Key Takeaways

Schools teach you to earn money, never to keep or grow it

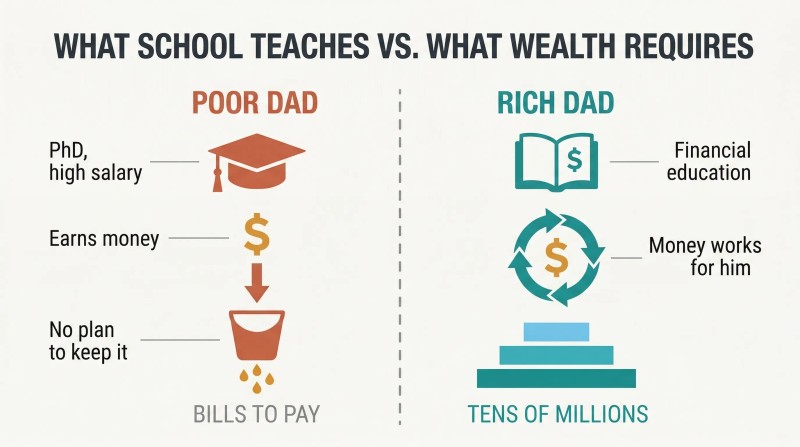

Kiyosaki grew up with two fathers. His biological dad ("poor dad") held a PhD, served as Hawaii's head of education, and earned a substantial salary — yet died leaving bills to be paid. His best friend Mike's father ("rich dad") never finished eighth grade but became one of Hawaii's richest men, leaving tens of millions to his family and charities. The difference wasn't intelligence or income — it was financial education.

Schools prepare you to work for money, not to make money work for you. Rich dad taught Kiyosaki that the education system produces employees, never investors or business owners. This gap explains why smart bankers, doctors, and accountants struggle financially while some high school dropouts build empires. The subject of money, rich dad insisted, is taught at home — if it's taught at all.

Learn one rule: assets put money in your pocket, liabilities take it out

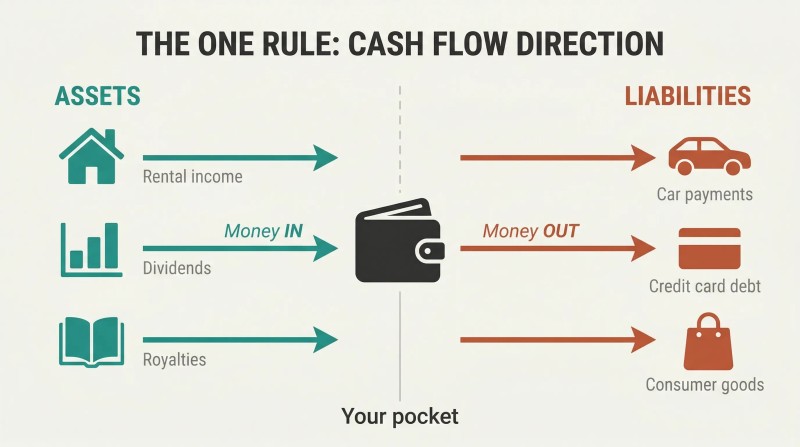

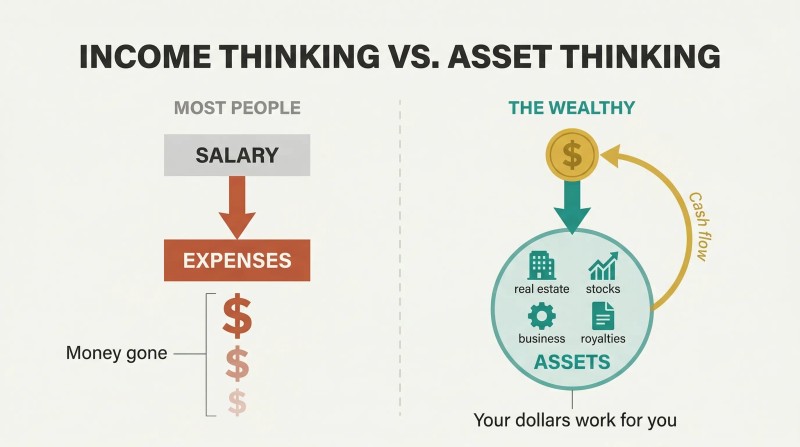

Rich dad's Rule #1 is deceptively simple: know the difference between an asset and a liability, and only buy assets. By Kiyosaki's cash-flow definitions, an asset generates income into your pocket whether you work or not — rental properties, dividend stocks, royalties. A liability drains cash out — car payments, credit card debt, consumer goods.

