Key Takeaways

Doing well with money is behavior, not brainpower or math

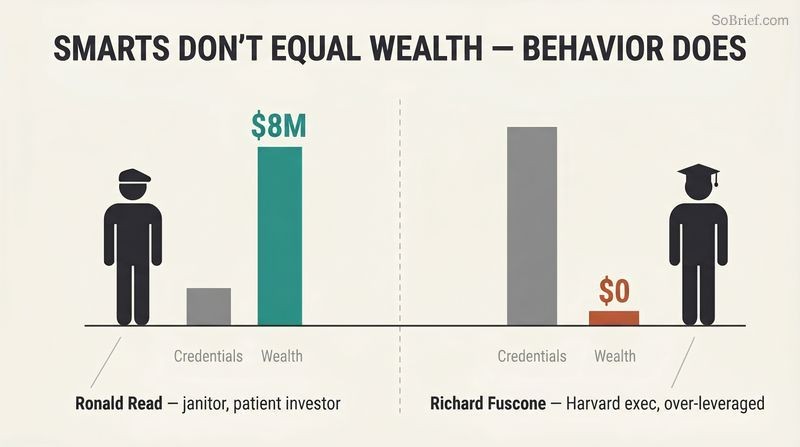

Smarts don't equal financial wisdom. Ronald Read, a Vermont janitor and gas station attendant who fixed cars for 25 years, died with over $8 million by quietly buying blue-chip stocks and waiting decades. Meanwhile Richard Fuscone, a Harvard-educated Merrill Lynch executive, went bankrupt in the 2008 crisis after borrowing heavily to expand a mansion that cost $90,000 a month to maintain.

Finance is a soft skill. No janitor outperforms a heart surgeon, but in investing the untrained routinely beat the credentialed. Money is taught like physics, with formulas and laws, when it actually behaves like psychology, full of emotion and nuance. A genius who panics is a financial disaster; an ordinary person with patience and discipline can quietly build a fortune.

What's striking is how this reframes financial education itself. Behavioral economists like Richard Thaler and Daniel Kahneman spent careers proving that humans systematically deviate from the rational actor of classical economics, yet most personal finance curricula still teach optimization rather than self-regulation. The Read versus Fuscone contrast echoes research on the marshmallow test and delayed gratification, where temperament predicts outcomes better than IQ. One caveat: survivorship is real. For every patient Ronald Read, others saved diligently and still got crushed by bad timing or medical catastrophe. Behavior tilts the odds powerfully, but it does not fully neutralize luck, a tension the book itself wrestles with honestly.

Nobody is crazy with money; everyone plays a different game

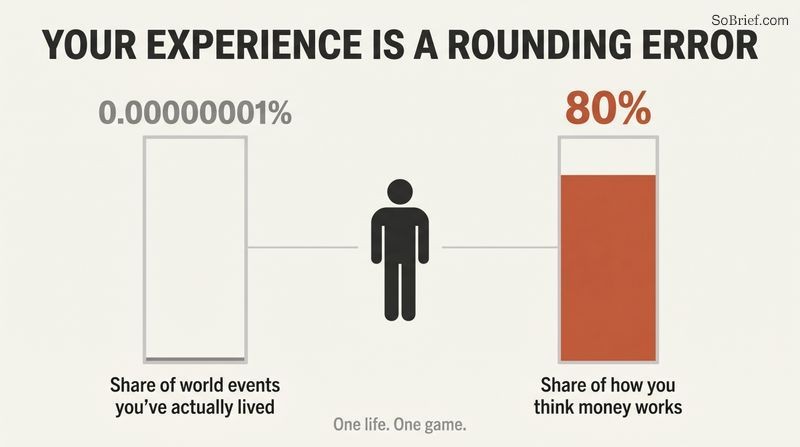

Your experience is a rounding error. Your personal history with money is maybe 0.00000001% of what has happened in the world, yet it shapes roughly 80% of how you think the world works. Someone who came of age during high inflation invests differently than someone raised in stable prices. Economists Malmendier and Nagel found investors anchor lifelong risk-taking to the markets they witnessed in early adulthood, not to logic.

Seemingly insane choices have hidden logic. The poorest American households spend about $412 a year on lottery tickets, four times what the richest spend, even though 40% of Americans cannot cover a $400 emergency. Cruel? Maybe. But for someone with no path to the comforts finance readers take for granted, a ticket is the only affordable dream. Every money decision makes sense to the person making it in that moment.

This is empathy as analytical tool, and it dovetails with cultural psychology research showing that risk preferences are not fixed traits but products of environment and scarcity. Studies on scarcity by Sendhil Mullainathan and Eldar Shafir show that financial deprivation taxes cognitive bandwidth, making the lottery purchase less irrational than it appears. The deeper point is humility: judging others' money choices without their context is like critiquing a film you walked into halfway through. A useful challenge, though, is that understanding why a behavior occurs does not make it wise. The book grants this, urging compassion without endorsing self-sabotage.

