Key Takeaways

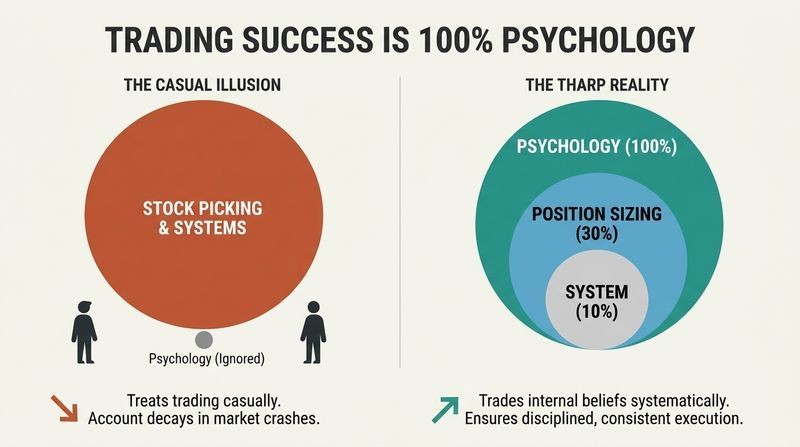

Trading success is 100% psychology, not stock picking

You trade your beliefs, not the market. Tharp, an NLP modeler who studied elite traders like Ed Seykota and Tom Basso, originally split trading into three parts: psychology (60%), position sizing (30%), and system development (10%). He later revised this: psychology accounts for everything, because beliefs, mental states, and mental strategies drive every task.

The average investor is doomed by treating investing casually. He tells the story of Joe, a smart engineer who spent eight years mastering his profession but read four books and watched CNBC before betting his $623,000 nest egg. Joe rode the 2008 crash down nearly 60% from his 2000 peak. You would not perform brain surgery off the street, yet people treat markets that way and their accounts die.

What's striking is how Tharp inverts the entire retail-investor mindset. Most people obsess over which stock to buy; he says that is the least important 10%. This aligns with behavioral finance research from Kahneman and Tversky showing humans are systematically irrational decision-makers. Tharp's twist is prescriptive rather than descriptive: instead of predicting how irrational markets behave, fix your own irrationality. One caution: claiming psychology is literally 100% risks being unfalsifiable, since it folds system and sizing into psychology by definition. Still, the core corrective is sound. Expertise in one domain (engineering, medicine) breeds dangerous overconfidence in another, a well-documented cognitive bias.

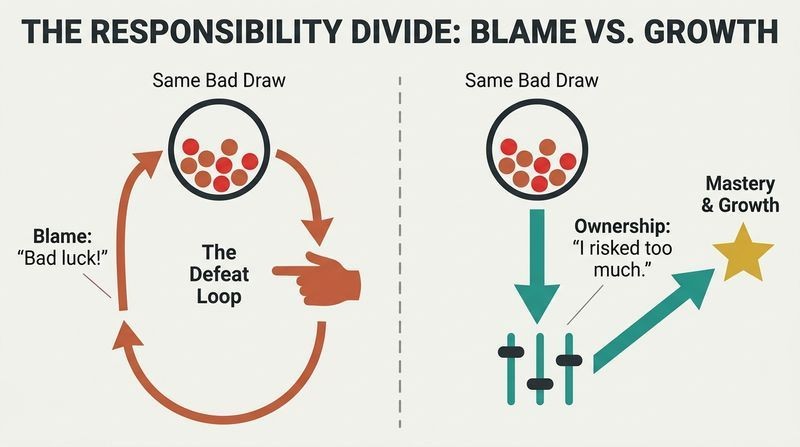

Take total responsibility, or repeat the same losses forever

Blame is the enemy of improvement. In Tharp's marble game, participants draw marbles from a bag representing a trading system, and everyone gets identical draws. When someone hits a losing streak, players who went bankrupt often blame the person who pulled the losing marbles. But every game is designed to contain a long losing streak. Blaming external causes guarantees you repeat the mistake.

Only one answer helps you grow. When asked why they lost, players offer excuses: bad luck, a stupid game, a bad system. The single useful response is: "I risked too much on some trades." That is the only answer you can act on. Tharp insists you produce your own results, so when you dislike them, you hunt for your own mistakes rather than a better guru.

