Key Takeaways

Master not losing money before you learn to make it

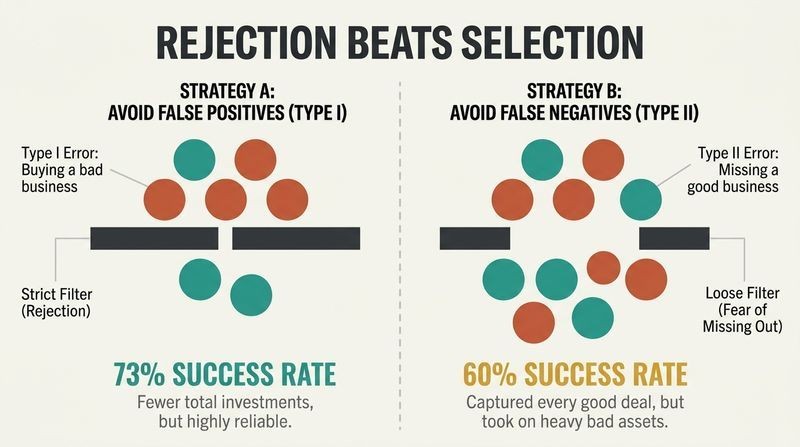

Rejection beats selection. Prasad opens by confessing his own $50 million wipeout at Warburg Pincus, then argues that the great investor is fundamentally a great rejector. He borrows statistics language: a Type I error (false positive) means buying a bad business you thought was good; a Type II error (false negative) means passing on a good business you thought was bad.

The math is brutal and counterintuitive. Even an investor right 80% of the time picks a good business only 57% of the time, because good businesses are rare. Cutting Type I errors from 20% to 10% lifts the success rate to 73%. Cutting Type II errors the same amount lifts it only to 60%. Nature agrees: deer, cheetahs, and plants all sacrifice opportunities to avoid the one fatal mistake.

The asymmetry Prasad surfaces echoes Nassim Taleb's survivorship logic and Charlie Munger's inversion principle: solve problems backward by avoiding stupidity rather than seeking brilliance. The statistical framing is genuinely useful because it quantifies why skepticism compounds. One nuance worth flagging: base rates matter enormously. His 57% figure assumes only 25% of businesses are good. In a richer opportunity set, minimizing Type II errors would matter more. Venture capital, which profits precisely by tolerating many false positives to catch one outlier, operates under the opposite regime. The lesson is not universal but strategy-dependent, which Prasad himself concedes when he notes he would have missed Amazon.

Define risk as odds of permanent loss, not price wobble

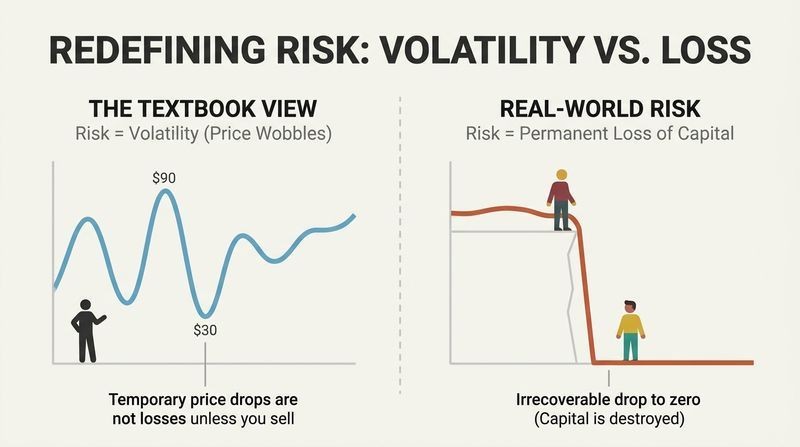

Reject the textbook definition. Finance theory equates risk with volatility, meaning a stock that swings wildly is deemed riskier. Prasad calls this nonsensical. If a quality grocery retailer trades at $90 before a crash and $30 after, academics label the $30 version riskier because volatility rose. Common sense says the opposite: your probability of capital loss is lower at $30.