Respect luck and risk as twins behind every outcome

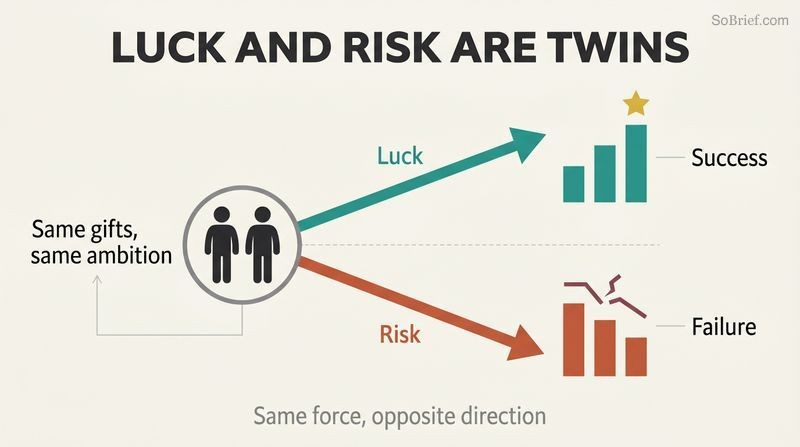

Bill Gates had one-in-a-million luck. In 1968 his school, Lakeside, was one of perhaps a handful on Earth with a computer. Gates himself said that without Lakeside there would have been no Microsoft. His equally brilliant friend Kent Evans, who shared the same gifts and ambition, died in a mountaineering accident before graduating. Same magnitude of force, opposite direction.

We misjudge both. When judging others' success we credit skill; when judging our own failure we blame risk. Nobel economist Robert Shiller said what he most wants to know is the exact role of luck in success. Housel's advice: be careful who you praise and who you scorn, and study broad patterns rather than extreme individuals, since the most extreme outcomes are the least repeatable and the most luck-soaked.

This maps neatly onto fundamental attribution error in social psychology, where observers overweight character and underweight circumstance. Nassim Taleb's Fooled by Randomness makes the parallel argument that markets manufacture lucky fools indistinguishable from geniuses until the tide turns. The practical genius here is the prescription to study patterns over personalities. Warren Buffett is nearly impossible to emulate because his result sits so far in the tail that luck's contribution is high and unmeasurable. A broad finding like people with control over their time are happier is more reliably actionable. The honest difficulty, which the author concedes, is that we cannot cleanly separate the skill from the dice.

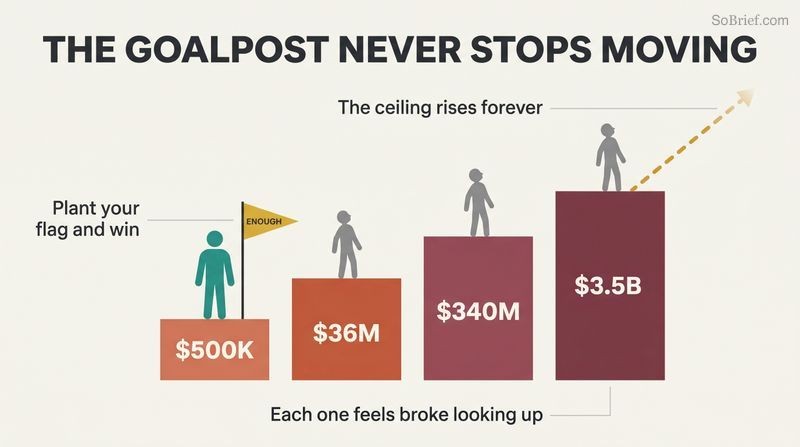

Get the goalpost to stop moving or wealth destroys you

Enough is the rarest financial skill. Rajat Gupta, who rose from a Kolkata orphanage to run McKinsey and sit on Goldman's board, was worth $100 million yet committed insider trading chasing billionaire status. Bernie Madoff ran a legitimate market-making firm earning tens of millions a year before the Ponzi scheme. Both threw away everything because they had no sense of enough.

Social comparison is a war you can't win. A $500,000 rookie feels broke next to a teammate earning $36 million, who feels modest next to hedge fund managers earning $340 million, who look up at Buffett gaining $3.5 billion a year. The ceiling rises forever. Happiness is results minus expectations. Reputation, freedom, family, and being loved are not worth risking for things you do not need.

