Key Takeaways

Being right only half the time can still make you a fortune

Minervini, an eighth-grade dropout who taught himself trading, won the 1997 U.S. Investing Championship with a 155 percent annual return and averaged 220 percent yearly from 1994 to 2000. His secret is counterintuitive: he is correct on only about 50 percent of his trades. What separates him from amateurs is not stock-picking accuracy but rigorous risk management. Because losses work against you geometrically (a 50 percent drop requires a 100 percent gain to recover), keeping each loss small while letting winners run tilts the math in your favor. Superperformance, his term for outsized returns that transform a small account into a fortune, comes from discipline, not clairvoyance or luck.

This reframes trading as a probabilistic game closer to poker or insurance underwriting than fortune-telling, a point Minervini makes explicitly. It echoes Nassim Taleb's distinction between frequency of being right and magnitude of payoff: you can be wrong most of the time and still win if your winners dwarf your losers. The claim is empirically defensible, though survivorship bias looms. Thousands attempt the same asymmetric-payoff strategy and blow up. What Minervini downplays is that the psychological discipline to cut losses consistently is rarer than the intellectual understanding of why you should.

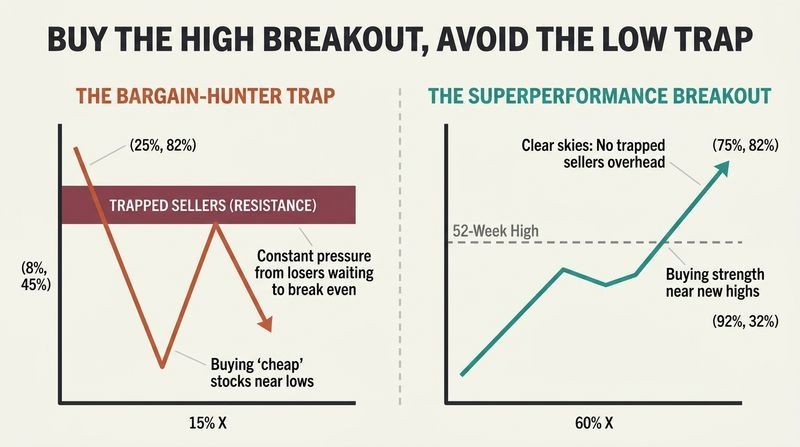

Buy stocks near new highs, never bargain-hunt at the lows

Minervini's early strategy of buying beaten-down, cheap stocks produced dreadful results, because many low-priced stocks are cheap for good reason and headed lower. He discovered that the biggest winners hit the 52-week-high list and then climb higher still. His Trend Template demands a stock trade above its rising 150-day and 200-day moving averages, sit at least 30 percent above its 52-week low, and rank in the top relative-strength tier before he considers buying. A stock at a new high has no trapped sellers waiting overhead to dump shares; a stock near its low is buried under people desperate to break even.

This directly contradicts the folk wisdom of buy low, sell high, and aligns with academic momentum research (Jegadeesh and Titman documented that past winners keep winning over 3-to-12-month horizons). The overhead-supply concept is behavioral economics in action: the disposition effect means losers hold until breakeven, creating selling pressure at prior highs. Minervini's insight is that a fresh all-time high clears that resistance entirely. The caveat: momentum strategies suffer brutal crashes during regime shifts, which is precisely why his stop-loss discipline is inseparable from the entry philosophy.