Most people confuse the two. Conventional accounting lets you list cars, furniture, and golf clubs as "assets," but they produce no income. Kiyosaki uses simple cash-flow diagrams to show three patterns: the poor spend everything on expenses, the middle class funnel income into liabilities disguised as assets, and the rich buy assets whose income funds more assets. The direction of cash flow — not the dollar amount on your paycheck — determines your financial destiny.

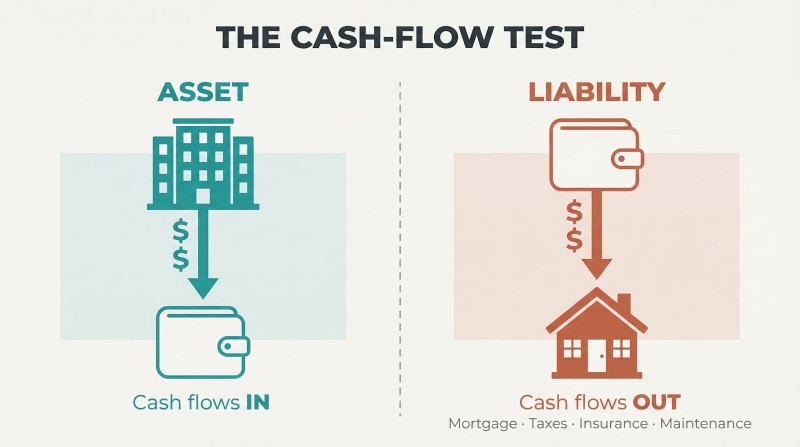

Your house is likely your biggest liability, not your best asset

This is the book's most controversial claim. Rich dad called his home a liability; poor dad called his home his greatest investment. By the cash-flow test, a personal residence fails: mortgage payments, property taxes, insurance, and maintenance all drain your pocket. The 2008 housing crash proved millions of homeowners painful agreement.

Over-investing in a home carries three hidden costs:

1. Loss of time during which other assets could have grown in value

2. Loss of capital spent on maintenance instead of income-producing investments

3. Loss of investment education from never having money to invest

Kiyosaki doesn't say never buy a house — he says buy income-generating assets first, then let their cash flow pay for the house.

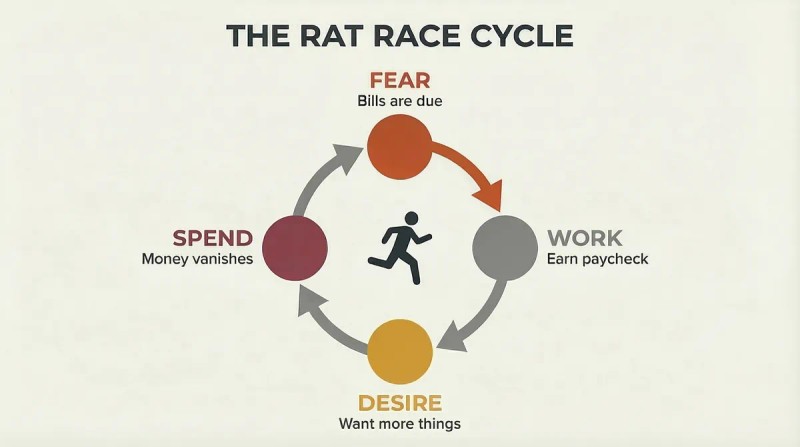

The paycheck cycle is a trap driven by fear and greed

Kiyosaki calls this cycle the Rat Race. Fear of not paying bills drives you to work. Then desire kicks in: your paycheck sparks visions of new cars, vacations, bigger houses. You spend, the money vanishes, and fear returns Monday morning. Like a donkey chasing a carrot, the paycheck always dangles just out of reach. Offer people more money and they simply increase their spending.