Risk is the chance you never get your money back. Nalanda defines risk purely as the probability of permanent capital loss, ignoring past or future price swings entirely. This reframing drives everything: Buffett's famous rules about never losing money become, in Prasad's translation, a directive to avoid big risks and think about the downside before the upside. Betting your life, as prey animals effectively do at every watering hole, becomes a sound investing posture.

This distinction separates value investors from the modern portfolio theory establishment, and Prasad plants his flag firmly. The volatility-as-risk convention persists because it is mathematically tractable, not because it is wise. Beta and standard deviation are easy to compute; probability of permanent impairment requires judgment. There is a defensible counterargument, though: for investors who may be forced to sell (facing redemptions, margin calls, or liquidity needs), volatility becomes real risk because it determines the price at which they are compelled to transact. Prasad's definition works precisely because Nalanda has patient, committed capital that never forces a sale at the bottom.

Screen for one metric that drags many virtues behind it

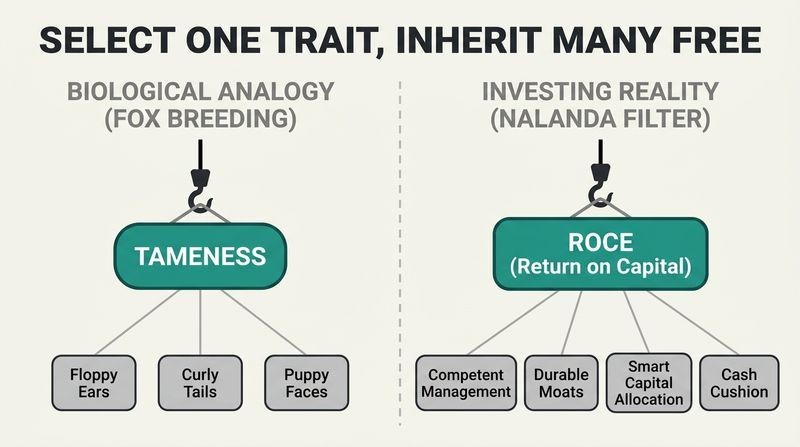

Select one trait, inherit many free. A 60-year Soviet experiment breeding silver foxes for tameness alone accidentally produced floppy ears, curly tails, piebald coats, and puppy-like faces, because selecting one behavioral trait shifted the hormones governing dozens of others. Prasad wanted an investing equivalent: a single measurable filter that quietly signals overall quality.

Return on capital employed is that filter. ROCE is operating profit divided by capital employed (working capital plus fixed assets). Nalanda rejects management quality (unmeasurable, as Enron's polished executives proved), revenue growth (WeWork grew eightfold while burning cash), and margins (Costco's 3% margin beats Tiffany's 19% because Costco turns inventory in 31 days versus 521). A consistently high ROCE tends to bring competent management, durable moats, smart capital allocation, and the cash cushion to take risks, all for the price of one screen.

The fox analogy is charming and scientifically real (the Belyaev experiment is a landmark in evolutionary biology), but the logic deserves scrutiny. ROCE is backward-looking, and Prasad admits monopolies, tariff protection, or plain luck can inflate it temporarily. The deeper insight is about correlated traits: in complex systems, a single well-chosen indicator often carries information about hidden variables. This is why credit scores, though crude, predict behavior across domains. The danger is Goodhart's Law: once a metric becomes a target, it gets gamed. Companies can juice ROCE by underinvesting or leveraging. Prasad guards against this by demanding a decade-plus track record rather than a single year.

Change without changing: buy businesses robust at many levels

Robustness is the hidden survival engine. Life persists through 3.5 billion years of assault because it is robust at multiple layers: a DNA mutation often codes the same amino acid, a changed amino acid often folds the same protein, altered proteins often preserve the body plan. Two sea urchin species look identical yet develop completely differently. McKinsey transformed its geography, services, and hiring over a century while staying culturally the same firm.