This echoes Stoic philosophy, particularly Epictetus, who distinguished between what is in our control and what is not, and located all genuine agency in our own judgments. Tharp's marble game is a clever experimental demonstration of attribution bias: humans credit skill for wins and blame luck for losses. The deeper point connects to locus of control research in psychology, where an internal locus correlates with better outcomes across domains. The risk is over-attribution: sometimes markets genuinely are random, and punishing yourself for a statistically inevitable drawdown can breed paralysis rather than learning. Responsibility should mean ownership, not self-flagellation.

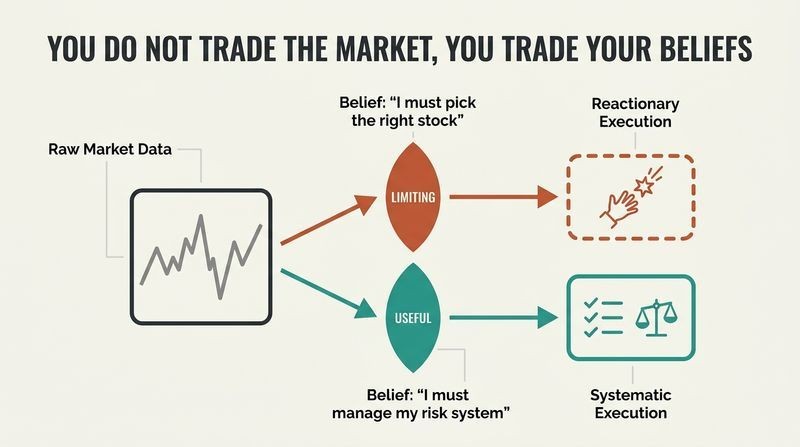

You do not trade markets, you trade your beliefs

Every belief is self-confirming and useful or limiting. Tharp argues the market itself is inaccessible; you only ever act on your beliefs about it. He runs the Belief Examination Paradigm: for each belief ask who gave it to you, what it gets you into, what it gets you out of, how it limits you, whether it is useful, and whether an emotional charge holds it in place.

Test beliefs by usefulness, not truth. Take "good performance comes from picking the right stock." It sends you hunting for tips and reading stock-picking books while it gets you out of personal responsibility, exits, position sizing, and planning. A core NLP presupposition drives this: if something does not work, do something else. He asks traders to write down 100 personal beliefs and 200 market beliefs, then audit each one.

The constructivist framing here has real philosophical weight. It resembles pragmatism (William James, John Dewey), which judges ideas by their practical consequences rather than correspondence to some fixed reality. It also anticipates cognitive behavioral therapy, which treats maladaptive beliefs as revisable rather than true. The strength is empowerment; the danger is relativism. Markets do contain objective facts (prices, volatility, liquidity), and treating all beliefs as merely useful fictions can slide into wishful thinking. Tharp partly guards against this by demanding beliefs be tested against results. The most defensible reading: beliefs are the lens, and you can grind a better lens.

Exits make money; entries barely matter at all

A coin-flip entry can still profit. Tharp and Tom Basso tested a system that entered ten commodities randomly (long or short by coin flip), risked 1% per position, and exited at three times the 20-day average true range. Despite paying $100 per trade in costs and surrendering any entry edge, it made money consistently over ten years. The reason: wide trailing stops kept it in strong trends and cut losing trends fast.

The golden rule is cut losses, let profits run. Your initial stop defines 1R, your baseline risk. A tight stop (small 1R) produces frequent small losses but occasional huge R-multiple wins. Buy a $50 stock with a $1 stop; if it climbs $10, that is a 10R gain even after three prior 1R losses. Entries feed the myth of stock selection that mutual funds perpetuate.

This is Tharp's most counterintuitive and empirically grounded claim. The random-entry experiment is a genuine falsification test of the stock-picking obsession, and trend-following funds (Dunn, Winton, Man AHL) have built decades of returns on asymmetric exits rather than clever entries. The math is convexity: capping downside at 1R while letting winners run creates a positively skewed distribution, the same logic Nassim Taleb describes in his barbell strategy. One nuance: random entry only works with sufficient trend persistence and enough capital to survive drawdowns and costs. In choppy, mean-reverting, or high-friction markets, sloppy entries can bleed an account dry. Exits dominate, but entries are not literally irrelevant.

Position sizing drives 90% of your performance variability

Same trades, wildly different outcomes. In Tharp's marble game, 100 people receive identical trades starting with $100,000. At the end there are typically as many different ending equities as there are players. A third go bankrupt, a third lose money, a third profit hugely. The only variables are how much each risked per trade and the psychology behind that decision.