At nine years old, Kiyosaki learned this viscerally. Rich dad had him work for nothing at a convenience store, then offered escalating pay — 25 cents, a dollar, two dollars, finally five dollars an hour (a fortune in 1956). Kiyosaki resisted, learning that everyone has a price and the cycle breaks only when you stop reacting emotionally and start thinking strategically about money.

Build your asset column, not your resume or salary

Ray Kroc once told MBA students he wasn't in the hamburger business — he was in real estate. McDonald's is the world's largest single owner of real estate. The franchise sells burgers; the business is the land underneath. Rich dad taught the same principle: your profession is your job, but your business is your asset column.

Most people chase raises and promotions — income-column thinking. The rich focus on the balance sheet, acquiring assets that produce cash flow: businesses they don't run daily, stocks, bonds, income-generating real estate, and royalties. Keep your day job, but funnel every spare dollar into assets. Kiyosaki defines wealth not as net worth, but as the number of days you could survive if you stopped working today. When asset income covers expenses, you're wealthy — even before you're rich.

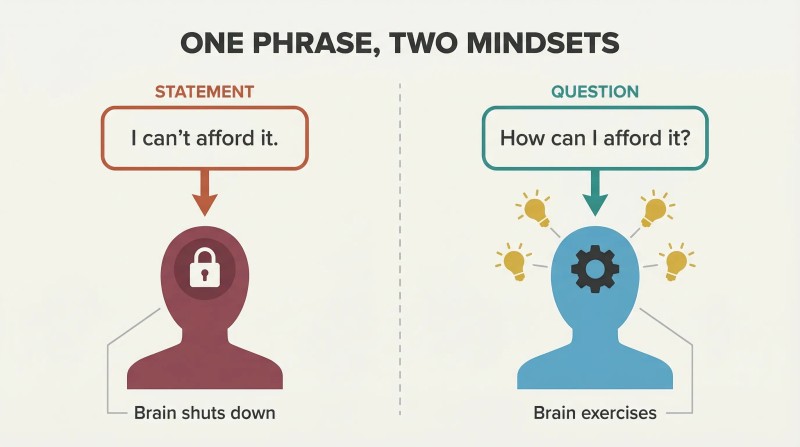

Ask 'How can I afford it?' — never say 'I can't'

This phrase swap separates mindsets. Poor dad frequently said "I can't afford it," shutting down his brain. Rich dad banned those words and insisted on the question "How can I afford it?" One is a statement that kills possibilities; the other forces creative problem-solving. Rich dad wasn't concerned about what Kiyosaki wanted to buy, as long as the question was exercising his mind like a muscle.

The same principle cures hidden laziness. Kiyosaki argues the most common form of laziness isn't lying on a couch — it's staying busy to avoid confronting financial problems. The antidote: a little greed. Ask "What would my life look like if I never had to work again?" That desire creates energy. Without it, progress stalls. Too much greed corrodes, but too little guarantees mediocrity.

