Key Takeaways

Chase F-You Money, not retirement, so you can always say no

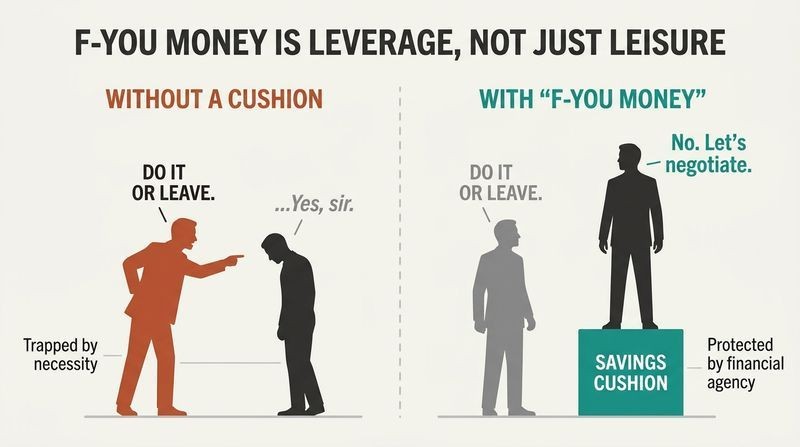

The real prize is freedom, not leisure. Collins never aimed to stop working. He aimed to accumulate enough savings that he could walk away from any boss, project, or situation that no longer served him. He calls this stash F-You Money, a phrase he lifted from a James Clavell novel. At age 25, after saving just $5,000 on a $10,000 salary, he asked for four months of unpaid leave, got refused, and resigned. His boss immediately reversed course and negotiated a six-week leave plus an extra month of annual vacation.

That modest cushion taught him working relationships are negotiable when you can afford to lose the job. Money's most valuable purchase is the ability to choose your work and refuse abuse.

What's striking is how Collins reframes money as leverage rather than accumulation for its own sake. This aligns with psychological research on autonomy: self-determination theory identifies control over one's actions as a core driver of wellbeing, often outranking income. The insight also echoes Nassim Taleb's observation that a person who cannot afford to be fired is not truly free. One caveat worth naming: the same cushion that empowers negotiation can breed complacency or premature exits. The power of F-You Money lies less in spending it than in never needing to, which requires the discipline to keep it intact.

Spend less than you earn, invest the surplus, avoid debt

The entire strategy fits on a napkin. Collins compresses financial independence into three moves that reinforce each other. A high savings rate does double duty: you learn to live on less while simultaneously building the pile that frees you. He suggests aiming for 50% of income, which he insists is doable without debt, and notes some enthusiasts push toward 70-80%.

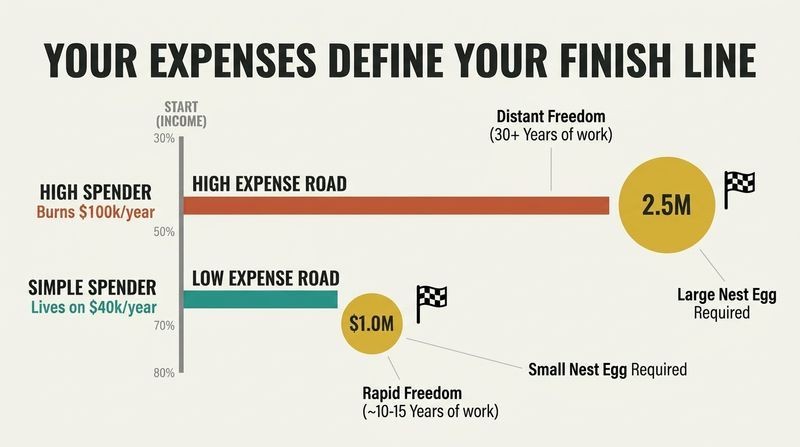

Independence is as much about wanting less as having more. He contrasts a friend burning through $175,000 every three months (miserable on an $800,000 bonus) with the author of Early Retirement Extreme, who lives contentedly on $7,000 a year and needs only $175,000 invested to be free. Someone earning $25,000 who lives on $12,500 can reach independence in roughly a decade. Money is relative; your needs set the finish line.