Robust businesses evolve while staying themselves. Nalanda seeks firms that are robust on many fronts simultaneously:

1. High, durable ROCE

2. Zero or minimal debt

3. Fragmented customer and supplier bases

4. Strong competitive barriers

5. Stable management in a slow-changing industry

Crucially, robustness enables evolvability. Paints maker Havells survived a botched acquisition because its 52% ROCE gave it cash to fix mistakes. Robustness comes free with quality, just as evolvability comes free with biological resilience.

Prasad's borrowing of robustness-enables-evolvability from Andreas Wagner's work is intellectually rich and underappreciated in investing circles. The idea that stability is a precondition for adaptation, not its opposite, inverts the Silicon Valley cult of disruption. It resonates with Nassim Taleb's antifragility, though Prasad stops short: he wants businesses that survive shocks, not ones that gain from them. The framework's weakness is subjectivity. Unlike ROCE, robustness is a qualitative judgment call across seven or more dimensions, and Prasad admits most businesses live in a gray zone. His honest counterexample, Gap, stayed robust yet stagnant for fifteen years, showing robustness guarantees survival but not growth.

Ignore what moves prices; obsess over what moves businesses

Separate proximate from ultimate causes. Biologists explain a bird's migration two ways: the proximate trigger (a cold snap on August 25) and the ultimate cause (millions of years of selection favoring migrants). Dung beetle horns can be explained by the hormones that grow them or the mating advantage that selected them. Both questions are valid but different.

Markets confuse the two constantly. A Fed rate hint, an OPEC breakdown, or a Greek default sends stocks tumbling worldwide, yet these are proximate noise divorced from long-term business success. When the Asian crisis hit in October 1997, Walmart and Boeing dropped, then rose 57% and 16% within six months. Three Indian banks under identical interest-rate regimes multiplied 16x, 33x, and 81x over two decades. The difference was management, not macro. Nalanda assigns exactly zero weight to macroeconomic forecasting.

The proximate-ultimate distinction, drawn from Ernst Mayr's foundational 1961 paper, is one of the book's most transferable mental models. It maps neatly onto Kahneman's signal-versus-noise problem and onto the trader-versus-owner divide. The evidence that economists failed to predict 148 of 150 recessions is damning and consistent with Philip Tetlock's research showing expert political and economic forecasters barely beat chance. Where Prasad slightly overreaches: for some businesses, macro genuinely is ultimate. Banks live and die by interest rate cycles and credit conditions; commodity producers by global prices. His own examples of high-quality banks succeeding across rate regimes actually prove that quality moderates macro sensitivity rather than eliminating its relevance entirely.

Interpret the past like Darwin; never forecast the future

Investing is a historical science, not a predictive one. Physics predicts; evolutionary biology explains what already happened. Darwin cracked natural selection, sexual selection, and common descent not with new data but by reinterpreting facts everyone could see: pigeon breeding, peacock tails, embryo similarities. Nalanda mimics this, analyzing only delivered historical financials over a decade or more, building zero projections.

Discounted cash flow is elaborate self-deception. DCF values a business as the sum of future cash flows discounted to today. But it requires forecasting a discount rate (built on the dubious volatility-equals-risk beta) and cash flows years out. A single percentage point change in discount rate swings present value 11-13%. Analysts could not predict Snapchat's numbers days ahead, yet DCF demands decade-long guesses. Nalanda values businesses on trailing earnings, buying at a median 14.9 PE versus the market's 19.7.

Prasad's assault on DCF is bracing but somewhat rhetorical. DCF is not wrong in theory; it is the mathematically correct definition of intrinsic value. His real objection is epistemic: the inputs are unknowable, so precision becomes false confidence. This echoes Keynes on spurious mathematical exactitude and Buffett's quip that he would rather be approximately right than precisely wrong. The historical-science framing is elegant and true to Stephen Jay Gould's philosophy of contingent explanation. The scope limit Prasad honestly flags: history fails for fast-changing industries (Nokia looked invincible on every historical metric) and for turnarounds (Starbucks post-2008), where the past actively misleads.