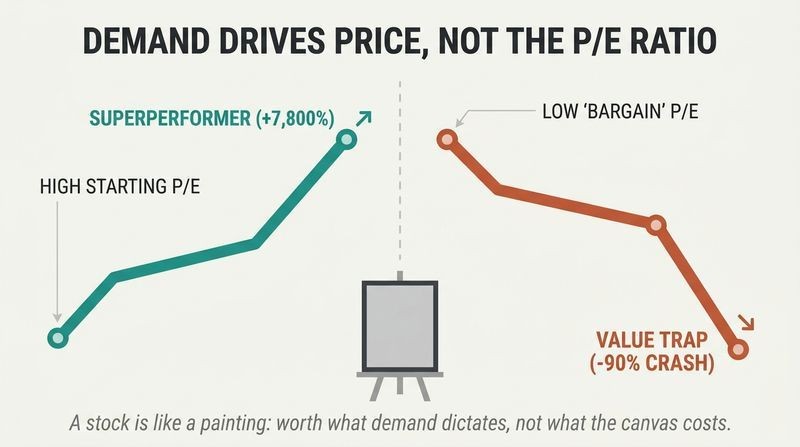

A high P/E is often the cheapest thing about a great stock

Minervini calls the price/earnings ratio one of the most useless statistics on Wall Street for finding big winners. He bought Yahoo at 938 times earnings; it rose 7,800 percent in 29 months. The top 100 small- and mid-cap performers of 1996 to 1997 averaged a P/E of 40 at the start and 87 later, gaining 421 percent. Meanwhile AIG, Citigroup, and others hit 10-year-low P/Es in 2008 and then fell over 90 percent. The reason: value does not move prices, people do, through buy orders. A stock is like a van Gogh painting, worth what demand dictates, not what the canvas costs.

Minervini weaponizes a truth value investors resist: growth companies grow so fast that Wall Street cannot price them efficiently, leaving them systematically undervalued relative to future earnings. His superlow-P/E warning is the sharper insight, a P/E of two or three near a 52-week low often signals impending bankruptcy, not a bargain. This is a useful corrective to naive Graham-and-Dodd screening. However, the framing risks confirmation bias: for every Yahoo at 938x that soared, countless high-multiple stocks imploded. The discipline that redeems it is his willingness to sell fast when the trend breaks.

Every big winner climbs through four predictable life-cycle stages

Adapted from Stan Weinstein's work, Minervini maps every stock through four stages: Stage 1 (neglect, drifting sideways with no trend), Stage 2 (advancing, driven by accumulation and rising earnings), Stage 3 (topping, volatile distribution as smart money sells to latecomers), and Stage 4 (decline, capitulation). Roughly 99 percent of superperformers trade above their 200-day moving average during their big move, and over 90 percent launch as the broad market exits a correction or bear market. The entire lesson is simple: buy only in Stage 2, never fish for bottoms in Stage 1, and never hold through Stage 3 into Stage 4.

Stage analysis is essentially a visual heuristic for trend persistence, and its power lies in forcing patience. The framework prevents two classic errors: premature bottom-fishing and holding losers into oblivion. What's notable is Minervini's fusion of technical stages with fundamental cause. He overlaid earnings data on price stages and found accumulation coincides with earnings surprises. Critics of technical analysis argue such patterns are apophenia, seeing shapes in noise. The rejoinder is that Minervini uses stages as a filter, not a crystal ball, refusing any stock in a downtrend regardless of story quality, which is risk control masquerading as pattern recognition.

Watch for volatility to shrink from left to right before buying

Minervini's signature setup is the Volatility Contraction Pattern (VCP). As a stock consolidates, it undergoes a series of two to six progressively smaller pullbacks, each roughly half the depth of the prior one, accompanied by shrinking trading volume. A stock might correct 25 percent, then 15 percent, then 8 percent, then 3 percent. This tightening signals that weak, nervous holders have been shaken out and supply has dried up, establishing what Jesse Livermore called the line of least resistance. He records each stock's technical footprint in shorthand (weeks, largest correction over smallest, number of contractions), then buys as price breaks above the pivot point on a volume surge.