The math here is genuinely subversive. Personal finance culture obsesses over investment returns, but Collins shows the savings rate is the dominant lever. Blogger Mr. Money Mustache demonstrated the same point quantitatively: at a 50% savings rate, you reach independence in about 17 years regardless of income, because saving more shrinks both the numerator (time) and the denominator (required nest egg). One limitation: the framing assumes discretionary income exists to compress. For those near subsistence, the advice reads as tone-deaf, though Collins would argue the principle still directs whatever surplus is available.

Treat debt like leeches to scrape off, not normal life

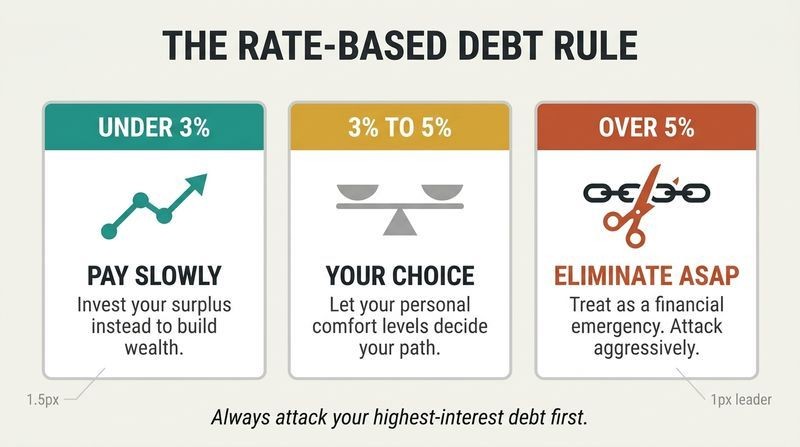

Debt is the single biggest obstacle to wealth. Collins rejects the cultural framing of debt as the ticket to the good life. He argues easy financing is precisely why cars average $32,000 and degrees exceed $100,000; the loans inflate the prices. He offers a rate-based rule for existing debt:

1. Under 3%: pay slowly, invest instead.

2. Between 3-5%: your comfort decides.

3. Over 5%: eliminate ASAP.

Attack highest-interest debt first. He rejects the popular smallest-balance-first method as a psychological crutch, preferring you adapt yourself to the numbers. He is especially scathing about student loans, which survive bankruptcy and can garnish wages and even Social Security. A state school education jumped 33-fold from 1970 to 2014 while general prices rose only six-fold, creating what he calls a generation of indentured servants.

Collins's rate-based framework is financially rational but psychologically contested. Behavioral economist studies on the debt snowball method (smallest balance first) suggest early wins boost persistence, which is why Dave Ramsey champions it. Collins knowingly rejects this, betting readers can rewire their psychology rather than accommodate it. His critique of student debt anticipates the broader reckoning over higher education financing: when a third party guarantees payment, sellers face little price discipline, a dynamic economists call moral hazard. The leech metaphor is deliberately visceral, designed to strip away the respectability debt has acquired in modern consumer culture.

Toughen up: the market always climbs, but the ride terrifies

Crashes are the price of admission, not a malfunction. Over 1975 to 2015, the market averaged 11.9% annually with dividends reinvested, despite the 1987 crash, the dot-com bust, 9/11, and 2008. Collins guarantees your wealth will be cut in half more than once across a long investing life, and that 2008-scale meltdowns arrive roughly every 25 years. The market always recovers, and if it ever truly doesn't, no investment will be safe anyway.

Your psychology, not the market, is the real risk. In 1987, Collins himself panicked and sold near the bottom, locking in losses and paying a premium to buy back in a year later. That expensive lesson taught him to stay the course. Most investors underperform the very funds they own because they buy high and sell low.

This is the emotional core of the book, and it is well supported. Dalbar's annual studies consistently show the average investor earns several percentage points less than the funds they hold, purely from mistimed buying and selling. Collins's insistence on internalizing crashes emotionally, not just intellectually, matches research on affective forecasting: people systematically underestimate how they will feel during losses. Kahneman and Tversky's loss aversion explains why a 50% drop feels catastrophic even when history guarantees recovery. The honest confession of his own 1987 panic makes the lesson credible. The one unexamined assumption is American exceptionalism, addressed elsewhere as the survivorship question.