The Vonnegut and Heller anecdote that opens the chapter, where a novelist tells a hedge fund billionaire he has something the rich man never will, namely enough, distills an ancient Stoic and Epicurean insight into a single word. Modern hedonic adaptation research confirms the mechanism: lottery winners and the newly promoted return to baseline happiness as expectations recalibrate upward. What the book adds is the asymmetry of ruin. Gupta and Madoff illustrate that insatiability is not merely unsatisfying but actively dangerous, because chasing the marginal dollar eventually demands betting things that are irreplaceable. The skill is psychological, not mathematical, and almost nobody is taught it.

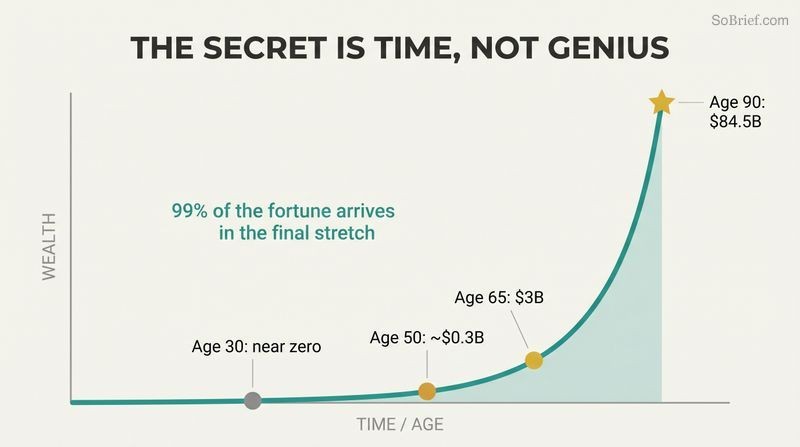

Compounding's secret isn't big returns, it's absurd time horizons

Buffett's edge is longevity, not genius. Of Warren Buffett's roughly $84.5 billion, about $84.2 billion was accumulated after his 50th birthday, and $81.5 billion after his mid-60s. Had he started investing at 30 and retired at 60 with normal returns, he would be worth around $11.9 million, 99.9% less. His skill is investing; his real secret is investing consistently for three-quarters of a century.

Linear brains underestimate exponential growth. Ice ages form not from massive force but from a thin layer of summer snow that simply lasts, reflecting sunlight and compounding into miles-thick sheets. Money works the same way. The most powerful investing book, Housel jokes, would be titled Shut Up And Wait, a single page with a long-term growth chart. Good returns sustained uninterrupted beat spectacular returns that cannot be repeated.

The cognitive science is real: humans reason linearly because ancestral environments rarely featured exponential dynamics, which is why people misjudged early pandemic spread and why Bill Gates once doubted anyone needed a gigabyte of email storage. The Jim Simons comparison is the sharpest blade in the chapter. Simons compounded at 66% annually, triple Buffett's 22%, yet is far less wealthy simply because he started decades later. This reframes the entire industry's obsession with maximizing annual returns as a category error. The quiet implication, worth sitting with, is that boring consistency and a long runway matter more than brilliance, which is unflattering to the heroic stock-picker mythology.

Survive first; ruin erases every future opportunity to compound

Getting rich and staying rich are opposite skills. Jesse Livermore made the equivalent of $3 billion in a single day shorting the 1929 crash, then grew overconfident, made bigger bets, lost everything, and took his own life. Getting money takes optimism and risk; keeping it takes frugality, paranoia, and the humility to admit luck played a role.

Plan on the plan not working. Of companies successful enough to go public, 40% eventually lose essentially all their value. Rick Guerin, Buffett and Munger's equally talented third partner, was forced to sell his Berkshire shares during the 1973 to 1974 crash because he used leverage and was in a hurry. The fix is a barbelled mind: optimistic about the long arc, paranoid about the landmines in between. Margin of safety keeps you in the game.

Taleb's barbell strategy and his maxim that you must avoid ruin at all costs sit at the center here, and the math backs it. Because compounding requires uninterrupted time, a single wipeout is not a setback but a reset to zero, forfeiting the asymmetric upside entirely. This connects to ergodicity economics, the argument by Ole Peters that what matters is not the average outcome across many parallel players but the trajectory of the single player who cannot replay a blown-up life. The cash-during-a-bull-market example is psychologically astute: holding dry powder feels like leaving money on the table, yet preventing one panicked sale can outweigh dozens of winning picks.

