Key Takeaways

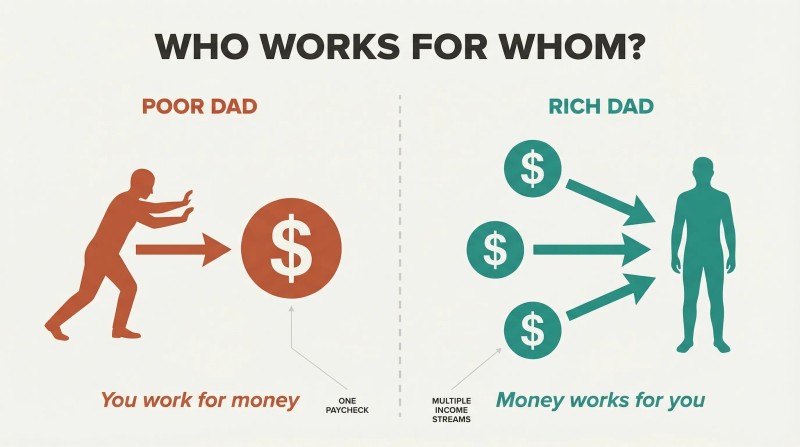

Schools teach you to work for money — the rich learn the opposite

Kiyosaki grew up with two dads. His "poor dad" was his biological father — a PhD, superintendent of education in Hawaii — who earned well but died leaving bills to be paid. His "rich dad" was his friend Mike's father — an eighth-grade dropout who became one of the wealthiest men in Hawaii. Both worked hard. The difference was financial education.

Poor dad said "get good grades, find a secure job." Rich dad said "learn how money works and make it work for you." At age 9, Robert chose rich dad's path. Over 30 years, rich dad taught him six lessons about money — lessons never covered in school. Most people spend their lives earning paychecks, while the wealthy build systems that generate income without their direct labor.

Buy things that put money in your pocket, not things that take it out

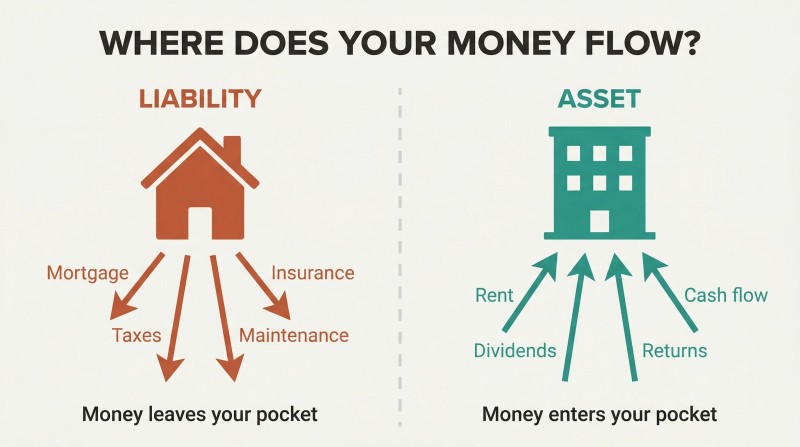

Rich dad's Rule #1 is deceptively simple: know the difference between an asset and a liability. Forget accounting jargon. An asset puts money in your pocket — rental properties, dividend stocks, royalty-producing intellectual property. A liability takes money out — car payments, credit card debt, consumer loans.

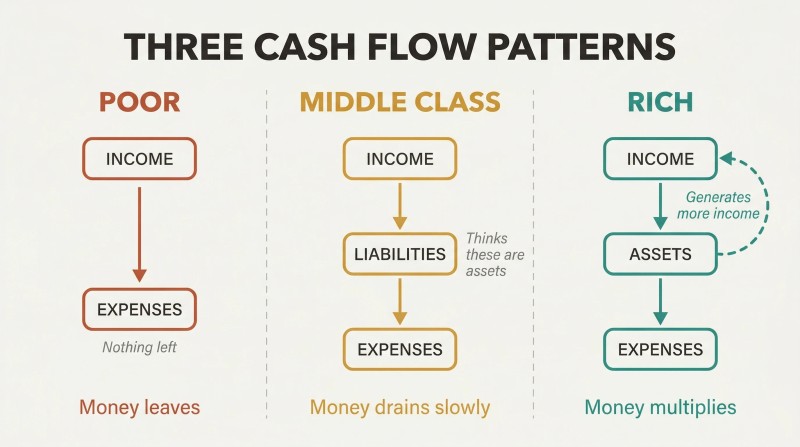

The cash flow pattern tells the whole story. Poor people's income flows straight to expenses. The middle class earns more but channels it into liabilities they mistake for assets — bigger mortgages, nicer cars, club memberships. The wealthy funnel income into assets first, then let those assets generate income that covers expenses. The simplicity is exactly why adults miss it: they've been educated by professionals who never learned these distinctions themselves.