Own the whole market with one index fund and forget it

Buy everything instead of guessing winners. Collins's core recommendation is VTSAX, Vanguard's Total Stock Market Index Fund, which holds roughly 3,700 US companies. Because failing companies drop out and new winners rise, the index is self-cleansing: a bad stock can only fall 100%, but a winner can rise 1,000% or more, creating a permanent upward bias. Jack Bogle, who launched the first index fund in 1975, said in 61 years he never met anyone who could reliably beat the market.

Fees are the silent wealth-killer. VTSAX charges 0.05% versus the industry average of about 1.25%. Over 20 years, giving up 2% annually to an advisor can cost nearly $287,000 on a $100,000 investment. A Vanguard study found 82% of actively managed funds failed to beat the index over 15 years, yet all charged high fees to try.

The evidence for indexing is overwhelming and has only strengthened since publication. The SPIVA scorecards from S&P confirm that over 15-year windows, roughly 90% of active US equity funds underperform their benchmarks. Warren Buffett famously won a decade-long bet that an S&P 500 index fund would beat a basket of hedge funds. Collins's beer-and-foam metaphor (the businesses are the beer, the daily price swings are the foam) is a memorable way to separate signal from noise. The subtle critique worth raising: as passive investing grows, some economists question whether price discovery suffers, though active managers still dominate enough trading volume to keep markets efficient.

Skip international funds; VTSAX already owns global giants

You are more globally diversified than you think. Collins breaks from nearly every other advisor by refusing to recommend a separate international allocation. His reasoning is threefold: added currency risk, added expense (international funds cost at least twice VTSAX's 0.05%), and redundancy. The 500 largest US companies make up about 80% of VTSAX, and giants like Apple, Coca-Cola, and Caterpillar earn half or more of their sales overseas.

Correlation erodes the diversification benefit. The classic argument for holding foreign stocks is that they move independently of US markets, smoothing returns. But as economies knit together, world markets increasingly move in lockstep, shrinking that benefit. For readers who still want more exposure, he points to Vanguard's ex-US funds or a total world fund, while cautioning to always include the US market, which is too large to skip.

This is Collins's most contrarian position and the one most likely to age unevenly. Vanguard itself, along with most portfolio theorists, recommends 20-40% international allocation, arguing that home-country bias is a documented behavioral error. The counterargument: US equities have crushed international for over a decade, seemingly vindicating Collins, but valuations and the dollar mean-revert, and past US dominance does not guarantee future returns. His point about multinationals providing indirect exposure is real but incomplete, since revenue exposure differs from currency and governance diversification. Reasonable investors split here; Collins simply prioritizes simplicity and low cost over theoretical optimization.

You will be conned; certainty you can't be is the trap

Everyone is a mark, especially the confident. Collins tells of nearly making an enemy of a friend's widow by warning her about financial predators. Her fatal reply: I can't be conned. That statement, he says, violates the first rule of avoiding cons. The smartest people are often the easiest targets because they let their guard down in areas they think they understand. Many of Bernie Madoff's victims were financial professionals.

How the classic con works. He describes a scam where an advisor mails stock predictions that keep coming true. The trick is an inverted pyramid: send 1,000 letters, half predicting a rise and half a fall. The 500 who got the right call get a second letter, split again, and so on. By the sixth letter, a handful of people have seen six perfect predictions and are begging to invest. Ninety-nine percent of a con is true; the lie hides in the fine print.

Collins's rules distill decades of fraud psychology. Research on affinity fraud confirms that con artists exploit trust within groups and expertise blind spots, which is why doctors get scammed on medical investments and financiers on financial ones. The inverted-pyramid stock scam is a real historical technique sometimes called the sports-betting tout scheme. His deeper point connects to metacognition: the Dunning-Kruger effect works in reverse here, as competence in one domain breeds overconfidence in adjacent ones. The practical safeguard he implies is structural humility: assume vulnerability, verify independently, and treat any too-good-to-be-true return as a red flag by definition.

When 25x your annual spending is invested, you are free

The 4% rule defines the finish line. Financial independence arrives when you can live on 4% of your portfolio each year, meaning your invested assets equal 25 times your annual expenses. Live on $20,000 and you need $500,000; live on $40,000 and you need $1 million. This comes from the Trinity Study, where three professors tested withdrawal rates across 30-year periods. A portfolio taking 4% annually with inflation adjustments survived 96% of the time, failing only if you started in 1965 or 1966.