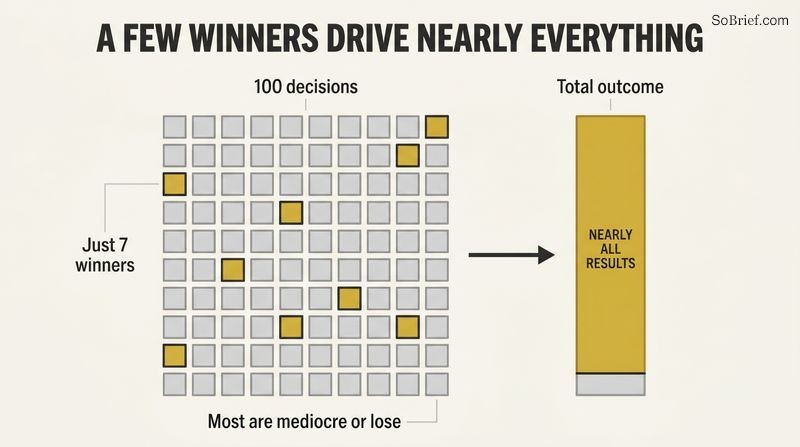

A tiny handful of decisions drive nearly all your results

Tails dominate everything. Art dealer Heinz Berggruen bought masterpieces in bulk like an index fund; 99% may have been mediocre, but a few Picassos made the collection worth over a billion. Of the Russell 3000 stocks since 1980, 40% lost at least 70% and never recovered, while just 7% of components drove effectively all the index's gains. Walt Disney made hundreds of cartoons that lost money before Snow White's 83 minutes transformed the company.

You can be wrong half the time and still win. Peter Lynch said great investors are right 6 times out of 10. Buffett owned 400 to 500 stocks but made most of his money on 10. The lesson extends to behavior: Sue, who invested through every recession from 1900 to 2019, ended with $435,551, far more than investors who fled downturns.

This is the power-law worldview, and it generalizes far beyond finance, from venture capital where one investment can return an entire fund, to scientific careers, to the box office. The Chris Rock detail, where the polished Netflix special is the surviving tail of hundreds of fumbled small-club sets, is a vivid reminder that we only ever see finished products, never the failure-strewn process behind them. The cross-disciplinary echo is Pareto and Mandelbrot's fractal markets. One nuance worth flagging: diversified index investing harnesses tails safely, but concentrated tail-hunting in individual stocks exposes ordinary investors to the 40% that go to zero. The strategy that captures tails matters enormously.

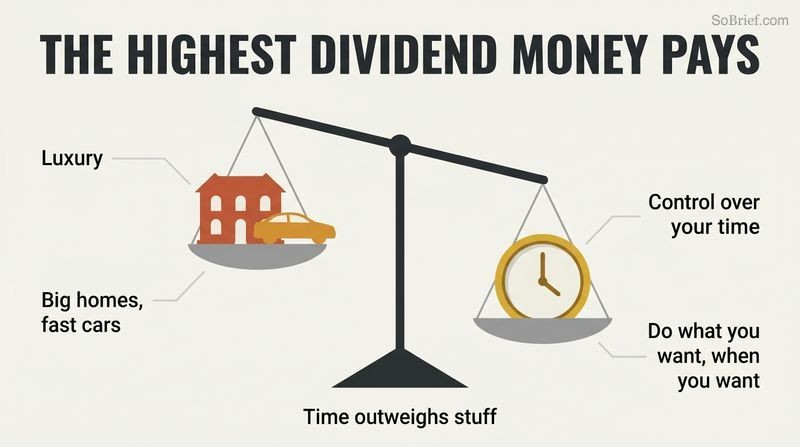

Money's highest dividend is control over your own time

Autonomy beats luxury for happiness. Psychologist Angus Campbell found that a strong sense of controlling one's life predicts wellbeing better than income, house size, or job prestige. The ability to do what you want, when you want, with whom you want, is the highest dividend money pays. Housel quit a prestigious investment banking internship in a month because doing work he loved on a schedule he could not control felt like work he hated.

Modern jobs never clock out. Entrepreneur Derek Sivers said the moment that made him free was saving $12,000 in his twenties, not selling his company later. Yet Americans are no happier than in the 1950s despite far bigger homes and faster cars, because knowledge work, like John D. Rockefeller's thinking, follows us home. We bought stuff and surrendered time.

Self-determination theory, developed by Edward Deci and Richard Ryan, independently identifies autonomy as one of three core psychological needs alongside competence and relatedness, lending robust empirical scaffolding to Campbell's finding. The concept of reactance, our instinctive rebellion against losing control, explains why even beloved work becomes misery on someone else's schedule. Karl Pillemer's interviews with a thousand elderly Americans, none of whom said working harder for money was the path to happiness, function as a kind of deathbed regret study echoing palliative nurse Bronnie Ware's findings. The subtle modern twist, that smartphones turned the workday into the whole day, deserves more attention than productivity culture gives it.