The rich legally pay less tax by earning through corporations

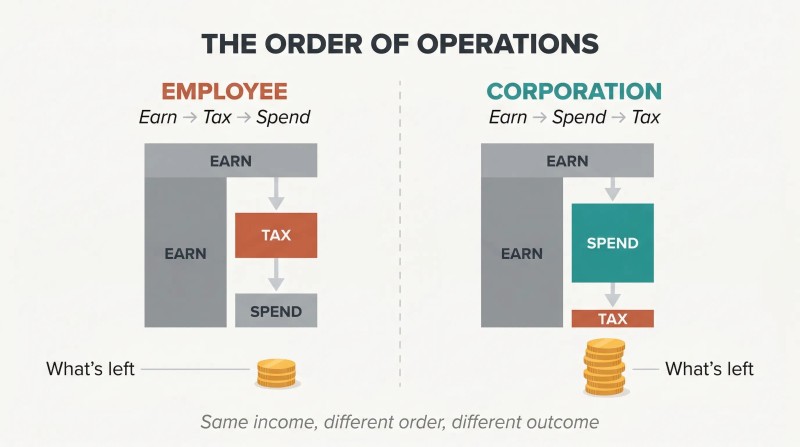

Taxes were designed to punish the rich — but the rich adapted. Income tax was first permanently imposed in England (1874) and America (1913), sold to voters as targeting only the wealthy. But as government spending grew, taxes trickled down to the middle class and poor — the very people who'd voted for them. Meanwhile, the rich discovered corporations.

The order of operations is everything. Employees earn, get taxed, then spend what's left. Corporations earn, spend on legitimate pre-tax expenses (travel, vehicles, insurance, meals), then pay taxes on whatever remains. This legal difference means the rich keep more of every dollar. Kiyosaki calls this awareness one pillar of Financial IQ — alongside accounting, investing, and understanding markets — that together create true financial intelligence.

Master selling — the one skill separating talented-poor from wealthy

A Singapore reporter wanted to become a bestselling author. When Kiyosaki suggested she take a sales course, she was offended — she had a master's in English literature. He pointed to his book cover: "It says best-selling author, not best-writing author." She stormed off. Kiyosaki admits he's a terrible writer who attended sales school. Combined, those skills produced a book on the New York Times bestseller list for nearly seven years.

Rich dad told Kiyosaki to know a little about a lot. That's why Kiyosaki quit a high-paying merchant marine job, joined the Marines to learn leadership, then worked at Xerox specifically to conquer his fear of rejection through their sales-training program. The most critical skills aren't technical — they're sales, marketing, communication, and managing people. McDonald's makes more money than better cooks because it mastered business systems, not hamburgers.

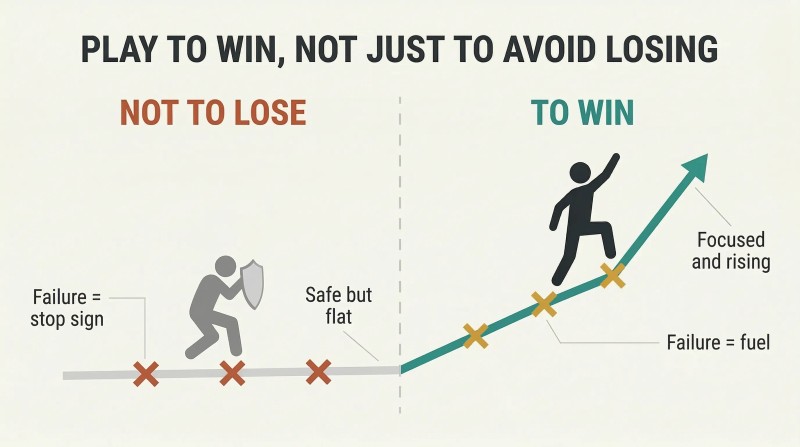

Play to win, not just to avoid losing

Rich dad loved the Texan attitude. Texans are proud when they win and brag when they lose. The Alamo was a devastating military defeat, but "Remember the Alamo!" became a rallying cry for victory. Rich dad used this story whenever he was nervous before a big deal — failure was fuel, not a stop sign.

A balanced portfolio means playing not to lose. Most people's retirement sits in CDs, low-yield bonds, and mutual funds — safe, but not a winning strategy. Kiyosaki argues that with limited capital, you must focus, not diversify. Thomas Edison, Bill Gates, and George Soros weren't balanced — they were intensely focused. The pain of losing money keeps 90 percent of Americans from ever winning financially. Cynics criticize; winners analyze. And the worst of times, Kiyosaki insists, is actually the best time to invest.