Flexibility matters more than the exact number. Withdrawing 3% or less is nearly bulletproof; straying past 7% risks dog food in old age. Crucially, the study assumes low-cost index funds; add 2% in fees and the success rate collapses from 96% to 65%. Collins himself withdraws over 5% but stays flexible, ready to cut spending if markets crash.

The 4% rule is the most cited and most debated heuristic in retirement planning. Critics like Wade Pfau (whom Collins quotes) note it was derived from US historical data during an exceptional era, and sequence-of-returns risk means the first few years matter disproportionately. A crash early in retirement is far more dangerous than one late. Collins's emphasis on flexibility is the crucial nuance often lost in popular retellings: the rule was never meant as a set-and-forget autopilot. Recent work on dynamic withdrawal strategies (spending more in good years, less in bad) confirms his instinct that a living, adjusting approach beats rigid mechanical rules.

Match your fund to your life stage, not your age

Two stages, two simple portfolios. Collins divides investing life into the Wealth Accumulation Stage (while you earn and add money) and the Wealth Preservation Stage (once you live off your investments). For accumulation, he recommends 100% stocks via VTSAX: aggressive, volatile, and highest-returning. For his own semi-retired preservation stage, he holds roughly 75% VTSAX, 20% VBTLX (Vanguard's Total Bond Fund, a deflation hedge and ride-smoother), and 5% cash.

Stages shift with life, not birthdays. He rejects the conventional rule of putting your age in bonds. People retire early, take sabbaticals, or return to work, so stages can flip multiple times. For those who want zero maintenance, Target Retirement Funds automatically rebalance and grow more conservative over time for a slightly higher fee. He rebalances once a year, on his wife's birthday, and notes Bogle found rebalancing benefits are so slight they may be statistical noise.

Framing allocation by life stage rather than age is a meaningful update to conventional glide-path thinking, and it reflects the reality of nonlinear modern careers. The bonds-as-deflation-hedge framing is elegant: stocks hedge inflation (companies raise prices), bonds hedge deflation (fixed payments gain purchasing power). One tension: 100% stocks during accumulation maximizes expected return but assumes iron discipline during crashes, which most people lack. This is why Target Retirement Funds, which Collins endorses as second-best, may actually produce better real-world outcomes for the average person, precisely because automation removes the temptation to panic-sell that undoes even the best-designed portfolio.

Stop thinking what money buys; think what money earns

Every dollar spent has an invisible second cost. Collins urges shifting from consumption thinking to compounding thinking. A $20,000 car costs far more than $20,000 because of opportunity cost, the earnings you forfeit by spending rather than investing. At 8%, that $20,000 could earn $1,600 a year, so over ten years of ownership the true cost climbs past $36,000, and that ignores the compounding those lost earnings would have generated.

Buffett owns businesses, not paper. Collins invokes Warren Buffett, who lost $25 billion on paper in 2008 but never panicked because he thinks of stocks as ownership stakes in real companies, not fluctuating slips of paper. Mike Tyson earned about $300 million and went bankrupt because he understood money only as a tool for buying things. Financial independence means your portfolio's compounding growth outpaces the opportunity cost of what you spend.

Opportunity cost is economics 101, but Collins weaponizes it emotionally by calling it compounding's evil twin. The framing is powerful, though it can curdle into miserliness if taken to extremes, since a life of never spending defeats the purpose of freedom. Behavioral finance offers a useful counterbalance: research on the hedonic value of experiences shows that some spending genuinely increases lasting wellbeing, so the goal is intentional spending, not zero spending. The Tyson example illustrates a robust finding that sudden wealth without financial literacy rarely survives; studies of lottery winners show high bankruptcy rates driven by the same consumption-only mindset Collins diagnoses.

Analysis

The Simple Path to Wealth succeeds by weaponizing simplicity against an industry that profits from complexity. Collins, writing originally as letters to his daughter, makes a thesis-driven argument disguised as a memoir: financial independence requires only a high savings rate, low-cost index funds, and the emotional fortitude to ignore market noise. What distinguishes the book is not novel information (Bogle and the efficient-market crowd said much of this decades earlier) but its rhetorical clarity and emotional honesty. Collins confesses his own expensive mistakes, from the 1987 panic-sell to $50,000 lost on a gold penny stock, which lends credibility that data alone cannot.