Academia calls it asset allocation and misses the point. A 1991 study of 82 portfolio managers found 91% of performance variability came from asset allocation, which the researchers defined as how much was held in stocks, bonds, and cash. Tharp argues "how much" is the real secret, yet books on asset allocation never define or explain it. His CPR formula makes it concrete: Position size equals Cash to risk divided by Risk per unit.

Tharp deserves credit for popularizing position sizing as a distinct discipline, separate from entry rules, at a time when retail education ignored it. The marble game is a vivid Monte Carlo demonstration that dispersion of outcomes is driven by bet sizing, a point formalized in the Kelly criterion (John Kelly, 1956) and used by professional gamblers and quants alike. The claim that sizing is 90% of variability may overstate a figure borrowed loosely from the Brinson study, which measured something narrower. But directionally he is right: over-betting causes ruin faster than bad entries, and the gap between theoretical edge and realized returns usually lives in sizing.

Judge your system by expectancy divided by variability

Expectancy tells you what you earn per dollar risked. Tharp describes systems as distributions of R-multiples, where R is your initial risk. A system with 20% winners can still thrive: if winners average 10R and losers average around 1R, expectancy might be 0.8R, meaning you net 0.8R per trade on average. Over 100 trades that is 80R.

Quality equals consistency, not accuracy. He divides mean R by the standard deviation of R to gauge how easily a system meets objectives. A ratio of 0.16 to 0.19 is poor but tradable; 0.25 to 0.29 is good; 0.70 or better he calls Holy Grail. Crucially, opportunity matters: a 0.5-ratio system trading 20 times monthly beats a 0.75 system trading once yearly. His System Quality Number folds in trade frequency.

Reframing reliability (win rate) as nearly irrelevant is Tharp's sharpest corrective to the human need to be right. Schoolteachers trained us that 70% is a passing grade, so traders chase high hit rates and end up with tiny stops and catastrophic tails. His expectancy-to-deviation ratio is essentially a Sharpe-ratio cousin applied to trade-level results rather than returns. The framing is pedagogically superior to raw Sharpe because it keeps risk in units the trader actually sets. One caveat: R-multiple samples are notoriously unstable, and a handful of outlier winners can dominate the mean, making backtested "Holy Grail" ratios fragile out of sample.

Build different systems for six distinct market types

Most traders fail chasing one system for all conditions. Tharp classifies markets along two axes: direction (up, down, sideways) and volatility (quiet, volatile), producing six types. He measures direction using rolling 13-week windows, calling anything under a 5.53% absolute move sideways. He measures volatility with average true range as a percentage of close, with 2.87% as the dividing line.

Match the tool to the weather. Buying and holding tech stocks worked in 1999 and cratered in 2000 to 2002. Buying inverse index funds when the market flashed bearish in 2007 worked wonders in 2008. The two waiters who bragged about their trading in 1999 almost certainly did not survive. Developing a strong strategy for one market type is easy; the fatal mistake is forcing a single strategy to work everywhere. When your type has no fitting system, go to cash.

This regime-based thinking prefigures what quantitative finance now calls regime-switching models, and it maps neatly onto the observation that strategy performance is conditional, not universal. The value is humility: rather than seeking one holy formula, Tharp advocates a toolkit plus a diagnostic for which tool to deploy. The weakness is regime-identification lag. His 13-week and 40-week signals are backward-looking by construction, so you always recognize a new regime after it has begun, sometimes after significant damage. Whipsaws in transitional markets are the Achilles heel. Still, the discipline of asking "what kind of market is this and does my system fit it?" is more than most retail traders ever do.

Define a mistake as breaking your own rules

No rules means everything you do is a mistake. Tharp defines a mistake precisely: not following your written trading rules. This is why a business plan matters, because it generates the rules against which mistakes are measured. Repeating the same mistake is self-sabotage.

Mistakes are quantifiable and expensive. He asks coached traders to track mistakes in R. One futures trader running $200 million made 11 mistakes in nine months, costing 46.5R, roughly halving his potential profit. A long-term ETF trader with wide stops made 27 mistakes costing only 8.2R, about 20% of profits. Leveraged traders lose roughly 4R per mistake; long-term investors about 0.4R. The fix is two daily rituals: morning mental rehearsal ("what could go wrong today?") and an end-of-day debrief ("did I make any mistakes?"). Improving from 90% to 98% efficiency can double returns.