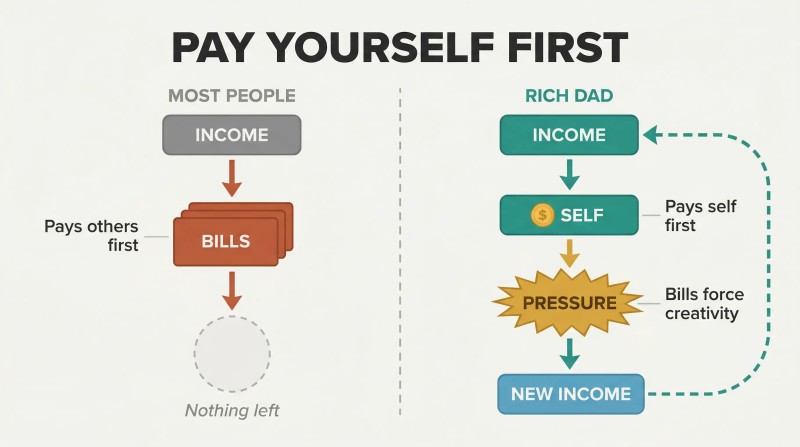

Pay yourself first — the pressure will force you to earn more

Rich dad always paid himself first — even before creditors. Poor dad, like most people, paid everyone else first and had nothing left. Rich dad's logic: if you pay yourself last, there's no pressure to find more income. But when bill collectors are screaming and you've already invested your money, the urgency forces you to think creatively — start a side business, trade stocks, generate new income sources.

This isn't permission to dodge bills. Kiyosaki emphasizes avoiding consumer debt entirely. The formula:

1. Keep expenses low and avoid large debt positions

2. When cash is short, let pressure sharpen your financial instincts instead of raiding investments

He credits this single habit — perhaps more than any other — as the number-one factor separating the rich from the poor and middle class. Self-discipline with money is the foundation everything else builds on.

Analysis

Rich Dad Poor Dad is, at its core, an accounting primer disguised as a parable. Kiyosaki's genius lies not in the sophistication of his financial ideas — most CFAs would find them elementary — but in the narrative delivery system. The "two dads" device transforms abstract concepts like cash-flow direction and balance-sheet management into emotionally charged father-son drama, making dry accounting principles sticky and shareable. This explains why the book has sold over 40 million copies despite, or perhaps because of, its simplicity.

The book's most durable contribution is reframing " asset " and " liability " from accounting-textbook definitions into cash-flow-based ones. This single shift — does this thing put money in your pocket or take it out? — gives financially illiterate readers an immediate heuristic for evaluating every financial decision. The "your house is not an asset" provocation, while technically incomplete (it ignores equity buildup, inflation hedging, and imputed rent savings), powerfully counteracts the American cultural bias toward over-leveraging into housing at the expense of productive investment.

However, the book carries significant blind spots. It exhibits survivorship bias: Kiyosaki generalizes from his own trajectory and rich dad's success without acknowledging that most entrepreneurial ventures fail. His dismissal of professional specialization contradicts substantial labor economics research showing that skill premiums drive income growth for most workers. The corporate-tax-avoidance advice, while legally sound in principle, is vastly oversimplified for readers without existing capital or access to good counsel. And the book is virtually silent on systemic barriers — race, class, geography — that shape who can realistically "choose" to be rich.

Still, the book succeeds at what it actually attempts: shifting readers from an income mindset to a cash-flow mindset, from consumer thinking to investor thinking, and from financial passivity to financial agency. A quarter century later, the vocabulary it popularized — Rat Race, asset column, cash flow — has become the lingua franca of popular financial literacy, proving that well-executed simplification can be more transformative than sophistication.

Review Summary

Readers praise "Rich Dad Poor Dad" for its eye-opening insights on financial literacy and mindset shifts. Many credit it with changing their perspective on money and motivating them to take control of their finances. However, some criticize the book for oversimplification, repetitiveness, and lack of concrete advice. Despite mixed opinions, most agree it's thought-provoking and motivational, even if not a comprehensive guide to wealth-building.

