping, which often masks the discomfort of grinding through the plateau. A counterpoint: over-specialization carries concentration risk, as the investors who only knew apartments during the 1986 Tax Reform Act discovered. The sophisticated position, which the book gestures toward, is to master one niche deeply, then add adjacent competencies deliberately rather than reactively.

Hold money accountable: dead, safe, healthy, or wealthy

Money must earn its wages. Keller's mentor Michael called idle bank savings "dead money" because you cannot reach independence with capital that earns less than inflation. Keller grades money by its return: dead (4% or less, below inflation), safe (5 to 8%), healthy (9 to 12%), and wealthy (above 12%). Money, like a worker, should be gainfully and well employed.

This insight drives a key behavior: tracking both ROI (return on your initial investment) and ROE (return on your total accumulated equity). As equity builds in a property, ROE naturally declines even as the dollars grow. That is why savvy investors refinance to pull equity out and redeploy it into new properties, keeping all their capital working at high wages. They typically maintain a 40% equity position rather than letting money sit idle.

The four-tier vocabulary turns an abstract concept (opportunity cost) into something visceral. Calling savings "dead money" reframes the comfortable default of hoarding cash as an active loss, which is precisely how inflation operates on idle capital. The ROI-versus-ROE distinction is genuinely sophisticated and under-appreciated by casual investors, who fixate on cash returns while trapped equity quietly underperforms. The refinancing strategy, however, embodies the leverage double-edge again: continually pulling equity out maximizes returns in rising markets but leaves thin cushions when values fall. The 40% equity target reads as a reasonable middle path between the safety of full ownership and the aggression of maximum leverage.

Reach the 7th Level: hire a CEO so money works without you

From I do it to they do it. The ultimate destination Keller calls Receive a Million: generating $1 million in annual unearned income while stepping out of daily operations. Getting there means climbing seven levels of people leverage, progressing from doing everything yourself, to contracting your Work Network, to hiring employees, and finally to installing a CEO who runs the business for you.

Investor 34 exemplifies it. Starting on savings and credit cards at a kitchen table, he and his wife reinvested $100 and $150 profits into apartments and storage, eventually netting over $12 million annually, that is $1 million a month, while working roughly 20 hours a week. The goal of wealth, Keller insists, ends in distribution: money is good for the good it can do, so receive more than you need and give the rest.

The seven-level progression mirrors Michael Gerber's E-Myth insight that entrepreneurs must work on the business rather than in it, and the final handoff to a CEO is where most owner-operators stumble, unable to relinquish control. Keller's honesty about the transition, that no successor will initially match your skill yet may eventually exceed it, reflects real founder psychology documented in succession research. The closing pivot from accumulation to philanthropy gives the wealth-building project a moral telos that distinguishes it from pure self-interest. The framework's limit is that genuine passive income at this scale requires building an actual operating business, not merely owning rentals, a leap many investors neither want nor reach.

Analysis

The Millionaire Real Estate Investor occupies a specific niche in personal-finance literature: it is a framework-driven business book disguised as a motivational one, built atop interviews with more than 100 self-made investors and Keller's own experience founding the largest real estate franchise in North America. Its central thesis is that wealth-building is a learnable, modelable discipline, not a matter of luck, genius, or timing. The book's structure mirrors a journey through four stages (Think, Buy, Own, Receive), each progressively more technical, which makes the early chapters accessible to novices while the later worksheet-heavy sections serve serious practitioners.

The work's enduring strength is its psychological architecture. Before teaching a single tactic, Keller spends extensive effort dismantling limiting beliefs (the MythUnderstandings) and installing an investor identity. This sequencing reflects sound behavior-change science: tactics fail without an enabling mindset. His coined frameworks (the Money Matrix, the Dynamic Trio of Criteria-Terms-Network, the Five Laws, the four conditions of money) are mnemonically sticky and genuinely clarifying.

The book's blind spot, glaring in hindsight, is risk. Published in 2005 at the peak of a housing bubble, it presents leverage as nearly costless and real estate as exceptionally stable, citing pre-crash volatility data. The 2008 collapse vindicated the cautious investors Keller profiles (those who bought right, held positive cash flow, and kept reserves) while devastating the over-leveraged speculators he warns against. So the book contains its own corrective, but readers must heed the caveats, not just the inspiring compounding math.

Methodologically, the reliance on millionaire interviews introduces survivorship bias: we learn what winners did, not the base rate of failure among imitators. Still, the principles (buy below market, prioritize cash flow, specialize, build a network, hold long-term) are robust across cycles. The book is best read as a disciplined operating philosophy rather than a guarantee, valuable precisely for the patience and rigor it demands of an asset class that rewards both.

Review Summary

The Millionaire Real Estate Investor receives mixed reviews, with many praising its comprehensive approach to real estate investing and mindset development. Readers appreciate the practical advice, models, and strategies provided. Some find it motivational and credit it for their success. Critics argue it's outdated, overly positive, and lacks specific details. The book is recommended for beginners but may be too basic for experienced investors. Many readers value the emphasis on financial planning, networking, and long-term wealth building through real estate.