Operationalizing "mistake" as rule-violation is a genuinely useful move, because it converts a vague sense of regret into a measurable, coachable metric. This resembles the aviation and surgical checklist movement documented by Atul Gawande, where catastrophic errors dropped once professionals followed pre-committed procedures rather than improvising under pressure. Tharp's mental rehearsal also has support in sports psychology, where visualization measurably improves performance. The subtle risk: labeling every rule-break a mistake assumes your rules are correct. Sometimes discretion that violates a rule is actually adaptive learning, not error. Distinguishing a disciplined deviation from an emotional one requires exactly the self-knowledge he champions elsewhere.

Treat trading like a business with a written plan

Only about 5% of traders have a written plan. Tharp ranks a business plan among his top requirements. It is not for raising money; it is a living document guiding your career. It should cover your mission statement, goals, market beliefs, the big picture, tactical strategies, position sizing, psychological challenges, daily procedures, an education plan, and a worst-case contingency plan.

Plan for disaster before it arrives. Under stress, adrenaline diverts blood from the brain to muscles, shrinking your conscious capacity from about seven chunks of information. So you must rehearse in advance. He cites a world-class cyclist who sat in a field imagining every possible crash and rehearsing responses; months later, spotting a tire about to blow at high speed, he flipped over the handlebars automatically and saved his life. Brainstorm 100 things that could go wrong, then rehearse three solutions each.

The business-plan framing borrows sensibly from entrepreneurship, where the discipline of writing forces implicit assumptions into the open. The neuroscience Tharp invokes is broadly accurate: acute stress impairs prefrontal working memory, which is why pilots, soldiers, and surgeons drill procedures until they are automatic. His worst-case rehearsal is essentially the premortem technique that psychologist Gary Klein advocates, imagining failure in advance to surface hidden risks. The 300-solutions prescription is heavy and few will complete it, but even partial preparation beats none. The deeper insight is that consistency under pressure comes from prior rehearsal, not in-the-moment willpower, which reliably collapses when adrenaline hits.

Simplicity beats the perfectionism-complexity trap

Complexity is a form of avoidance. Tharp names the perfectionism-complexity complex: the belief that your system is never quite good enough, that there is always one more exit or entry to test. This keeps you tinkering endlessly and never actually trading. Your conscious mind holds only about seven chunks of information, so over-engineering exceeds your capacity and invites failure.

Purity of spirit beats sophistication. He praises a trader whose entire method was to buy what is going up, exit immediately if it turns against him, and let winners run. Tharp cites a retired engineer he coached who watched markets with a clear mind, bought strength, sold weakness, and grew his account into a substantial hedge fund over 18 years using simple principles. A broker who scored in the bottom 1% of his test was drowning in chaos; the prescription was one long-term system checked once daily after the close.

The cognitive-load argument rests on George Miller's famous 1956 finding that working memory holds roughly seven items, and Tharp applies it shrewdly: complexity that exceeds capacity degrades decisions, especially under stress. This connects to modern research on choice overload and decision fatigue. There is also a robustness argument he undersells: simple rules with few parameters overfit less and generalize better out of sample, a point quants make about curve-fitting. The counterpoint is that some genuinely profitable strategies (statistical arbitrage, options market-making) are irreducibly complex. Tharp's simplicity gospel fits discretionary and trend traders better than quantitative ones. For most retail traders, though, the tinkering he warns against is pure procrastination dressed as diligence.

Analysis

Super Trader is a distillation of Van K. Tharp's coaching program, structured as five sequential steps: work on yourself, build a business plan, develop market-type-specific systems, master position sizing, and minimize mistakes. Its genre is hybrid: part trading manual, part self-help, part behavioral psychology. What makes it hard to summarize is its anthology structure, dozens of short standalone essays rather than a single argument, and its unusual fusion of technical rigor (R-multiples, expectancy, system quality) with spiritual and NLP-derived exercises (God Boxes, inner interpreters, mindfulness) that many finance readers find jarring.

The book's enduring contribution is conceptual reordering. Tharp took the retail obsession with stock picking and inverted the hierarchy: entries barely matter, exits and position sizing dominate, and psychology governs everything. His marble game and random-entry experiment are pedagogically brilliant demonstrations of ideas that quantitative finance independently formalized through the Kelly criterion, convexity, and regime-switching models. R-multiple thinking, expressing every outcome as a multiple of initial risk, is a genuinely clarifying lens that deserves its wide adoption among systematic traders.