VCP is a disciplined operationalization of supply-and-demand equilibrium. The genius is quantifying the qualitative: rather than eyeballing a base, Minervini demands measurable contraction in both price range and volume, which filters out failure-prone patterns. The concept resonates with the physics of coiled springs and with information theory, declining volatility reflects declining disagreement about price. The vulnerability is subjectivity in real time; contractions are cleaner in hindsight. Minervini's insistence on waiting for the actual breakout above the pivot, rather than anticipating it, is the crucial guardrail that converts a chart pattern into a risk-defined trade.

Your loss limit should be half your average winning gain

Minervini treats loss-cutting like an insurance actuary treats mortality tables: your maximum acceptable loss is a mathematical function of your expected gain, not an arbitrary feeling. If your winners average 15 percent, cut losers at no more than 7.5 percent. He caps every loss at an absolute 10 percent regardless. His Loss Adjustment Exercise proved this: retroactively capping his past losses at 10 percent flipped a losing portfolio into a 70-plus percent gain. He aims for a 2:1 or 3:1 reward-to-risk ratio, which he calls building in failure, meaning he can be right just 40 to 50 percent of the time and still prosper.

This is the book's mathematical backbone, and it is rigorous. Minervini's warning against widening stops for volatile stocks contradicts common advice but is provably correct: as your batting average falls in tough markets, larger losses drive you toward negative expectancy faster than higher gains save you. The actuarial framing is elegant and underused among retail traders. The behavioral obstacle he names honestly, cutting a loss means admitting error, and ego resists. Kahneman and Tversky's prospect theory explains exactly why: losses loom larger than gains, so humans hold losers hoping to avoid the pain of realizing a mistake.

Superperformers are young companies with an identifiable catalyst driving them

Most superperformance stocks go public within 8 to 10 years of their biggest move, when they are small, nimble, and expanding into untapped markets with entrepreneurial management at its best. Eighty percent of the 1990s tech winners were IPOs within the prior eight years. Behind every huge advance sits a catalyst: a hot new product (Apple's iPod, Crocs' clogs), FDA approval, a new CEO, or an industry shift. Small share floats matter, less demand is needed to move the price. Minervini looks for the primary base, the first sound consolidation after a company goes public, as the safest entry into a young leader.

The youth-and-catalyst thesis aligns with innovation-diffusion theory: growth is fastest during early market penetration, before saturation compresses margins and multiplies competitors, as Minervini illustrates with the auto and TV industries collapsing from dozens of firms to a handful. The emphasis on small float is sound market microstructure, thin supply amplifies price moves in both directions. One tension: buying recent IPOs is notoriously risky (Facebook's 2012 debut is his own cautionary tale), so his insistence on a multi-week primary base before entry is what separates disciplined participation from lottery-ticket speculation on unproven newcomers.

Demand accelerating earnings, sales, and margins all firing at once

Minervini wants a Code 33: three consecutive quarters of accelerating earnings, sales, and profit margins simultaneously. Over 90 percent of the biggest winners showed earnings acceleration before or during their moves. He insists on 20 to 25 percent minimum quarterly earnings growth (often 30 to 100 percent), backed by real revenue growth, not accounting tricks. He scrutinizes earnings quality: he strips out one-time gains, distrusts profits built only on cost-cutting (which walks on short legs), and treats rising inventories or receivables growing faster than sales as red flags. Cisco posted 15 of 17 quarters above 100 percent earnings growth while its stock rose 13-fold.

This is fundamental analysis in service of a technical strategy, a hybrid Minervini calls techno-fundamentalism. The Code 33 concept captures operating leverage: when revenue accelerates while margins expand, earnings explode nonlinearly, and markets reward that convexity with multiple expansion. His forensic skepticism about earnings quality anticipates concerns later formalized in accounting research on earnings management and the accruals anomaly (Sloan's work showed cash-based earnings predict returns better than accrual-heavy ones). The practical wisdom in comparing finished-goods inventory to sales is genuine operational insight most chart-focused traders ignore entirely, giving his approach unusual depth.