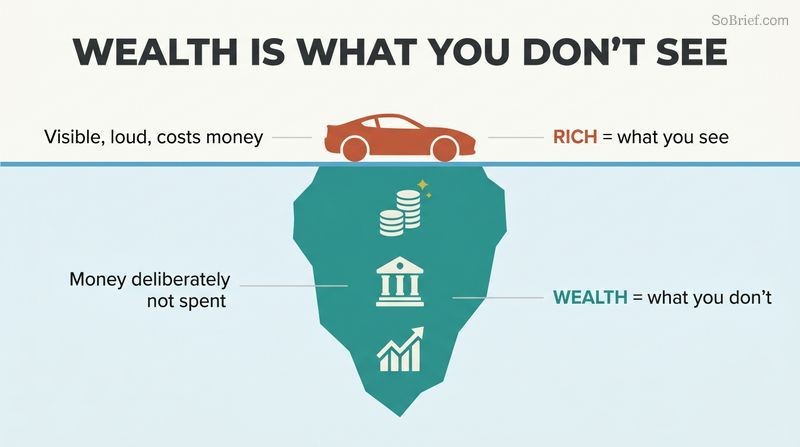

Wealth is the spending you don't see, not the spending you do

Rich and wealthy are opposites. Rich is current high income, the $100,000 car and the big house, which is loud and visible. Wealth is income deliberately not spent: the car not bought, the upgrade declined, financial assets that have not been converted into stuff. The only data point a Ferrari gives you is that the owner has $100,000 less than before, or more debt.

The Man in the Car Paradox. People buy flashy things believing others will admire them, but onlookers admire the car while ignoring the driver, mentally placing themselves behind the wheel. Wealth is hidden by definition, which makes it nearly impossible to learn by imitation. Ronald Read became a role model only after death, because in life every penny of his fortune was invisible. The way to be wealthy is simply to not spend the money you have.

The distinction cuts against a multibillion-dollar signaling economy. Thorstein Veblen named conspicuous consumption over a century ago, and Robert Frank's work on luxury fever shows how positional spending traps entire societies in arms races that raise costs without raising satisfaction. Housel's sharpest move is epistemological: because wealth is unseen, we lack role models for it, the way an aspiring writer who could not read great books would struggle. The diet analogy, where being rich is the workout and being wealthy is declining the reward meal, is memorable and accurate. One could push further: social media has made the invisibility problem worse, broadcasting only the consumption and never the restraint.

Savings rate, not income or returns, builds your wealth

Frugality is the controllable variable. Just as the world solved the 1970s oil crisis mostly through efficiency (the US uses about 60% less energy per dollar of GDP than in 1950) rather than finding more oil, you build wealth by needing less, not earning or returning more. Returns are uncertain and out of your control; your savings rate is 100% in your hands.

Savings is the gap between ego and income. Past a basic level, spending is mostly showing others you have money. Raise your humility and you raise your savings. You don't need a specific goal to save; savings without a purpose is a hedge against life's inevitable surprises and a down payment on flexibility. In a hyper-connected world where being smart is no longer rare, flexibility, the ability to wait for opportunity, is the durable edge.

This quietly demolishes the financial media's fixation on returns. The arithmetic is unforgiving: professionals grind 80-hour weeks to add a tenth of a percentage point while ignoring two or three points of lifestyle bloat that require no market cooperation. Behavioral research on the hedonic treadmill supports the ego-versus-income framing, since spending to impress yields fleeting status gains. The forward-looking argument is sharp and underappreciated: as globalization and software flatten the value of raw intelligence, optionality becomes the scarce asset, echoing labor economists who note that adaptability now outpaces credentials. The unmeasurable return on cash, the freedom to say no, is precisely what spreadsheets ignore and therefore what people undervalue.

Aim to be reasonable, not coldly rational, with money

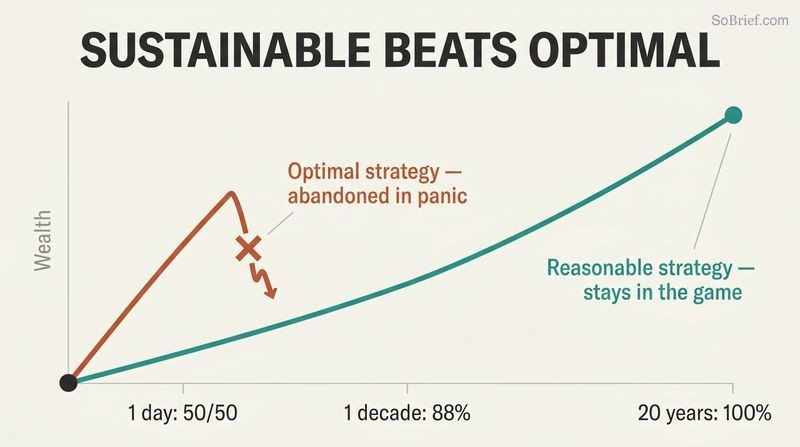

Sustainable beats optimal. A rational strategy you abandon in panic is worse than an imperfect one you stick with. Nobel laureate Harry Markowitz, who won for mathematically optimizing risk and return, split his own portfolio 50/50 between stocks and bonds simply to minimize future regret. Loving your investments, having home-country bias, or keeping a little money for individual stock-picking are technically suboptimal but reasonable, because they keep you in the game.