Invest in proven templates, not individual businesses

Convergence means success has a limited menu of forms. Unrelated species facing the same problem evolve the same solution independently. Caribbean lizards on four islands developed identical body types. Australian marsupials mirror placental wolves, mice, and anteaters. Sharks and dolphins share the same shape. There are only so many ways to swim fast or eat termites.

Business success converges too, so ask: where else has this worked? Nalanda invested in Naukri, India's leading job site, not because founders impressed them but because the model converged with two proven templates: old Yellow Pages directories (network-effect monopolies earning 40%+ margins) and seven global job boards from Australia to Japan showing identical economics. This mirrors Kahneman's outside view: before trusting your inside story, check base rates. The disciplined outside view on airlines (a cumulative $44 billion loss across US carriers from 2000 to 2013) says simply walk away.

The convergence-outside view pairing is the book's most practically powerful idea, uniting evolutionary biology with behavioral economics. Kahneman's finding that people ignore pallid statistical base rates in favor of vivid inside narratives explains most investing disasters and most failed business plans. Prasad's airline analysis is a masterclass in reference-class forecasting. The honest tension he raises through Lenski's E. coli experiment, where after 33,000 generations one population suddenly evolved to digest citrate, is that convergence is dominant but not absolute. Amazon is the citrate mutant of business, breaking the focus-wins pattern. Pattern-matching protects against hundreds of losers at the cost of missing the rare true anomaly.

Trust only signals that are expensive for a company to fake

Zahavi's handicap principle decodes corporate communication. In nature, a signal is honest only when it is costly to produce. A peacock's extravagant tail and a guppy's bright red coloration are reliable because they are dangerous handicaps only healthy animals can afford. Cheap signals get faked: small frogs lower their croak to fake size, milk snakes mimic venomous coral snakes.

Most corporate signals are cheap, therefore worthless. Press releases, glossy investor conferences, earnings guidance, and management interviews cost nothing to spin optimistically. Wirecard's CEO gave a flawless interview a year before his fraud arrest. Nalanda ignores all of these. It trusts only costly signals:

1. Decades of delivered operating and financial performance

2. Scuttlebutt from competitors, ex-employees, suppliers, and customers

A reputation built over decades cannot be faked cheaply. Scuttlebutt once revealed a company inflating sales through a subsidiary; its value later fell 98%.

Applying Zahavi's costly-signaling theory (a cornerstone of evolutionary biology and signaling economics, for which Michael Spence won a Nobel with his job-market model) to equity analysis is genuinely original. The insight cuts against the industry ritual of management meetings, which Prasad dismisses as theater. This aligns with research showing CEO charisma correlates poorly with firm performance and can even predict overconfident value destruction. One caveat: scuttlebutt has its own biases. Competitors may disparage, disgruntled ex-employees may distort, and confirmation bias can shape which sources an analyst weights. The costliness heuristic is powerful but not immune to the interpreter's own motivated reasoning. Verification across many independent sources, as Nalanda does, is the safeguard.

Great businesses drift daily but barely change over decades

Evolution runs fast short-term, slow long-term. Finnish scientist Bjorn Kurten found brown bear teeth changed at 13.8 units over 8,000 years but only 0.41 units over 400,000 years. The Grants watched Galapagos finch beaks swing dramatically year to year with droughts, yet stay range-bound across decades. Short-term fluctuation is not long-term direction.

Prasad calls this the Grant-Kurten Principle of Investing. For a high-quality business whose fundamental character stays stable, exploit the inevitable short-term price swings to buy, never to sell. L'Oreal endured lawsuits, recalls, price-fixing fines, and a 20% China sales drop between 2009 and 2020, yet remained the same global beauty compounder, its stock rising 450%. Nalanda invested $851 million (46% of fourteen years of deployment) during just 26 months of market panic, including $288 million in seventeen days of March 2020.

The fractal insight that volatility scales inversely with the observation window is empirically robust in both paleontology (Gingerich's work on evolutionary rates) and finance (the well-documented gap between daily price noise and long-run fundamental value). Prasad operationalizes it into a contrarian buying discipline that most investors preach but few practice, because loss aversion makes falling prices feel like danger rather than opportunity. The behavioral edge here is structural: patient committed capital lets Nalanda act when others are forced or frightened into selling. The scope limit Prasad honestly names is Kodak, where a genuine regime shift (digital photography) meant the short-term signal was actually a permanent punctuation, not noise.