The market's true leaders bottom first and warn you first

Leading stocks turn up days, weeks, or months before the Dow, S&P, and Nasdaq bottom, and they buckle first at tops. Amgen and American Power Conversion emerged into new highs on the exact same day, 22 days into the 1990 rally, while the indexes languished 25 percent below their peaks; APCC then rose 4,100 percent. Panera Bread rose 1,100 percent while the Nasdaq fell 80 percent during 2000 to 2002. Minervini takes a bottom-up approach: individual leaders point him to hot sectors, not the reverse. Fewer than 25 percent of one cycle's leaders lead the next, so expect unfamiliar names each time.

This inverts the standard top-down macro approach and has real merit, leadership rotation is a documented feature of market cycles, and the observation that yesterday's leaders rarely lead again aligns with the creative-destruction dynamics of capitalism. The practical payoff is using your own watchlist and portfolio as an early-warning system for the broad market. The risk is that a handful of vivid examples (Panera surging during a crash) can seduce readers into fighting the tape. Minervini guards against this by insisting most superperformers still launch coming out of corrections, so the leader-spotting is about preparation during declines, not heroism against them.

Concentrate in four to six stocks; diversification guarantees average results

Minervini rejects broad diversification as a protection myth, in a bear market almost everything falls together, so spreading across dozens of names just smooths you toward mediocrity while making it impossible to know each holding intimately or exit quickly. He typically holds 4 to 6 stocks (up to 10 or 12 for large portfolios), and has put his entire account in just four names during his most profitable periods. He scales into positions incrementally with pilot buys, adding only after a trade shows a profit, the opposite of amateurs who average down into losers. He quotes Buffett: risk comes from not knowing what you're doing.

Concentration versus diversification is one of investing's genuine fault lines. Minervini sides with Buffett, Munger, and Kelly-criterion logic: if you have a real edge, over-diversifying dilutes it. The math is sound only if the edge is real and losses are truly capped, which is why this takeaway is inseparable from his stop-loss discipline. For most retail investors lacking his monitoring intensity, concentration is dangerous advice, and he would agree, since it presupposes the skill to select and the discipline to exit. His scaling-in method (pyramiding winners, never averaging down) is a practical safeguard borrowed straight from Livermore and Sperandeo.

Wait like a cheetah; you get to see the market's cards for free

Minervini invokes trader Mark Weinstein's cheetah, which stalks patiently and strikes only when success is nearly certain. Unlike poker, where an ante costs money to see cards, the stock market lets you sit on the sidelines watching for free until probabilities stack in your favor. He advises pacing yourself like a 12-inning game: after coming out of cash, start slow with small pilot buys, find the market's theme, establish rhythm, then step up exposure only once trades confirm. If you keep getting stopped out, either your selection criteria are flawed or the market is hostile, so shrink position size until conditions improve.

The patience-as-edge argument is the emotional core of disciplined trading and the hardest to practice. Behavioral finance confirms that overtrading destroys returns (Barber and Odean found the most active retail traders underperform most). Minervini's insight that inactivity is a competitive advantage inverts the action-bias that markets exploit. The cheetah metaphor is memorable precisely because it dramatizes restraint as predatory strength rather than passivity. His adaptive position-sizing, scaling down during losing streaks rather than doubling up to recoup, is the antidote to the revenge-trading spiral that ruins accounts, and it reflects a mature understanding that markets, not willpower, dictate when opportunity exists.

Commitment, not talent or capital, is what separates winners from dreamers

Minervini dropped out of school at 15, started with a few thousand dollars, and endured six straight years without making a penny before breaking through. He distinguishes interest from commitment: interest gets you started, but commitment (the will to not give up) gets you to the finish. He read over 1,000 investing books, photocopying entire volumes he couldn't afford. He warns against paper trading because it lacks the emotional sting of real money, citing a memory study where students tested three times outperformed those who studied four times by 50 percent. Trade small but real amounts, own your failures, and treat trading like a business, not a hobby.