The fever analogy. Fevers actually help fight infection, slowing some viruses 200-fold, yet we universally suppress them because they hurt. It may be rational to want a fever, but it is not reasonable. Money is the same. The historical odds of making money in US stocks rise from 50/50 over a day to 88% over a decade to 100% over 20 years, so anything that keeps you invested has a quantifiable edge.

This is a genuinely contrarian stance against the optimization ethos that dominates quantitative finance. The malariotherapy story, where a doctor cured syphilis by inducing fever and won a Nobel, is a brilliant vehicle for the rational-versus-reasonable distinction. It connects to the literature on robust versus optimal decision-making, where engineers favor designs that tolerate imperfect conditions over those that maximize performance under ideal ones. The leveraged-retirement study, mathematically superior yet psychologically unbearable since no human calmly rebuilds after a total wipeout, exposes the gap between paper and people. The deeper claim is that emotional sustainability is itself a quantifiable financial input, not a weakness to engineer away.

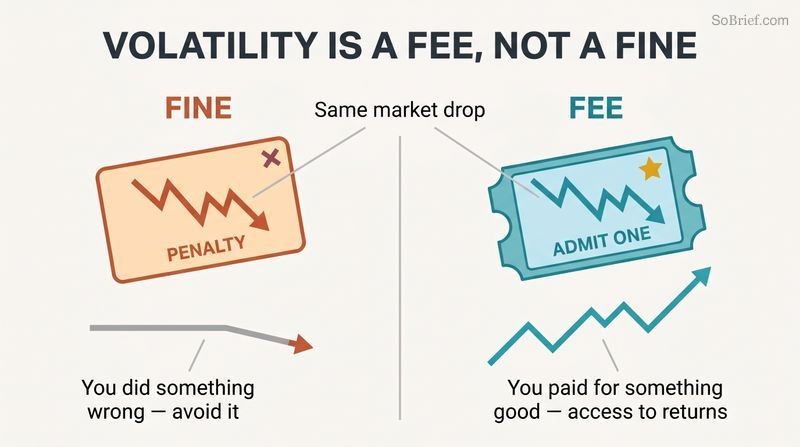

Treat market losses as a fee for entry, not a fine for error

Returns demand payment in volatility. The Dow returned about 11% annually from 1950 to 2019, but the price was relentless: stocks spent enormous stretches well below previous highs. Netflix returned over 35,000% from 2002 to 2018 yet traded below its prior peak on 94% of days. There is no toll-free road to high returns.

Fee versus fine mindset. A fine means you did something wrong and should avoid it; a fee means you paid for something good, like a Disneyland ticket. Investors who treat volatility as a fine try to dodge it by timing the market, and usually pay double. Morningstar found that of 112 tactical funds designed to sidestep downturns, only nine beat a simple 60/40 fund. Jack Welch's GE smoothed earnings by pulling future gains forward, and shareholders eventually paid the deferred bill in full. Find the price, then pay it willingly.

The reframe is more than semantic. Loss aversion, Kahneman and Tversky's finding that losses sting about twice as much as equivalent gains feel good, is precisely what makes volatility register as punishment rather than purchase. By relabeling the experience as a fee, the book performs a cognitive reappraisal, a technique clinical psychology uses to defuse anxiety. The GE and Freddie Mac earnings-smoothing examples are damning: the attempt to deliver returns without the discomfort of uncertainty does not eliminate the cost, it merely defers and compounds it. One honest limit, which the book grants, is that the fee is not always worth it. Sometimes it rains at Disneyland, and some assets never recover.

Analysis

The Psychology of Money is an anthology of twenty loosely linked essays unified by a single thesis: financial success depends far more on behavior, temperament, and emotional self-regulation than on intelligence, formulas, or market knowledge. Morgan Housel, a former columnist who began writing during the 2008 crisis, structures the book as a sequence of vivid parables (a janitor who outsaved a Harvard executive, Gates and his doomed friend, Livermore's rise and ruin) rather than a rigid framework, which makes it memorable but occasionally repetitive. The danger in summarizing it is that its power lives in the stories, not in abstractable principles; strip the anecdotes and you risk reducing rich insight to fortune-cookie maxims. The book sits at the intersection of behavioral economics and Stoic-adjacent life philosophy. Its intellectual lineage runs through Kahneman, Thaler, and Taleb, but Housel's contribution is translation: he renders academic findings into kitchen-table wisdom. His strongest, most original moves are the redefinitions, wealth as the spending you cannot see, savings as the gap between ego and income, volatility as a fee rather than a fine. These reframings perform genuine cognitive work, converting abstract concepts into actionable mental postures.