Your home is probably your biggest liability, not your best investment

This is Kiyosaki's most controversial claim. Conventional wisdom calls your house your greatest asset, but rich dad pointed out that a house takes money out of your pocket every month: mortgage payments, property taxes, maintenance, insurance, and utilities. It produces no income. By the cash-flow definition of assets and liabilities, that makes it a liability.

The real cost is missed opportunity. Money locked in a house can't work in income-producing assets. Kiyosaki isn't saying never buy a home — he's saying understand what it actually is. When his wife wanted a Mercedes, the couple waited four years until their apartment buildings generated enough extra cash flow to cover the car payment. The luxury cost nothing from their earned income.

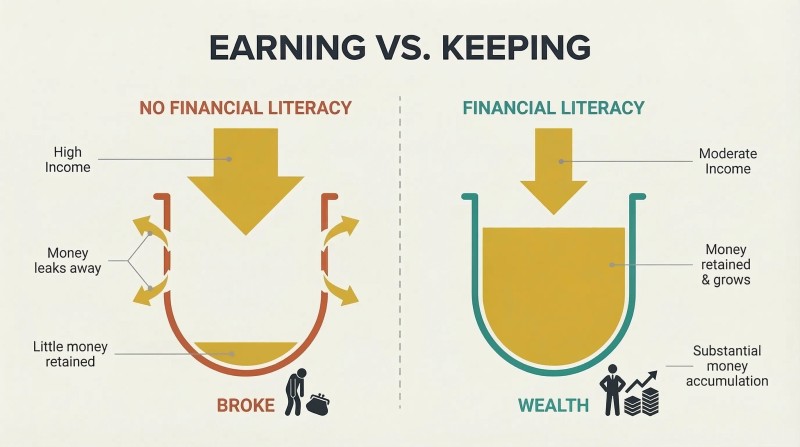

It's not how much you earn — it's how much you keep and grow

Lottery winners go broke; so do millionaire athletes. Kiyosaki cites a championship basketball player earning millions who, by 29, was working at a car wash — his entourage had taken everything. He also references nine of America's wealthiest men from 1923 who within 25 years ended up broke, insane, imprisoned, or dead by suicide.

The real skill is financial aptitude — knowing how to keep money, grow it, and prevent others from taking it. A pay raise doesn't fix bad cash-flow patterns; it accelerates them. Money "only accentuates the cash flow pattern running in your head," Kiyosaki writes. If your habit is to spend everything you get, more income just means more spending. The foundation of lasting wealth isn't earning power — it's financial literacy.

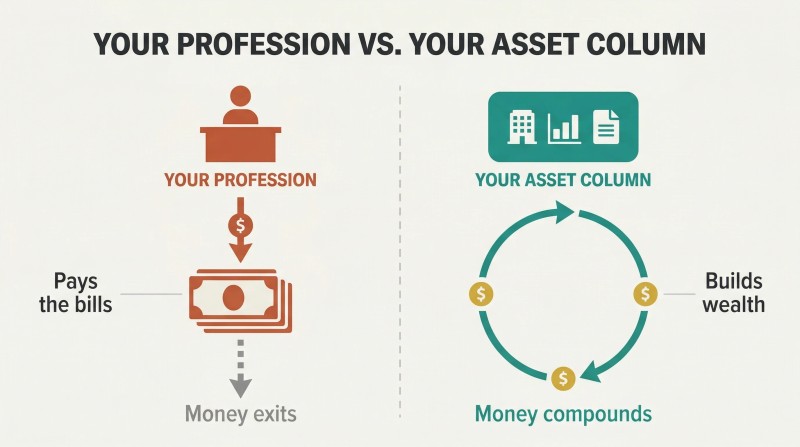

Your profession pays the bills; your asset column builds wealth

Ray Kroc asked MBA students what business McDonald's was in. "Hamburgers," they laughed. Wrong. "My business is real estate," Kroc said. Each franchise was a vehicle to acquire America's most valuable intersections. Today, McDonald's owns more real estate than the Catholic Church.