This is the motivational scaffolding around the technical method, and while such framing risks generic self-help territory, Minervini grounds it in specifics: the six barren years, the photocopied books, the discount-brokerage lobby where he checked quotes every ten minutes. His skepticism of paper trading is genuinely insightful and supported by the testing-effect research he cites, retrieval under real stakes builds durable skill in ways simulation cannot. The claim that anyone can achieve superperformance is inspiring but statistically dubious given survivorship bias. Still, his honest accounting of prolonged failure is a valuable counterweight to the overnight-success mythology that pervades trading culture.

Analysis

Trade Like a Stock Market Wizard is a framework-driven trading manual anchored by a rags-to-riches memoir, written for self-directed equity investors seeking outsized returns. Its central argument fuses two traditions usually held apart: growth-fundamental analysis and technical trend-following. Minervini brands this synthesis SEPA (Specific Entry Point Analysis), demanding that a stock satisfy trend, fundamentals, catalyst, entry, and exit criteria simultaneously, a convergence he compares to four cars arriving at an intersection at once.

The book's intellectual lineage is explicit and honest. Minervini credits Richard Love, Marc Reinganum, Stan Weinstein, Richard Donchian, William O'Neil, and Jesse Livermore, positioning himself as a synthesizer rather than an originator. This transparency is a strength; the ideas have been road-tested across market cycles back to the early 1900s. The core empirical claims (that superperformers trade above rising moving averages, launch from corrections, and are young companies with catalysts) are consistent with academic momentum literature, even if Minervini has no interest in academic validation and openly disdains the efficient-market hypothesis.

The deepest and most defensible material is on risk management, which occupies two full chapters and reflects genuine mathematical rigor. His actuarial framing of loss-cutting, his proof that widening stops in volatile markets courts negative expectancy, and his geometric-loss arithmetic elevate the book above typical chart-pattern manuals.

The principal weakness is survivorship bias, endemic to the genre. Minervini's own extraordinary record cannot establish that his method is replicable by readers, and the vivid winners (Yahoo, Amgen, Panera) are selected precisely because they worked. The strategy is also demanding: it requires daily monitoring, iron discipline, and emotional detachment few possess. Yet the book is unusually candid about this, insisting that the greatest challenge is not the market but the self. For disciplined, full-time-attentive traders, it offers a coherent, internally consistent, and risk-obsessed system. For passive investors, its concentration and momentum tenets are actively dangerous. Read as a probabilistic craft demanding relentless self-control, it is among the more rigorous popular trading texts.

Review Summary

Trade Like a Stock Market Wizard receives high praise for its comprehensive approach to growth stock investing. Readers appreciate Minervini's SEPA strategy, risk management advice, and insights on market psychology. Many find the book's technical analysis and chart examples valuable. Some note similarities to William O'Neil's methods but with unique perspectives. While a few critics find the content repetitive or challenging to apply, most reviewers consider it a must-read for both novice and experienced traders, citing improved trading performance after implementing Minervini's techniques.

People Also Read

FAQ

What's Trade Like a Stock Market Wizard about?

- Focus on Superperformance: The book by Mark Minervini emphasizes achieving exceptional returns in stock trading through a disciplined approach.

- SEPA Methodology: It introduces Specific Entry Point Analysis (SEPA), a method combining technical and fundamental analysis to identify high-potential stocks.

- Mindset and Discipline: Minervini highlights the importance of developing the right mindset and emotional discipline for success in the stock market.

Why should I read Trade Like a Stock Market Wizard?

- Comprehensive Guide: The book is a thorough resource on trading growth stocks, offering insights for both novice and experienced traders.

- Proven Strategies: Minervini shares tested strategies and personal experiences, helping readers learn from his successes and mistakes.

- Risk Management Focus: It emphasizes risk management as crucial for trading success, teaching how to protect capital while pursuing high returns.