People Also Read

Glossary

MythUnderstandings

Self-limiting beliefs blocking wealthKeller's coined term combining myth and misunderstanding for the eight common false beliefs that stop people from investing. Three concern self-image (my job will make me wealthy, I do not need wealth, I cannot do it) and five concern investing itself (it is complicated, requires rare knowledge, is risky, demands market timing, all good deals are taken). Each is dismantled as a fear masquerading as fact.

Criteria, Terms, Network (CTN)

The three investing focus areasKeller's Dynamic Trio of investing. Criteria are the non-negotiable facts defining what you buy (location, type, price). Terms are the negotiable elements defining how you buy it (price, down payment, financing, closing costs). Network is who helps you (agents, lenders, contractors, mentors). Criteria identify deals, Terms make them profitable, and Network supports everything.

Money Matrix

Four roles every dollar playsA model sorting money into four uses: Capital (invested to grow in value), Cash Flow (income generated by investments), Cash (reserves held for security), and Consumption (spending on things that do not appreciate). Investors prioritize Capital first; consumers prioritize Consumption first, which explains why the rich get richer and the poor stay poor.

Shadow Wealth

Appearance of wealth without assetsKeller's term for a lifestyle that looks prosperous (big house, nice car) but rests on consumption rather than income-producing assets. People living in Shadow Wealth may have high salaries yet no Capital foundation, leaving them perpetually one job loss away from financial distress despite outward signs of success.

Equity Buildup and Cash Flow Growth

Two engines of real estate wealthThe two ways real estate creates wealth. Equity Buildup increases net worth through price appreciation plus debt paydown (rent retiring the mortgage). Cash Flow Growth provides unearned income when rental income exceeds all costs including vacancy, expenses, and mortgage. Both can occur simultaneously, and reinvesting cash flow accelerates equity.

Buy It Right, Pay It Down, Pay It Off

The wealth-building mottoKeller's mantra for the Buy and Hold strategy. Buy It Right means purchasing below market value to lock in profit and a margin of safety going in. Pay It Down means accelerating equity through mortgage reduction. Pay It Off means owning free and clear, which maximizes net cash flow once the loan disappears.

30:10:3:1 Ratio

Experienced investor deal funnelThe lead-generation funnel of seasoned investors: for every 30 properties worth examining (suspects), about 10 warrant serious investigation (prospects), 3 are worth an offer, and 1 becomes an actual deal. Beginners typically must examine three to five times as many properties to find one deal, reinforcing that finding deals is a numbers game.

The 7th Level

Hiring a CEO replacementThe final stage of building an investment business, where the owner hires a CEO to run daily operations, achieving total people leverage. The progression moves through seven levels from doing everything yourself, to contracting help, to hiring employees in Acquisition/Disposition, Administration, and Operations, until the owner works on the business a few hours weekly rather than in it.

Four Conditions of Money

Grading returns: dead to wealthyKeller's classification of invested money by its rate of return relative to inflation. Dead money earns 4% or less (below inflation), Safe money 5 to 8%, Healthy money 9 to 12%, and Wealthy money above 12%. The principle: money should be gainfully and well employed, never left idle earning less than inflation.

Big Why

Deep motivation powering achievementKeller's term, drawn from Napoleon Hill, for the compelling personal reason that drives sustained action toward wealth. A true Big Why shifts thinking from wants (electives) to needs (imperatives), supplying the stamina and focus required for long-term financial success. The most powerful Big Whys relate to reaching one's highest potential rather than material goals.

FAQ

What's The Millionaire Real Estate Investor about?

- Wealth Building Focus: The book emphasizes achieving financial independence through real estate investing, presenting it as an accessible path for those willing to learn and apply proven strategies.

- Mindset and Models: It combines the art of thinking big with the science of using effective models, guiding readers through necessary mindset shifts and practical steps to become successful investors.

- Real-Life Examples: Gary Keller shares insights from over 100 successful real estate investors, illustrating their experiences and the models they used to achieve financial independence.

Why should I read The Millionaire Real Estate Investor?

- Proven Strategies: The book provides actionable advice and proven models that can help both novice and experienced investors navigate the real estate market effectively.

- Overcoming Fear: It addresses common fears and misconceptions about investing, empowering readers to take the first steps toward building wealth without being paralyzed by doubt.

- Comprehensive Framework: Offers a structured approach to real estate investing, breaking down complex concepts into manageable parts, making it easier for readers to understand and implement.

What are the key takeaways of The Millionaire Real Estate Investor?

- Three Areas of Focus: Highlights the importance of Criteria (what you buy), Terms (how you buy it), and Network (who helps you) as essential components for successful investing.

- Four Stages of Growth: Outlines a progression through four stages: Think a Million, Buy a Million, Own a Million, and Receive a Million, each representing a step toward financial wealth.