Great firms stay great and bad ones stay bad for decades

Punctuated equilibrium describes business too. Gould and Eldredge argued species stay static for eons, then change abruptly, rather than evolving gradually. Stasis is the default in nature. Prasad finds the same in commerce: excellent businesses remain excellent, weak ones remain weak, far longer than intuition suggests. Of the 1955 Fortune 500, a plausible 40-45% were still thriving sixty years later. Meanwhile perhaps 97-99% of firms that could have joined the list never did.

This justifies extreme laziness in both buying and selling. Because great businesses are rare and durable, the default is not to buy. Because they stay great, once owned, the default is never to sell. Nalanda never confuses a rising stock price with genuine business improvement, which keeps it out of hyped sectors like Indian infrastructure, where Reliance Power fell 95% from its IPO peak.

Importing punctuated equilibrium into business strategy is provocative and mostly persuasive. The stasis observation aligns with research on persistent firm-level profitability differences (economists like Mueller documented that abnormal profits erode far more slowly than competitive theory predicts) and with the widening moat literature showing industry concentration rising since the 1990s. The counterweight is disruption theory: Christensen showed incumbents can be toppled by initially inferior entrants. Prasad's defense is that true disruption is rarer than pundits claim, and his Fortune 500 survival data supports him. The unresolved tension is identification. Knowing stasis is the default does not tell you whether a specific troubled firm is in temporary dip or permanent decline.

Let a handful of winners pay for all your mistakes

Compounding hides its power, then explodes. Twenty-four rabbits released in Australia in 1859 became ten billion by 1925, yet for decades almost nothing seemed to happen. Darwin grasped this: a 1% selective advantage spreads through a population in a few thousand generations. The counterintuitive lesson is that compounding produces nothing visible for a long time, which is precisely why impatient investors sell too soon.

A few extraordinary holdings carry the whole portfolio. Shelby Davis turned $50,000 into $370 million buying insurers and never selling, despite hundreds of dud picks. In Nalanda's first fund, seven of seventeen investments underperformed, yet Page Industries alone (up 82x over fourteen years) paid for all seven losers more than five times over. Prasad's costliest error was selling Shree Cement for a quick 2.2x gain; it later rose fivefold, a $400 million lesson in the tyranny of chasing internal rate of return over multiple.

The distinction between IRR (annualized rate) and multiple (total money returned) is where Prasad delivers his most actionable wealth-building insight. Optimizing for IRR biases toward early selling; optimizing for multiple rewards holding winners for decades. This is mathematically why the richest people on earth are overwhelmingly non-sellers of a single compounding asset. The pattern mirrors venture capital's power law, where one or two investments return the entire fund, though Prasad reaches the same destination by a different road. The endowment effect he confesses (loving his entrepreneurs) is usually a bias to overcome, but in a permanent-ownership model it becomes a feature that reinforces the discipline of not selling.

Win by repeating a simple process, like a honeybee swarm

Complexity yields to a repeatable algorithm. Honeybees make their most consequential decision, choosing a new home, through a stunningly simple process: scouts dance longer for better sites, and undecided bees randomly follow dancing sisters. This positive feedback loop reliably converges on the best available site without any leader. It does not succeed every time, but it has served bees brilliantly for thirty million years.

Nalanda's entire method is three repeatable steps:

1. Avoid big risks

2. Invest only in stellar businesses at a fair price

3. Own them forever

The failure of most investors, Prasad argues, is not choosing a wrong model but failing to repeat a good one consistently. Biologists spend lifetimes admitting how little they know about a single gene, while investors declare after a one-hour meeting that they have found the next great company. Humility about ignorance, encoded into a simple durable process, is the real edge.