The weaknesses are equally clear. The book was written in late 2008 amid apocalyptic conviction that the United States was bankrupt and facing a decade-long bear market, a forecast the subsequent bull market decisively contradicted, which is ironic given Tharp's own insistence on not predicting. The spiritual material, Bible quotes, channeled texts, laughter therapy, will alienate empirically minded readers, and claims like "psychology is 100% of success" are unfalsifiable by construction. Backtested Holy Grail ratios are fragile out of sample, and regime signals lag.

Yet the core discipline survives these flaws. Tharp's central message, that consistent profit comes from self-knowledge, pre-committed rules, ruthless loss-cutting, and mathematically sound bet sizing rather than prediction, remains among the most useful frameworks available to independent traders. It is less a system than an operating philosophy for treating trading as a serious profession.

Review Summary

Super Trader is highly regarded by readers for its focus on trading psychology, position sizing, and developing a personalized trading system. Many consider it essential reading for traders at all levels. The book emphasizes self-awareness, treating trading as a business, and managing risk effectively. Readers appreciate Tharp's no-nonsense approach and practical advice. Some find the position sizing chapter confusing, but overall, the book is praised for its comprehensive coverage of trading psychology and risk management. Many readers report significant improvements in their trading after applying Tharp's principles.

People Also Read

Glossary

R-Multiple

Profit or loss versus initial riskA way of expressing every trade result as a multiple of the initial risk taken, where R equals the difference between entry price and stop-loss. If you risk $10 per share and gain $100, that is a 10R profit; a $15 loss is a 1.5R loss. Any system can be described by the distribution of R-multiples it produces.

Expectancy

Average R earned per tradeThe mean R-multiple of a trading system, telling you how much you can expect to make per dollar risked over many trades. A system with 0.8R expectancy nets about 0.8R per trade on average, or roughly 80R over 100 trades, even if it wins only 20% of the time.

Position Sizing

How much to risk per tradeThe element of a trading system that determines how large a position to take, and thus how you meet your objectives. Tharp argues it drives roughly 90% of performance variability. His CPR formula sets position size (P) equal to cash you will risk (C) divided by risk per unit (R).

System Quality Number (SQN)

System rating including trade frequencyTharp's proprietary measure of trading system quality that combines the ratio of expectancy to the standard deviation of R with the number of trades generated. Higher SQN means more freedom to size positions aggressively and easier achievement of objectives. It addresses the flaw that a high-ratio system with few opportunities is not actually valuable.

Holy Grail System

System with superb consistency ratioTharp's label for a system whose expectancy-to-standard-deviation ratio reaches 0.70 or better, or that generates such a ratio within a single market type with high trade frequency. Not a mythical perfect system but one so consistent it allows very aggressive position sizing. The true Holy Grail, he argues, is internal self-mastery.

Belief Examination Paradigm

Six questions to audit beliefsTharp's process for auditing a belief by asking six questions: who gave it to you, what it gets you into, what it gets you out of, how it limits you, whether it is useful, and whether an emotional charge holds it in place. Beliefs are judged by usefulness rather than truth.

Market Type

Six market condition categoriesTharp's classification of markets along two axes, direction (up, down, sideways) and volatility (quiet, volatile), yielding six types. He measures direction with rolling 13-week windows (under 5.53% absolute move is sideways) and volatility with average true range as a percentage of close (above 2.87% is volatile). Strategies should be built per market type.

1R (Initial Risk)

Baseline loss if stopped outThe initial risk in a trade, defined by the distance between your entry price and your protective stop-loss, multiplied by position size. It is the unit against which all profits and losses are measured as R-multiples. Knowing 1R before entering forces discipline and enables reward-to-risk evaluation.

The Four Quadrants

Four trader cash-flow typesAdapted from Kiyosaki's Cashflow Quadrant: employee traders work for a system they do not understand (bank and fund traders), self-employed traders are the system (perfectionist discretionary traders), business-owner traders build automated systems others run, and investor traders invest in systems. The right side (owner, investor) has money working for them and tends to succeed.

FAQ

What's Super Trader about?

- Focus on Trading Success: Super Trader by Van K. Tharp is a guide to achieving consistent profits in various market conditions, emphasizing personal psychology, business planning, and systematic trading.

- Five-Step Approach: The book outlines a five-step process for traders, including personal development, business planning, strategy creation, position sizing, and mistake minimization.

- Mindset and Self-Improvement: It stresses that successful trading is as much about mindset and self-awareness as technical skills and market knowledge.