Your profession is your income; your business is your asset column. Kiyosaki kept his Xerox day job while building real estate on the side. By 1978, his investment corporation earned more than his salary. Real assets include businesses that run without you, stocks, bonds, income-generating real estate, and royalties. Once a dollar enters your asset column, treat it as an employee working 24 hours a day — never let it leave.

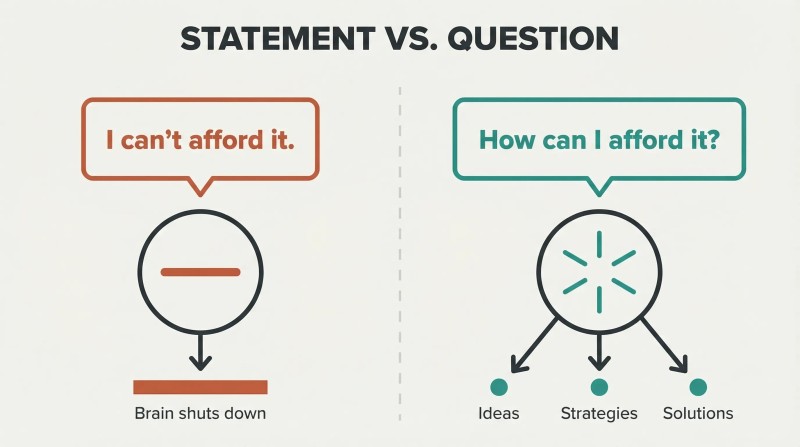

Replace 'I can't afford it' with 'How can I afford it?'

One dad shut down; the other activated. Poor dad habitually said "I can't afford it" — a statement that lets the brain off the hook. Rich dad forbade those words and insisted on the question "How can I afford it?" The statement is an endpoint; the question forces your mind to search for strategies, solutions, and creative options.

This connects to Kiyosaki's cure for laziness. The most common laziness isn't idleness — it's staying busy to avoid the uncomfortable work of building wealth. The antidote is a touch of healthy desire. Ask yourself what Kiyosaki calls the WII-FM question: "What's In It For Me?" What would life look like without a mandatory paycheck? That desire creates the mental energy to find answers rather than excuses.

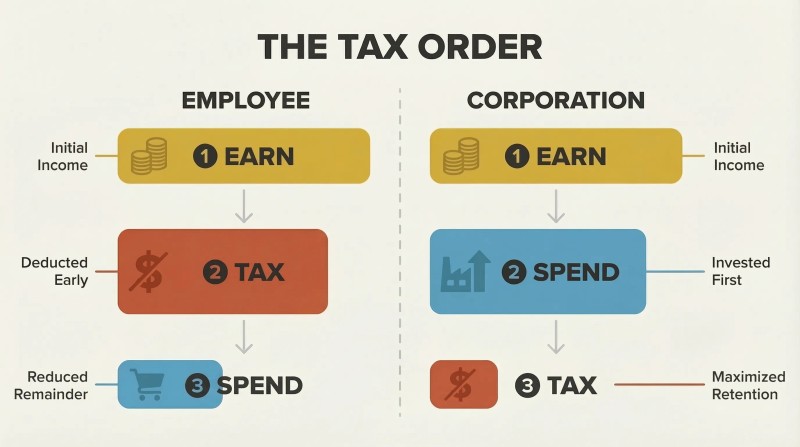

The rich use corporations to earn, spend, then pay taxes — in that order

Taxes were sold as punishment for the rich. U.S. income tax became permanent in 1913, marketed as targeting only the wealthy. But the rich adapted by using corporations, and the tax burden trickled down to the middle class. Average Americans now work five to six months per year just to cover their taxes.

The corporate structure flips the tax equation. Corporations pay expenses with pre-tax dollars — vehicles, travel, insurance, meals — then get taxed only on the remainder. Kiyosaki's Financial IQ combines four skills to exploit this:

1. Accounting — reading financial statements

2. Investing — making money produce money

3. Understanding markets — supply and demand

4. The law — tax advantages and asset protection

Pick jobs for the skills they teach, not the salary they pay

A Singapore journalist told Kiyosaki she wanted to be a best-selling author. He suggested a sales course. She was offended — she had a master's in English Literature. Kiyosaki pointed to her notes: "It says best-selling author, not best-writing author." He was a terrible writer but a trained salesman. She was gifted but couldn't sell.