Ending on the honeybee swarm (drawn from Thomas Seeley's research on collective decision-making) is a fitting capstone because it reframes the entire book as an argument for process over prediction. The swarm's genius is decentralized, rule-based, and robust to individual error, much like a checklist. Atul Gawande showed simple checklists slash surgical deaths; Nalanda's three rules function identically, protecting against the ego-driven improvisation that sinks most funds. The humility theme, that expanding knowledge reveals expanding ignorance, is Socratic and intellectually honest. The subtle risk is that a simple process, rigidly followed, can ossify into dogma when regimes genuinely shift. Prasad's saving grace is that his rules optimize for survival first, which forgives many errors.

Analysis

Pulak Prasad has written the rare investing book that is simultaneously a popular-science treatise, and both halves are load-bearing. As founder of Nalanda Capital, which compounded at 20.3% annually over fifteen years while beating Indian indices by nearly 11 points, he has earned the right to be contrarian. The book's structure mirrors his three-part strategy: avoid big risks, buy quality at a fair price, and be very lazy. Its distinctive move is using Darwinian biology not as decoration but as a genuine reasoning engine, drawing analogies from silver-fox domestication, sea-urchin development, dung-beetle horns, Galapagos finches, and honeybee democracy.

What elevates the work is intellectual honesty. Prasad opens by profiling his own $50 million failure and repeatedly names the businesses his method would have missed: Tesla, Eicher, Netflix, Amazon. He treats his strategy as a description, not a prescription, which paradoxically makes it more persuasive. The core epistemological stance, that investing is a historical science of interpretation rather than a predictive science of forecasting, is philosophically serious and aligns him with Gould over the DCF-wielding establishment.

The book's limitations are the mirror image of its strengths. Nalanda's model works because of structural advantages many cannot replicate: permanent committed capital from patient endowments, a concentrated portfolio, and a mandate to sit inactive for years. The convergence and stasis arguments, while empirically grounded, risk becoming rationalizations for avoiding genuinely novel opportunities. His dismissal of macro, management meetings, and DCF is bracing but occasionally overstated for rhetorical effect.

Still, the synthesis is original. Where most value investors cite Graham and Buffett, Prasad reaches for Zahavi's handicap principle, Kahneman's outside view, and Kurten's evolutionary rates, weaving them into a coherent philosophy of disciplined rejection, robustness, and radical patience. The analogies could feel gimmicky in lesser hands; here they illuminate. It is a book about knowing what you do not know, encoded into a process simple enough to repeat forever.

Review Summary

"What I Learned about Investing from Darwin" draws parallels between evolutionary biology and investment strategies. Readers praise Prasad's unique approach, combining Darwin's theories with financial insights. The book offers valuable lessons on risk avoidance, quality investments, and long-term thinking. Many appreciate Prasad's writing style, finding it engaging and accessible. While some critics note forced analogies and mathematical complexities, most reviewers commend the book's fresh perspective on investing. It's highly recommended for both finance professionals and those interested in evolutionary biology.

People Also Read

Glossary

Type I and Type II errors

Bad buys versus missed opportunitiesBorrowed from statistics. A Type I error (false positive, error of commission) is making a bad investment you wrongly thought was good, causing capital loss. A Type II error (false negative, error of omission) is rejecting a good investment you wrongly thought was bad, causing missed gains. Prasad argues investors should ruthlessly minimize Type I errors while tolerating many Type II errors, because good businesses are rare.

ROCE (Return on Capital Employed)

Operating profit over capital deployedOperating profit (earnings before interest and tax) divided by capital employed (net working capital plus net fixed assets, typically excluding excess cash). Nalanda uses historical ROCE as its single primary screen because a consistently high figure tends to signal strong management, durable competitive advantage, sound capital allocation, and a cash cushion, all correlated qualities inherited from one measurable trait.

Robustness

Resilience across multiple business layersPrasad's term (borrowed from Andreas Wagner) for a business's ability to function well despite internal and external shocks, achieved by being resilient on many fronts at once: high ROCE, no debt, fragmented customers and suppliers, strong moats, stable management, and a slow-changing industry. Robustness enables evolvability, meaning resilient businesses can adapt and grow without threatening their survival.