People Also Read

Glossary

Rat Race

The earn-spend-repeat paycheck trapKiyosaki's term for the cycle in which people work to earn money, spend it on expenses and liabilities, then must work again to pay new bills. Driven by two emotions—fear of not having enough money and greed for what money can buy—the Rat Race persists regardless of income level because higher earnings trigger proportionally higher spending and taxes, trapping people in permanent dependence on their paychecks.

CASHFLOW Quadrant

Four ways people earn incomeA framework dividing income earners into four categories based on where their cash comes from: E (Employee), S (Self-employed), B (Business Owner), and I (Investor). The left side (E and S) involves trading personal time for money. The right side (B and I) involves building systems and assets that generate income independently of the owner's daily labor. Kiyosaki advocates migrating from the left side to the right side to achieve financial freedom.

Financial IQ

Four combined financial skill areasKiyosaki's measure of financial intelligence, comprising four domains: (1) Accounting—the ability to read and interpret financial statements, (2) Investing—strategies for making money generate more money, (3) Understanding markets—knowledge of supply, demand, and current conditions, and (4) The law—awareness of tax advantages and legal protections, especially through corporate structures. Kiyosaki argues the synergy of all four creates the capacity to build and protect wealth.

Doodad

Non-essential consumer expense itemA term from Kiyosaki's CASHFLOW board game representing impulse purchases and non-essential consumer goods that drain cash without generating any return. Examples include boats, luxury electronics, and items bought on credit. In the game, drawing a doodad card increases a player's expenses and makes escaping the Rat Race harder—mirroring real-life spending habits that prevent wealth accumulation.

Asset (rich dad's definition)

Puts money in your pocketIn Kiyosaki's framework, an asset is anything that generates positive cash flow—putting money into your pocket whether you work or not. This differs from conventional accounting definitions that classify personal property (cars, furniture) as assets. Kiyosaki's examples include rental real estate, dividend-paying stocks, bonds, businesses that run without the owner's daily presence, and royalty-producing intellectual property.

Liability (rich dad's definition)

Takes money from your pocketIn Kiyosaki's framework, a liability is anything that takes money out of your pocket through ongoing costs. This notably includes items traditionally listed as assets by banks—such as a personal home (mortgage, taxes, maintenance), cars (loan payments, insurance, depreciation), and consumer goods bought on credit. The distinguishing test is cash-flow direction: if owning it costs you money month after month, it is a liability regardless of what a balance sheet says.

FAQ

What's Rich Dad Poor Dad about?

- Contrasting Perspectives: The book contrasts the financial philosophies of Robert Kiyosaki's two father figures—his biological father (Poor Dad) and his best friend's father (Rich Dad). Poor Dad emphasizes job security and traditional education, while Rich Dad advocates for financial education and investing.

- Financial Education: Kiyosaki argues that traditional schooling fails to teach essential financial skills, leading to a cycle of working for money rather than having money work for you.

- Wealth Creation Lessons: The book outlines key lessons from Rich Dad, such as investing in assets rather than liabilities and understanding how the rich think differently about money.

Why should I read Rich Dad Poor Dad?

- Transformative Mindset: The book can shift your perspective on money and wealth, encouraging you to think like the rich and challenge conventional beliefs about work and financial security.

- Practical Financial Lessons: It provides actionable advice on building wealth through investing in assets, understanding taxes, and leveraging financial education.

- Inspiration for Independence: Kiyosaki's personal anecdotes motivate readers to take control of their financial futures and seek financial education and independence.

What are the key takeaways of Rich Dad Poor Dad?

- Assets vs. Liabilities: Understanding the difference is crucial for building wealth. Rich people acquire assets, while the poor and middle class acquire liabilities they think are assets.

- Financial Literacy: Kiyosaki stresses that financial literacy is essential for becoming rich, involving understanding money, accounting, investing, and market dynamics.

- Mind Your Own Business: Focus on building your asset column rather than solely relying on your income statement, investing in income-generating assets.

What are the best quotes from Rich Dad Poor Dad and what do they mean?