Most people are one skill away from great wealth. Kiyosaki quit a lucrative shipping career to join the Marines (to learn leadership), then worked at Xerox (to conquer his fear of sales rejection). Rich dad advised knowing "a little about a lot" rather than specializing narrowly. The critical skills aren't technical — they're sales, marketing, communication, and managing people. McDonald's doesn't make the best burger; they run the best business system.

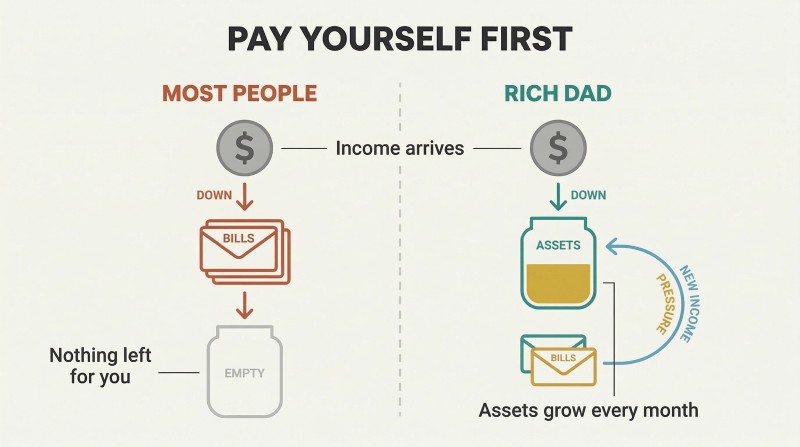

Pay yourself first — let creditor pressure fuel your creativity

Rich dad paid himself before anyone else — including the government. When Kiyosaki asked what happened if he came up short, rich dad explained the pressure from creditors forced him to find new income — side ventures, stock trades, extra deals. Paying himself last would have killed the motivation. Borrowed from George Clason's The Richest Man in Babylon, the pay-yourself-first principle requires the guts to resist the world pushing you around.

Most people do the opposite. They pay every bill, then save whatever remains — usually nothing. Kiyosaki's rules: keep consumer debt minimal, live below your means, but always fund your asset column before creditors. Don't dip into savings to cover bills. Use the discomfort of owing to generate new income instead.

Play to win, not just to avoid losing

Rich dad loved the Texan attitude toward failure. "Remember the Alamo" transformed a devastating military defeat into a rallying cry that built Texas. Rich dad told this story before every risky deal — it reminded him that losses could be converted into wisdom and determination. Colonel Sanders was turned down 1,009 times before someone bought his fried chicken recipe. He started at age 66.

Over 90% of Americans play not to lose. They build "balanced" portfolios — safe, sensible, but never winning. Kiyosaki argues that with limited capital, focus beats diversification. Edison, Gates, and Soros didn't spread thin early — they concentrated intensely. School punishes mistakes, but real wealth rewards people who learn from them. Winners hate losing but aren't paralyzed by the possibility.

Analysis

Rich Dad Poor Dad is perhaps the most culturally influential personal finance book ever published — and also one of the most debated. Its power lies not in technical sophistication but in narrative framing: the 'two dads' device gives readers permission to question financial assumptions inherited from parents, teachers, and institutions. Kiyosaki doesn't merely teach concepts; he reframes the entire middle-class script — study hard, get a secure job, save for retirement — as an outdated trap.

The book's core intellectual contribution is the asset/liability distinction defined by cash flow rather than accounting convention. This is simultaneously its greatest strength and weakness: the simplicity makes it accessible to millions who would never open an accounting textbook, but the oversimplification invites legitimate criticism. Calling your home a 'liability' ignores equity accumulation, forced savings, and hedging against rent inflation. His corporate tax advice, while directionally accurate, glosses over the complexity, costs, and legal risks of actual implementation.

What's most interesting from a behavioral economics perspective is how Kiyosaki anticipated concepts researchers would later formalize. The fear-greed cycle mirrors Kahneman's loss aversion. The Rat Race describes hedonic adaptation on a financial treadmill. 'How can I afford it?' is essentially cognitive restructuring, a technique psychologists now teach in clinical settings. The emphasis on financial education as the determining variable predates widespread institutional concern about financial literacy by over a decade.