The book's intellectual spine is sound and increasingly vindicated by SPIVA data and Buffett's famous hedge-fund bet. Its most defensible claims (fees compound catastrophically, timing is futile, savings rate dominates) are empirically robust. Its most contestable positions are the 100% US-equity tilt and the dismissal of international diversification, which rest heavily on an era of American market dominance that theory suggests should mean-revert. Collins essentially bets on continued US exceptionalism while framing it as prudence, a subtle sleight worth flagging.

The deeper achievement is philosophical. By redefining wealth as freedom (F-You Money) rather than consumption, Collins reframes frugality as liberation rather than sacrifice, aligning with self-determination theory's emphasis on autonomy. His parable of the monk and the minister crystallizes this: the person who can live on rice and beans needs no king to cater to. The weakness is scope; the advice assumes discretionary surplus and thus speaks most directly to middle-class earners, less to those at subsistence. Yet within its audience, the book earns its evangelical following precisely because it does one thing exceptionally well: it removes the fear and paralysis that keep ordinary people out of markets, replacing them with a plan simple enough to actually follow for decades.

Review Summary

The Simple Path to Wealth receives high praise for its straightforward approach to financial independence. Readers appreciate Collins' clear advice on avoiding debt, saving aggressively, and investing in low-cost index funds. The book is lauded for its simplicity and effectiveness, particularly for those new to investing. Some criticisms include its US-centric focus and lack of guidance for older investors. Many consider it a must-read for anyone seeking financial literacy, though its applicability may vary for non-US readers.

People Also Read

FAQ

What's "The Simple Path to Wealth" about?

- Financial Independence Focus: "The Simple Path to Wealth" by J.L. Collins is a guide to achieving financial independence and living a rich, free life. It emphasizes the importance of mastering money to gain freedom.

- Investment Strategy: The book advocates for a simple investment strategy using low-cost index funds, particularly those offered by Vanguard, to build wealth over time.

- Personal Finance Advice: It provides practical advice on saving, investing, and avoiding debt, aiming to simplify the often complex world of personal finance.

- Life Philosophy: Beyond finances, the book encourages readers to live life on their own terms, using financial independence as a tool to explore personal passions and interests.

Why should I read "The Simple Path to Wealth"?

- Simplified Investing: The book demystifies investing, making it accessible to those who may find the topic intimidating or complex.

- Proven Strategies: J.L. Collins shares strategies that have worked for him, backed by historical data and personal experience, offering a reliable path to financial security.

- Empowerment: It empowers readers to take control of their financial future, emphasizing that anyone can achieve financial independence with the right approach.

- Life Lessons: The book is not just about money; it also offers insights into living a fulfilling life, free from financial stress.

What are the key takeaways of "The Simple Path to Wealth"?

- Index Funds: Investing in low-cost index funds, like Vanguard's Total Stock Market Index Fund (VTSAX), is a core strategy for building wealth.

- Avoid Debt: Debt is a major obstacle to financial independence; the book advises avoiding it whenever possible.

- F-You Money: Having enough savings to say "no" to undesirable situations is crucial for personal freedom and security.

- Simplicity and Patience: Keeping investments simple and being patient with market fluctuations are essential for long-term success.

How does J.L. Collins suggest handling market volatility?

- Expect Volatility: Collins emphasizes that market volatility is normal and should be expected as part of the investment journey.

- Stay the Course: He advises against trying to time the market, suggesting that investors should remain invested and not panic during downturns.

- Long-Term Perspective: The book encourages a long-term view, highlighting that the market has historically always gone up over extended periods.

- Buying Opportunities: Market drops are seen as opportunities to buy more shares at lower prices, ultimately benefiting long-term investors.

What is the "4% Rule" mentioned in "The Simple Path to Wealth"?

- Withdrawal Rate: The 4% Rule is a guideline for how much you can withdraw from your retirement savings annually without running out of money.

- Trinity Study: Based on the Trinity Study, it suggests that a 4% withdrawal rate, adjusted for inflation, is sustainable for a 30-year retirement period.