- "The rich don’t work for money.": Wealthy individuals focus on making their money work for them through investments and assets, rather than trading time for money in a job.

- "Savers are losers.": Saving money in a low-interest environment does not build wealth; investing in assets that generate cash flow is more effective.

- "Your house is not an asset.": While many view their homes as investments, they often incur expenses and do not generate income, making them liabilities in Kiyosaki's view.

What is the difference between an asset and a liability according to Rich Dad Poor Dad?

- Asset Definition: An asset is something that puts money in your pocket, such as investments like real estate, stocks, and businesses that generate income.

- Liability Definition: A liability takes money out of your pocket, including expenses like mortgages, car payments, and other debts that do not generate income.

- Understanding Importance: Grasping this difference is crucial for financial success, as many mistakenly consider liabilities as assets, leading to financial struggles.

How does Rich Dad Poor Dad address the concept of financial education?

- Education Gap: Kiyosaki points out that money is not taught in schools, leading many to struggle financially despite academic qualifications.

- Learning from Experience: The book emphasizes learning about money through real-life experiences and mentorship rather than traditional schooling.

- Seek Knowledge: Kiyosaki encourages readers to actively seek financial education and develop their financial intelligence, including understanding accounting, investing, and market dynamics.

What is the CASHFLOW Quadrant in Rich Dad Poor Dad?

- Four Income Sources: The CASHFLOW Quadrant categorizes individuals into four groups based on their income sources: Employee (E), Self-employed (S), Business Owner (B), and Investor (I).

- Path to Freedom: To achieve financial independence, individuals should aim to transition from the E and S quadrants to the B and I quadrants, allowing for greater wealth-building potential.

- Assess Your Position: The quadrant helps readers assess their current financial situation and identify areas for growth, making informed decisions about their financial future.

How does Rich Dad Poor Dad suggest one should build wealth?

- Focus on Assets: Kiyosaki advises buying assets that put money in your pocket, such as income-generating properties, stocks, and businesses.

- Mind Your Own Business: Emphasizes focusing on your asset column rather than just your job, actively seeking opportunities to invest and grow wealth.

- Continuous Learning: Stresses the need for ongoing financial education and adapting to changing market conditions, seizing opportunities that others miss.

What is the Rat Race as described in Rich Dad Poor Dad?

- Definition: The Rat Race refers to the cycle of working hard for money, only to spend it on liabilities and expenses, a trap many find themselves in.

- Cycle of Debt: As people earn more, they often spend more, leading to increased debt and financial stress, perpetuating the struggle for financial security.

- Breaking Free: Encourages readers to break free by focusing on building assets and creating passive income streams, essential for achieving financial independence.

What is the importance of paying yourself first according to Rich Dad Poor Dad?

- Self-Discipline: Paying yourself first is a crucial habit for building wealth, ensuring you prioritize saving and investing over spending on liabilities.

- Financial Pressure: Creates urgency to generate additional income to cover expenses, motivating you to seek new opportunities and increase financial intelligence.

- Long-Term Wealth: Consistently paying yourself first helps grow your asset column over time, leading to greater financial security and independence.

How can I start applying the lessons from Rich Dad Poor Dad?

- Invest in Education: Begin by reading books, attending seminars, and seeking resources that enhance your financial literacy, as knowledge is the foundation for sound financial decisions.

- Identify Assets: Track your income and expenses to understand your assets and liabilities, focusing on acquiring assets that generate passive income.

- Take Action: Actively seek opportunities, whether investing in real estate or starting a business, as taking action is crucial for building wealth.

How do I find a good broker or financial advisor according to Rich Dad Poor Dad?

- Research and Interview: Look for brokers or advisors with a proven track record and experience in your areas of interest, interviewing them to understand their investment philosophy.

- Check Their Investments: A good broker should have personal investments in the market they advise on, demonstrating commitment and understanding.

- Value of Information: Choose brokers who provide valuable insights and education, not just sales pitches, as knowledgeable brokers can save you time and help make informed decisions.

Rich Dad Series

About the Author

Other books by Robert T. Kiyosaki

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.