The book's greatest blind spot is survivorship bias. Kiyosaki's personal deal examples read like a highlight reel without adequate discussion of the timing, risk tolerance, market conditions, and luck involved. His dismissal of diversification contradicts decades of portfolio theory. Yet the book's lasting impact is undeniable — it shifted millions of readers from 'how do I earn more?' to 'how do I make what I earn work harder?' That paradigm shift, however imperfectly argued, remains its enduring contribution to financial culture and the reason it has sold over 30 million copies.

Review Summary

Rich Dad Poor Dad receives mixed reviews. Many readers find it motivational and praise its accessible explanation of financial concepts, encouraging them to think differently about money and assets. However, critics argue the book lacks concrete advice, oversimplifies complex issues, and promotes potentially risky financial strategies. Some readers appreciate Kiyosaki's personal anecdotes and emphasis on financial education, while others find his writing style repetitive and his success claims questionable. The book's popularity and influence on personal finance are widely acknowledged, despite its controversial aspects.

People Also Read

Glossary

Rat Race

Earn-spend-owe cycle trapping workersKiyosaki's term for the endless cycle most people are trapped in: earning a paycheck, paying bills, and accumulating liabilities while never building income-producing assets. Driven by fear of not having enough money and desire for things money can buy. In his CASHFLOW board game, it is the inner track players must escape by building passive income that exceeds their monthly expenses.

Fast Track

Financial freedom zone beyond paychecksThe outer track in Kiyosaki's CASHFLOW board game, representing financial independence. Players reach it when their passive income from assets exceeds monthly expenses, meaning they no longer depend on a job. It simulates how the wealthy operate—generating wealth through investments and business ownership rather than trading time for a paycheck.

Financial IQ

Four-skill composite for building wealthKiyosaki's composite measure of financial intelligence, comprising four technical skills: (1) accounting—the ability to read and understand financial statements, (2) investing—strategies for making money produce more money, (3) understanding markets—grasping supply and demand dynamics, and (4) knowledge of the law—especially tax advantages and asset protection through corporate structures. The synergy of all four enables wealth building.

Doodad

Cash-draining luxury or unnecessary expenseA term from Kiyosaki's CASHFLOW board game for unnecessary luxury purchases that consume cash flow without generating income—boats, gadgets, vacations bought on credit. Drawing a doodad card increases expenses and makes escaping the Rat Race harder, mirroring how real-life impulse spending traps people in the earn-and-spend cycle by preventing capital from reaching the asset column.

Pay Yourself First

Fund assets before paying billsA principle Kiyosaki adopted from George Clason's The Richest Man in Babylon. It means allocating money to your asset column—investments that generate passive income—before paying bills, taxes, or creditors. The resulting financial pressure from unpaid obligations motivates finding additional income sources rather than simply depleting savings. Kiyosaki considers this the hardest but most important financial habit to master.

1031 exchange

Tax-deferred real estate reinvestment swapA provision under Section 1031 of the U.S. Internal Revenue Code that Kiyosaki frequently used. It allows real estate investors to defer paying capital gains taxes when selling a property, provided proceeds are reinvested into a property of equal or greater value. Kiyosaki used successive 1031 exchanges to grow a $5,000 investment into properties worth over a million dollars without paying taxes along the way.

FAQ

What's "Rich Dad Poor Dad" about?

- Dual Perspectives: "Rich Dad Poor Dad" by Robert T. Kiyosaki contrasts the financial philosophies of his two fathers: his biological father (Poor Dad) and his best friend's father (Rich Dad).

- Financial Education: The book emphasizes the importance of financial literacy and how it can lead to financial independence.

- Mindset Shift: It challenges conventional beliefs about money, work, and education, advocating for a mindset that focuses on building assets rather than relying solely on earned income.

- Practical Lessons: Through personal anecdotes, Kiyosaki shares lessons on investing, entrepreneurship, and financial management.

Why should I read "Rich Dad Poor Dad"?

- Financial Literacy: It provides insights into financial education that are often missing from traditional schooling.

- Mindset Change: The book encourages readers to think differently about money and wealth creation.

- Practical Advice: Offers actionable advice on how to build wealth through investments and entrepreneurship.

- Inspiration: It inspires readers to take control of their financial future and pursue financial independence.

What are the key takeaways of "Rich Dad Poor Dad"?