The book's limitations are worth naming. It is largely silent on systemic constraints, structural inequality, discrimination, and the reality that for many people the savings gap is not a choice but an impossibility, though the closing postscript on the American consumer partially redeems this. The advice is also tilted toward people who already have surplus income to manage. Its survivorship bias is real: counsel patience and frugality and you will produce Ronald Reads, but also unlucky savers crushed by timing. Still, as a corrective to the math-obsessed, return-chasing default of personal finance culture, it is unusually humane, durable, and quietly radical in insisting that the goal of money is not more money but autonomy over one's own time.

Review Summary

The Psychology of Money receives mostly positive reviews for its accessible insights into personal finance and investing psychology. Readers appreciate Housel's simple yet profound lessons on wealth, happiness, and decision-making. Many find the book's emphasis on behavior over intelligence refreshing. Some criticize it for being repetitive or lacking depth for experienced investors. However, most agree it offers valuable perspectives on the relationship between money and personal values, making it particularly useful for those new to financial planning.

People Also Read

Glossary

The psychology of money

Behavior beats knowledge in financeHousel's term for the soft, emotional, and behavioral skills that determine financial outcomes more than technical knowledge or intelligence. It captures the idea that money is not a hard science governed by formulas but a discipline shaped by personal history, ego, fear, and patience, where ordinary people can outperform experts through good behavior.

Enough

Knowing when to stopThe skill of getting the goalposts of desire to stop moving so that ambition does not outrun satisfaction. Housel frames it as the hardest and most protective financial skill, the recognition that an insatiable appetite for more eventually pushes people to risk things that are irreplaceable, like reputation, freedom, and family.

Wealth versus rich

Hidden assets versus visible spendingHousel's distinction: being rich means a high current income spent on visible things like cars and houses, while wealth is income deliberately not spent, financial assets kept as options for the future. Wealth is invisible by definition, which makes it hard to imitate or learn from.

Tails drive everything

Few events create most outcomesThe principle that a small number of outlier events, the long tails of a distribution, account for the majority of results in investing, business, and life. It means you can be wrong most of the time and still succeed enormously if your few winners are large enough.

Room for error (margin of safety)

Buffer that ensures survivalThe gap between what you expect to happen and what could happen, built into a financial plan so you can endure surprises and stay invested long enough for compounding to work. Housel calls it the most underappreciated force in finance; its purpose is to render forecasting unnecessary.

Reasonable over rational

Sustainable beats mathematically optimalHousel's advice to pursue financial strategies you can emotionally stick with rather than ones that are mathematically optimal on paper. Because staying invested over time matters most, a slightly imperfect plan you maintain through fear beats a perfect plan you abandon in panic.

Man in the Car Paradox

Admirers ignore the ownerThe observation that people buy expensive cars hoping to be admired, but onlookers admire the car while ignoring the driver, imagining themselves behind the wheel instead. It illustrates that flashy possessions rarely deliver the respect people actually crave.

Historians as prophets fallacy

Overusing past as future mapHousel's term for the mistake of treating economic and market history as a reliable guide to the future. Because the most important events are unprecedented surprises and because structures constantly change, past data calibrates expectations but cannot predict outcomes.

Appealing fictions

Believing what you desperately wantStories people accept as true because they desperately want them to be true, especially under high stakes and limited control. In money, they explain why investors trust unreliable forecasts and quack predictions: the bigger the gap between what you want and what is real, the more vulnerable you are.

FAQ

What's "The Psychology of Money" about?

- Behavior over intelligence: The book emphasizes that financial success is more about how you behave with money than how smart you are. It highlights the importance of understanding your own financial psychology.

- Stories and experiences: Morgan Housel uses short stories to illustrate how people's unique experiences shape their financial decisions, often leading to different outcomes.

- Soft skills in finance: The book argues that soft skills, like patience and understanding risk, are more crucial than technical financial knowledge.

- Universal lessons: It provides timeless lessons on wealth, greed, and happiness, applicable to anyone regardless of their financial background.

Why should I read "The Psychology of Money"?

- Practical insights: The book offers practical insights into how to manage money wisely by understanding human behavior and psychology.

- Relatable stories: Through relatable stories, it helps readers see the impact of their financial decisions and encourages them to think differently about money.

- Behavioral focus: It shifts the focus from traditional financial advice to understanding the psychological aspects of money management.

- Broad applicability: The lessons are applicable to a wide audience, from those just starting their financial journey to seasoned investors.

What are the key takeaways of "The Psychology of Money"?