- Mindset Shift: Encourages adopting a millionaire mindset, focusing on long-term goals and the value of real estate as a wealth-building tool.

What are the best quotes from The Millionaire Real Estate Investor and what do they mean?

- “Money lives on the other side of fear.”: Emphasizes that overcoming fear is essential to achieving financial success; many opportunities are lost due to hesitation.

- “Anyone can do it—not everyone will.”: Highlights the accessibility of real estate investing while acknowledging that success requires commitment and action from the individual.

- “Buy it right—pay it down—pay it off.”: Encapsulates the core strategy for building wealth through real estate, stressing the importance of making wise purchases and managing debt effectively.

What is the Money Matrix in The Millionaire Real Estate Investor?

- Understanding Financial Priorities: Distinguishes between Capital (invested money), Cash Flow (income generated), Cash (money held), and Consumption (spending), helping readers prioritize financial decisions.

- Investor vs. Consumer: Contrasts the mindset of investors, who focus on building wealth through Capital, with consumers, who prioritize spending, illustrating the importance of making investment a priority.

- Path of Money: Serves as a guide for directing money toward investments rather than consumption, emphasizing that successful wealth building requires intentional financial choices.

How do I establish my Criteria for real estate investing according to The Millionaire Real Estate Investor?

- Define Your Goals: Start by identifying what type of properties you want to invest in, considering factors like location, property type, and economic conditions that align with your financial goals.

- Be Specific: Create a detailed description of your ideal investment property, including aspects like price range, desired features, and any necessary conditions, to help filter potential opportunities.

- Adapt Over Time: As you gain experience and market knowledge, be prepared to refine your Criteria to better reflect your evolving investment strategy and goals.

What are the Four Stages of Growth outlined in The Millionaire Real Estate Investor?

- Think a Million: Focuses on developing a millionaire mindset, emphasizing the importance of big thinking and setting ambitious financial goals.

- Buy a Million: Investors learn to acquire properties worth a million dollars or more, applying the models and strategies discussed in the book.

- Own a Million: Involves building a portfolio with a million dollars or more in equity, requiring effective management and strategic decision-making.

- Receive a Million: About generating a million dollars in annual cash flow from investments, allowing for financial independence and the ability to enjoy the fruits of one’s labor.

How can I build my Network as a real estate investor according to The Millionaire Real Estate Investor?

- Identify Key Players: Connect with professionals in the real estate industry, such as agents, lenders, and contractors, who can provide valuable insights and support for your investment journey.

- Engage Regularly: Maintain consistent communication with your network through calls, emails, and meetings to build strong relationships and ensure they think of you when opportunities arise.

- Leverage Referrals: Encourage your network to refer potential leads and investment opportunities, and be sure to reciprocate by providing value to them in return.

What is the Lead Generation Model in The Millionaire Real Estate Investor?

- Finding Opportunities: Focuses on generating leads to find investment opportunities that meet your established criteria, encouraging proactive marketing and networking to attract motivated sellers.

- Qualifying Leads: Emphasizes the importance of qualifying leads to distinguish between suspects and prospects, ensuring that time is spent on viable opportunities.

- Five Laws of Lead Generation: Outlines five laws—never compromise, be a shopper, timing matters, it’s a numbers game, and be organized—that guide effective lead generation efforts.

How do I Buy it Right according to The Millionaire Real Estate Investor?

- Market Research: Conduct thorough research to understand property values and market conditions, ensuring you can identify undervalued properties that meet your Criteria.

- Negotiate Terms: Focus on negotiating favorable terms that enhance your equity position and cash flow, such as lower purchase prices, favorable financing, and contingencies that protect your investment.

- Evaluate Risks: Assess the potential risks associated with each investment, including market fluctuations and property conditions, to ensure you are making informed decisions that align with your financial goals.

What is the Acquisition Model in The Millionaire Real Estate Investor?

- Buying Right: Emphasizes the importance of making money on the purchase by ensuring that properties are acquired at a discount or favorable terms, setting the foundation for future profitability.

- Two Fundamental Strategies: Outlines two main acquisition strategies: buying for cash and buying for cash flow and equity buildup, allowing investors to choose the approach that aligns with their goals.

- Use of Worksheets: Provides worksheets to help investors analyze potential deals, ensuring that all financial aspects are considered before making an offer.

How can I maximize my net operating income (NOI) as suggested in The Millionaire Real Estate Investor?

- Increase Rental Income: Focus on strategies to increase gross rental income, such as implementing rent escalators, making property improvements, and targeting higher-paying tenants.

- Control Operating Expenses: Keep a close eye on expenses and implement cost-saving measures to improve your NOI. Regularly review your financials to identify areas for potential savings.

- Minimize Vacancies: Develop a proactive marketing strategy to minimize vacancies and ensure quick tenant turnover, including maintaining good relationships with current tenants and addressing their needs promptly.

About the Author

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.