- Assets vs. Liabilities: Understanding the difference between assets (which put money in your pocket) and liabilities (which take money out).

- Financial Independence: The importance of creating passive income streams to achieve financial freedom.

- Mind Your Own Business: Focus on building and managing your own assets rather than working for someone else.

- Financial Education: Continuous learning and financial literacy are crucial for wealth building.

What are the best quotes from "Rich Dad Poor Dad" and what do they mean?

- "The rich don’t work for money." This quote emphasizes the importance of having money work for you through investments and passive income.

- "It’s not how much money you make, but how much money you keep." Highlights the significance of financial management and saving.

- "The single most powerful asset we all have is our mind." Encourages investing in financial education and personal development.

- "The love of money is the root of all evil." vs. "The lack of money is the root of all evil." Contrasts the perspectives of Poor Dad and Rich Dad on money's role in life.

How does Robert T. Kiyosaki define assets and liabilities?

- Assets: According to Kiyosaki, assets are things that put money in your pocket, such as investments, real estate, and businesses.

- Liabilities: Liabilities are things that take money out of your pocket, like mortgages, car loans, and credit card debt.

- Financial Misunderstanding: Many people mistakenly consider liabilities as assets, such as a personal home, which can lead to financial struggles.

- Cash Flow: The book emphasizes understanding cash flow patterns to distinguish between assets and liabilities effectively.

What is the "Rich Dad" philosophy on financial education?

- Self-Education: Rich Dad advocates for self-education in financial matters, beyond what traditional schools teach.

- Practical Experience: Encourages learning through real-world experiences, such as investing and entrepreneurship.

- Continuous Learning: Stresses the importance of lifelong learning and adapting to financial changes and opportunities.

- Financial IQ: Developing a high financial IQ is crucial for making informed investment decisions and achieving financial success.

How does "Rich Dad Poor Dad" suggest overcoming the fear of losing money?

- Embrace Failure: The book suggests viewing failure as a learning opportunity rather than something to fear.

- Risk Management: Encourages understanding and managing risks rather than avoiding them entirely.

- Start Small: Begin with small investments to build confidence and experience without significant financial risk.

- Mindset Shift: Changing your mindset about money and risk can help overcome the fear of losing money.

What is the significance of "mind your own business" in "Rich Dad Poor Dad"?

- Focus on Assets: The phrase means focusing on building and managing your own assets rather than solely working for a paycheck.

- Entrepreneurial Spirit: Encourages readers to think like entrepreneurs, even if they are employees, by creating additional income streams.

- Financial Independence: By minding your own business, you work towards financial independence and security.

- Long-Term Vision: It involves having a long-term vision for wealth creation and not just short-term financial gains.

How does "Rich Dad Poor Dad" address the concept of taxes and corporations?

- Tax Advantages: The book explains how the rich use corporations to minimize taxes legally.

- Corporate Structure: Corporations can pay for expenses with pre-tax dollars, offering significant tax benefits.

- Financial Education: Understanding tax laws and corporate structures is part of financial education and wealth building.

- Wealth Protection: Corporations also provide a layer of protection for personal assets against liabilities.

What role does financial intelligence play in "Rich Dad Poor Dad"?

- Problem Solving: Financial intelligence is crucial for solving financial problems and making informed decisions.

- Investment Strategies: It involves understanding investment strategies and market dynamics to grow wealth.

- Continuous Improvement: Encourages continuous improvement and learning to enhance financial intelligence.

- Wealth Creation: A high level of financial intelligence is necessary for creating and sustaining wealth over time.

How does "Rich Dad Poor Dad" suggest using money to work for you?

- Investments: Invest in assets that generate passive income, such as real estate, stocks, and businesses.

- Reinvest Earnings: Reinvest earnings from assets to grow your wealth exponentially.

- Financial Literacy: Use financial literacy to identify and capitalize on investment opportunities.

- Long-Term Focus: Focus on long-term wealth creation rather than short-term financial gains.

What are the practical steps to start building wealth according to "Rich Dad Poor Dad"?

- Financial Education: Invest in your financial education through books, seminars, and courses.

- Start Small: Begin with small investments to gain experience and confidence.

- Build Assets: Focus on acquiring assets that generate passive income.

- Network: Surround yourself with financially savvy individuals and learn from their experiences.

Rich Dad Series

About the Author

Other books by Robert T. Kiyosaki

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.