Proximate versus ultimate causes

Immediate triggers versus root driversFrom evolutionary biologist Ernst Mayr. Proximate causes are immediate mechanical influences (a Fed announcement moving a stock price today). Ultimate causes are the deep drivers of long-term success or failure (a business's competitive position and economics). Nalanda ignores proximate causes of price movement entirely and focuses only on the ultimate causes of business quality.

Convergence (in investing)

Success follows repeating proven templatesIn biology, unrelated organisms independently evolve the same solutions to the same problems (sharks and dolphins share body shapes). Prasad applies this to business: success and failure follow recurring patterns. Nalanda invests in proven business templates, not individual companies, always asking where else this model has worked before committing capital.

Outside view

Judging by statistical base ratesDaniel Kahneman's concept. The inside view builds an estimate from the specifics of a single case and personal optimism; the outside view uses base rates from many similar cases. Prasad pairs it with convergence: before analyzing one airline in depth, study the entire airline industry's dismal track record, which counsels avoidance regardless of the individual company's story.

Handicap principle

Only costly signals are honestAmotz Zahavi's theory that a biological signal is reliable only when it is costly to produce, like a peacock's dangerous tail that only healthy males can afford. Prasad applies it to corporate signals: cheap-to-fake communications (press releases, guidance, interviews) are ignored, while costly signals (decades of delivered performance, hard-won reputation via scuttlebutt) are trusted.

Grant-Kurten Principle of Investing (GKPI)

Exploit short swings, ignore long stabilityPrasad's coinage combining Bjorn Kurten's finding that evolution appears faster over short periods and slower over long ones, with the Grants' Galapagos finch studies. Applied to investing: a high-quality business fluctuates greatly short-term but stays fundamentally stable long-term, so investors should exploit temporary price drops to buy and never sell on short-term noise.

Punctuated equilibrium (in business)

Long stasis, rare abrupt changeGould and Eldredge's theory that species stay static for long periods, then change abruptly, rather than gradually. Prasad applies it to commerce: business stasis is the default, meaning great businesses stay great and bad ones stay bad for decades. This justifies buying rarely and selling even more rarely.

Belyaev silver fox experiment

Breeding tameness yielded dog traitsA Soviet experiment begun in 1959 by Dmitri Belyaev and Lyudmila Trut, still running. By breeding silver foxes solely for tameness, researchers accidentally produced floppy ears, curly tails, piebald coats, and juvenile faces within decades, because selecting one behavioral trait altered the hormones controlling many others. Prasad uses it to argue that one well-chosen investment screen (ROCE) delivers many virtues at once.

FAQ

What's What I Learned about Investing from Darwin about?

- Investment Philosophy: The book draws parallels between evolutionary biology and investing, suggesting that principles of natural selection can inform better investment strategies.

- Darwinian Principles: Concepts like natural selection and gradualism are applied to understand market dynamics and the longevity of companies.

- Long-Term Focus: Emphasizes the importance of long-term thinking in investing, akin to the slow processes of evolution.

Why should I read What I Learned about Investing from Darwin?

- Unique Perspective: Offers a fresh perspective by linking investing strategies to Darwinian principles, making it engaging for both investors and science enthusiasts.

- Practical Insights: Provides practical insights into avoiding common investment pitfalls and understanding the importance of quality in investment choices.

- Author's Experience: Pulak Prasad shares his extensive experience as an equity fund manager, providing credibility and real-world applications of his theories.

What are the key takeaways of What I Learned about Investing from Darwin?

- Avoid Big Risks: Prioritize risk management, as losing money is more detrimental than missing out on potential gains.

- High Quality at Fair Price: Invest in high-quality businesses that are fairly priced, ensuring long-term value creation.

- Be Very Lazy: Encourages investors to be patient and avoid frequent trading, allowing investments to grow over time without unnecessary interference.

How does What I Learned about Investing from Darwin relate evolutionary biology to investing?

- Natural Selection Analogy: Prasad draws parallels between the principles of natural selection and the investment process, suggesting that just as species evolve, so too must investors adapt their strategies.