What are the key takeaways of Trade Like a Stock Market Wizard?

- Superperformance Stocks: These are stocks with exceptional returns, often showing strong earnings growth and market leadership.

- Four Stages of Stocks: Understanding the stages—neglect, advancing, topping, and declining—helps in making informed buy and sell decisions.

- Trend Following: The principle "The trend is your friend" is emphasized, aligning strategies with market movements for better outcomes.

What is Specific Entry Point Analysis (SEPA) in Trade Like a Stock Market Wizard?

- Methodology Overview: SEPA is a systematic approach to identifying optimal entry points for stocks using both technical and fundamental analysis.

- Five Key Elements: It includes trend, fundamentals, catalyst, entry points, and exit points, each crucial for a stock's success.

- Risk vs. Reward: SEPA aims to pinpoint trades with the highest potential reward relative to risk, aiding informed investment decisions.

How does Mark Minervini define a market leader in Trade Like a Stock Market Wizard?

- Strong Relative Strength: Market leaders outperform the market, showing consistent price appreciation.

- Earnings Growth: They typically exhibit strong earnings growth, attracting institutional investors.

- Emerging from Bases: These stocks often emerge from well-formed bases, indicating a solid foundation for future price increases.

What are the four stages of a stock's life cycle according to Trade Like a Stock Market Wizard?

- Stage 1 - Neglect Phase: Stocks are overlooked with little price movement; investors should avoid buying.

- Stage 2 - Advancing Phase: Ideal for buying, characterized by strong price increases and institutional buying.

- Stage 3 - Topping Phase: Shows signs of weakness and increased volatility; investors should be cautious.

- Stage 4 - Declining Phase: Significant price drop due to deteriorating fundamentals; avoid buying.

How important is risk management in trading according to Trade Like a Stock Market Wizard?

- Critical Component: Effective risk management is essential for long-term success, focusing on potential losses over gains.

- Protecting Capital: The book teaches setting stop-loss orders and managing positions to minimize losses.

- Psychological Factors: Understanding and managing emotions is crucial for maintaining discipline and making rational decisions.

What is the importance of cutting losses in Trade Like a Stock Market Wizard?

- Preserving Capital: Cutting losses early helps protect trading capital for future opportunities.

- Avoiding Emotional Decisions: Emotional attachment to losing positions can lead to larger losses; sticking to stop-losses is essential.

- Statistical Advantage: Maintaining a favorable risk/reward ratio is crucial, and cutting losses helps achieve this.

How can I identify a stock's trend according to Trade Like a Stock Market Wizard?

- Moving Averages: Use tools like the 50-day and 200-day moving averages to identify trends.

- Price Action: Look for higher highs and higher lows to determine a bullish trend.

- Volume Analysis: Increasing volume during price advances suggests strong institutional interest.

What role do catalysts play in stock performance according to Trade Like a Stock Market Wizard?

- Driving Growth: Catalysts like new products or regulatory approvals can significantly impact performance.

- Identifying Opportunities: Recognizing catalysts helps identify stocks with superperformance potential early.

- Market Reactions: Catalysts often lead to rapid price movements; spotting them is crucial for successful trading.

How does Mark Minervini suggest handling a losing streak in Trade Like a Stock Market Wizard?

- Assess Your Strategy: Evaluate stock selection criteria and market conditions during a losing streak.

- Scale Down Exposure: Reduce position sizes to mitigate losses and preserve capital.

- Stay Disciplined: Maintain discipline and stick to your trading plan despite challenges.

What are the best quotes from Trade Like a Stock Market Wizard and what do they mean?

- "The trend is your friend.": Emphasizes trading in the direction of the market trend to increase success likelihood.

- "Your first loss is your best loss.": Highlights the importance of cutting losses early to protect capital.

- "Discipline is the bridge between goals and accomplishment.": Stresses the necessity of discipline in executing a trading plan for long-term success.

About the Author

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.