- Flexibility Required: While generally reliable, the rule requires flexibility; in years of poor market performance, spending may need to be adjusted.

- Portfolio Composition: The rule assumes a balanced portfolio, typically 50% stocks and 50% bonds, to manage risk and growth.

What are the best quotes from "The Simple Path to Wealth" and what do they mean?

- "Spend less than you earn—invest the surplus—avoid debt." This quote encapsulates the core financial philosophy of the book, emphasizing the importance of saving and investing wisely.

- "The market always goes up." Collins reassures readers that despite short-term volatility, the stock market has historically increased in value over the long term.

- "F-You Money is critical." This highlights the importance of having enough savings to maintain independence and make choices aligned with personal values.

- "Simplicity is the keynote of all true elegance." Reflecting the book's approach, this quote underscores the value of keeping financial strategies straightforward and effective.

How does J.L. Collins recommend structuring a portfolio?

- Core Holdings: Collins recommends a simple portfolio primarily composed of Vanguard's Total Stock Market Index Fund (VTSAX) for stocks and Total Bond Market Index Fund (VBTLX) for bonds.

- Asset Allocation: The allocation between stocks and bonds should reflect the investor's stage in life, risk tolerance, and financial goals.

- Tax Efficiency: He suggests holding tax-efficient investments in taxable accounts and tax-inefficient ones, like bonds, in tax-advantaged accounts.

- Rebalancing: Periodically rebalancing the portfolio to maintain the desired asset allocation is advised, though not overly frequently.

What is "F-You Money" and why is it important according to "The Simple Path to Wealth"?

- Definition: "F-You Money" is a term used to describe having enough savings to walk away from undesirable situations without financial worry.

- Freedom and Security: It provides the freedom to make life choices based on personal values rather than financial necessity.

- Negotiation Power: Having F-You Money gives individuals leverage in negotiations, whether in personal or professional contexts.

- Peace of Mind: It offers peace of mind, knowing that financial stability is not dependent on any single job or income source.

How does "The Simple Path to Wealth" address debt management?

- Avoidance: The book strongly advises avoiding debt whenever possible, as it is a significant barrier to financial independence.

- Debt Elimination: For those already in debt, Collins suggests prioritizing its elimination, especially high-interest debt, to free up resources for investing.

- Psychological Impact: Debt is likened to being covered in leeches, emphasizing its draining effect on financial and emotional well-being.

- Financial Freedom: Eliminating debt is a crucial step toward achieving financial freedom and the ability to invest more aggressively.

What is J.L. Collins' view on investment advisors in "The Simple Path to Wealth"?

- Skepticism: Collins is skeptical of investment advisors, citing conflicts of interest and high fees that can erode investment returns.

- Self-Management: He advocates for self-management of investments, emphasizing that individuals can achieve better results with simple strategies.

- Cost Concerns: The book highlights the significant cost of advisor fees over time, which can substantially reduce the growth of a portfolio.

- Education and Empowerment: By educating themselves, investors can make informed decisions and avoid the pitfalls of relying on potentially biased advisors.

How does "The Simple Path to Wealth" suggest handling retirement accounts like 401(k)s and IRAs?

- Maximize Contributions: Collins advises maximizing contributions to tax-advantaged accounts like 401(k)s and IRAs to benefit from tax deferral.

- Employer Match: Taking full advantage of any employer match in a 401(k) is recommended, as it is essentially free money.

- Roth vs. Traditional: The book discusses the benefits of both Roth and Traditional IRAs, suggesting Roth IRAs for those in lower tax brackets.

- Rollovers: When changing jobs, rolling over 401(k) funds into an IRA is suggested to maintain control and potentially reduce fees.

What is the role of bonds in the investment strategy outlined in "The Simple Path to Wealth"?

- Stability and Income: Bonds provide stability and income, helping to smooth out the volatility of stocks in a portfolio.

- Deflation Hedge: They serve as a hedge against deflation, offering a counterbalance to the inflation protection provided by stocks.

- Risk Management: As investors approach retirement, increasing bond allocation can reduce risk and preserve capital.

- VBTLX Recommendation: Collins recommends Vanguard's Total Bond Market Index Fund (VBTLX) for its broad diversification and low cost.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.