- Luck and risk: Success in finance often involves a mix of luck and risk, and understanding this can help manage expectations and decisions.

- Compounding: The power of compounding is a central theme, emphasizing the importance of time in building wealth.

- Room for error: Planning for uncertainty and having a margin of safety is crucial for long-term financial success.

- Personal finance is personal: Financial decisions should be tailored to individual goals and circumstances, rather than following a one-size-fits-all approach.

What are the best quotes from "The Psychology of Money" and what do they mean?

- "A genius is the man who can do the average thing when everyone else around him is losing his mind." - This quote highlights the importance of staying calm and rational during financial turmoil.

- "The world is full of obvious things which nobody by any chance ever observes." - It suggests that many financial truths are overlooked because they are hidden in plain sight.

- "The purpose of the margin of safety is to render the forecast unnecessary." - This emphasizes the importance of planning for uncertainty rather than relying on precise predictions.

- "Nothing is as good or as bad as it seems." - It reminds readers to maintain perspective and avoid overreacting to financial highs and lows.

How does Morgan Housel define wealth in "The Psychology of Money"?

- Wealth is hidden: Wealth is what you don't see; it's the money not spent on visible luxuries but saved and invested for future flexibility and security.

- Options and freedom: True wealth provides options and the freedom to make choices without financial constraints.

- Beyond material possessions: Wealth is not about owning expensive items but having the financial security to live life on your terms.

- Financial independence: The ultimate goal of wealth is to achieve financial independence, allowing you to do what you want, when you want.

What is the "Man in the Car Paradox" in "The Psychology of Money"?

- Admiration misplacement: The paradox suggests that people often buy luxury items like cars to gain admiration, but observers admire the car, not the owner.

- Misunderstanding wealth signals: It highlights the common misconception that visible wealth equates to actual wealth, which is often not the case.

- Focus on respect: True respect and admiration come from qualities like humility and kindness, not material possessions.

- Financial implications: Understanding this paradox can help individuals make more meaningful financial decisions that align with their true values.

How does "The Psychology of Money" explain the role of luck and risk in financial success?

- Luck's impact: The book emphasizes that luck plays a significant role in financial success, often more than skill or intelligence.

- Risk awareness: It highlights the importance of recognizing and respecting risk, as it can lead to unexpected outcomes.

- Balancing both: Successful financial management involves balancing the understanding of both luck and risk in decision-making.

- Avoiding overconfidence: Acknowledging the role of luck helps prevent overconfidence and encourages humility in financial planning.

What does "The Psychology of Money" say about compounding?

- Time's power: Compounding is described as the most powerful force in finance, with time being its greatest ally.

- Early start benefits: Starting early with investments allows compounding to work its magic over decades, leading to significant wealth accumulation.

- Patience required: The book stresses the importance of patience and long-term thinking to fully benefit from compounding.

- Misunderstood concept: Many people underestimate compounding's potential because its effects are not immediately visible.

How does "The Psychology of Money" address the concept of "Enough"?

- Knowing limits: The book discusses the importance of recognizing when you have enough, to avoid unnecessary risks and stress.

- Avoiding greed: It warns against the dangers of constantly moving financial goalposts, which can lead to perpetual dissatisfaction.

- Contentment focus: Emphasizing contentment with what you have can lead to greater happiness and financial stability.

- Risk management: Understanding "enough" helps in managing risks and making more prudent financial decisions.

What does "The Psychology of Money" suggest about financial independence?

- Ultimate goal: Financial independence is portrayed as the highest form of wealth, providing control over one's time and choices.

- Freedom emphasis: It allows individuals to make decisions based on personal values rather than financial necessity.

- Lifestyle alignment: Achieving financial independence often involves aligning lifestyle choices with long-term financial goals.

- Savings importance: A high savings rate and living below one's means are crucial steps toward achieving financial independence.

How does "The Psychology of Money" view the relationship between money and happiness?

- Control over time: The book argues that money's greatest value is in providing control over one's time, which is a key component of happiness.

- Beyond material wealth: Happiness is not directly correlated with material wealth but with the freedom and options money can provide.

- Personal fulfillment: Using money to align with personal values and goals leads to greater fulfillment and satisfaction.

- Avoiding comparison: The book advises against comparing oneself to others, as this can lead to unnecessary stress and dissatisfaction.

What is the significance of "Room for Error" in "The Psychology of Money"?

- Planning for uncertainty: Room for error involves planning for unexpected events and having a financial buffer to handle them.

- Margin of safety: It acts as a margin of safety, allowing individuals to endure financial setbacks without derailing long-term goals.

- Flexibility advantage: Having room for error provides flexibility and reduces the pressure to make perfect financial decisions.

- Long-term success: It is crucial for long-term financial success, as it helps individuals stay the course during volatile times.

About the Author

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.