- Robustness and Adaptability: Discusses how robust businesses, like resilient species, can adapt to changing environments and thrive over time.

- Learning from Nature: By observing the strategies of successful organisms, investors can glean insights into making better investment decisions.

What is the significance of "avoiding big risks" in What I Learned about Investing from Darwin?

- Core Principle: Prasad argues that the most fundamental rule in investing is to avoid significant losses, which can derail an investment career.

- Type I and Type II Errors: Discusses the concepts of type I errors (making bad investments) and type II errors (missing good investments), advocating for a focus on minimizing type I errors.

- Real-World Examples: Shares personal anecdotes and examples from his career to illustrate the importance of this principle in achieving long-term success.

How does Pulak Prasad define "high quality" in investing?

- Historical Return on Capital Employed (ROCE): Uses ROCE as a primary metric to assess business quality, looking for companies that have consistently delivered high returns.

- Sustainable Competitive Advantage: Emphasizes the need for businesses to have a sustainable competitive advantage, which allows them to maintain profitability over time.

- Management Quality: Suggests that high-quality management teams are often reflected in a company’s historical performance, particularly in its ROCE.

What does "buy high quality at a fair price" mean in the context of What I Learned about Investing from Darwin?

- Investment Strategy: This phrase encapsulates the second key strategy of Prasad's investment philosophy, focusing on acquiring businesses that are fundamentally strong but not overpriced.

- Valuation Metrics: Encourages investors to use various valuation metrics to determine if a business is fairly priced relative to its quality and growth potential.

- Long-Term Value Creation: By investing in high-quality businesses at fair prices, investors can expect sustainable growth and returns over the long term.

What does Prasad mean by "being very lazy" in investing?

- Patience Over Activity: Advocates for a patient approach to investing, suggesting that frequent trading can lead to poor decision-making and unnecessary costs.

- Long-Term Ownership: Emphasizes the importance of being a permanent owner of high-quality businesses, allowing them to grow without constant interference.

- Avoiding Market Noise: By being "lazy," investors can avoid being swayed by short-term market fluctuations and focus on the long-term performance of their investments.

What is thematic investing, and why is it cautioned against in What I Learned about Investing from Darwin?

- Definition of Thematic Investing: Involves focusing on trends or themes, such as electric vehicles or renewable energy, rather than the fundamentals of individual companies.

- Risks of Overvaluation: Highlights that many companies within a theme may be overvalued, as seen with examples like Nikola, which had a market value of $6 billion despite lacking a viable product.

- Historical Evidence: Argues that chasing themes can lead to poor investment decisions, as historical performance is often overlooked in favor of speculative trends.

What is the Grant–Kurtén principle of investing (GKPI)?

- Investment Model: States that when high-quality businesses do not fundamentally alter their character over the long term, investors should exploit short-term fluctuations for buying rather than selling.

- Long-Term Focus: Encourages investors to remain patient and not react impulsively to market volatility, allowing them to capitalize on attractive valuations.

- Empirical Evidence: Supports this principle with empirical data showing that many high-quality businesses have historically outperformed over extended periods.

How does the author suggest handling market fluctuations in What I Learned about Investing from Darwin?

- Ignore Short-Term Movements: Advises investors to disregard daily stock price fluctuations and focus on the long-term fundamentals of their investments.

- Use Fluctuations to Buy: Instead of selling during downturns, investors should view market fluctuations as opportunities to buy high-quality businesses at attractive prices.

- Stay Committed: Maintaining a long-term perspective allows investors to benefit from the compounding growth of their investments, even during periods of volatility.

What are the best quotes from What I Learned about Investing from Darwin and what do they mean?

- "Never lose money. Never forget rule number 1.": This quote from Warren Buffett encapsulates the core principle of risk management in investing.

- "A bad business that is dirt cheap? Pass.": Emphasizes the importance of quality over price in investment decisions.

- "We want to be permanent owners of high-quality businesses.": Reflects Prasad's long-term investment philosophy and commitment to sustainable growth.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.