Why should I read Super Trader?

- Transformative Insights: The book offers insights into the psychological aspects of trading, often overlooked by traders, with practical exercises to improve mental state and discipline.

- Structured Learning: It provides a structured approach for developing a personalized trading plan, applicable to both novice and experienced traders.

- Long-Term Success: By focusing on self-improvement and a solid business plan, readers can achieve long-term success rather than short-term gains.

What are the key takeaways of Super Trader?

- Self-Work is Essential: Working on oneself is critical for successful trading, with an emphasis on identifying and overcoming limiting beliefs.

- Develop a Business Plan: A well-defined business plan guides trading decisions and strategies, including mission statements, goals, and tactical strategies.

- Position Sizing Matters: Effective position sizing is vital for managing risk and achieving trading objectives, with the CPR model introduced for alignment with goals.

What is the five-step approach outlined in Super Trader?

- Work on Yourself: Address personal issues affecting trading performance, including self-appraisal and identifying limiting beliefs.

- Develop a Business Plan: Create a comprehensive plan outlining trading goals, strategies, and risk management techniques.

- Create Effective Strategies: Develop strategies that align with market conditions and personal objectives, adapting to different market types.

- Understand Position Sizing: Emphasize position sizing for managing risk and achieving goals, with models to determine appropriate sizes.

- Minimize Mistakes: Monitor performance and minimize mistakes through discipline and adherence to trading rules.

How does Super Trader address the psychological aspects of trading?

- Beliefs Shape Reality: Traders must examine their beliefs about themselves and the market, as these influence behavior and outcomes.

- Self-Responsibility: Encourages taking full responsibility for results, promoting learning from mistakes rather than blaming external factors.

- Mindfulness Practices: Introduces mindfulness techniques to help traders stay present and focused, reducing emotional reactions.

What is the importance of a mission statement in trading according to Super Trader?

- Guides Decision-Making: A mission statement serves as a guiding principle, helping evaluate opportunities against core objectives.

- Clarifies Goals: It clarifies goals and motivations, ensuring actions align with long-term vision for success.

- Enhances Focus: A clear mission helps maintain focus and avoid distractions that do not contribute to the overall strategy.

What is the CPR model for position sizing mentioned in Super Trader?

- Risk Management Framework: The CPR model stands for Capital, Position, and Risk, providing a structured approach to risk on each trade.

- Aligns with Objectives: Helps align position sizes with trading objectives, managing risk effectively while pursuing profits.

- Dynamic Adjustments: Allows for dynamic adjustments based on market conditions and performance, promoting flexibility.

What is the Belief Examination Paradigm in Super Trader?

- Assess Your Beliefs: A tool to identify and evaluate beliefs about trading, considering their origins and influence on behavior.

- Identify Limitations: Uncovers limiting beliefs that may hinder performance, prompting questions about their usefulness.

- Transform Limiting Beliefs: Aims to transform limiting beliefs into empowering ones, essential for a mindset conducive to success.

What are some common mistakes traders make according to Super Trader?

- Ignoring Trading Rules: Not following established rules can lead to emotional decision-making and losses.

- Risking Too Much: Failing to manage risk by risking too much capital on a single trade can lead to significant drawdowns.

- Emotional Exits: Exiting trades based on emotions rather than criteria can minimize profits and maximize losses.

How can I apply the concepts from Super Trader to improve my trading?

- Self-Assessment: Conduct an honest self-appraisal to identify personal beliefs and psychological barriers affecting trading.

- Create a Business Plan: Develop a comprehensive plan outlining goals, strategies, and risk management, aligning with your mission.

- Practice Mindfulness: Incorporate mindfulness practices to enhance focus and reduce emotional reactions for rational decision-making.

What are some effective daily procedures suggested in Super Trader?

- Daily Mental Rehearsal: Start each day with a mental rehearsal to anticipate challenges and plan responses.

- Debriefing: Conduct a debriefing session at the end of each day to assess performance and identify mistakes.

- Tracking R-Multiples: Keep track of R-multiples to evaluate performance over time, allowing for informed strategy adjustments.

What are the best quotes from Super Trader and what do they mean?

- "You create your own results.": Emphasizes personal responsibility in trading, suggesting ownership of decisions and outcomes.

- "You cannot trade the market; you can only trade your beliefs about the market.": Highlights the psychological aspect, emphasizing mindset and beliefs' influence on success.

- "Enjoy your obstacles.": Encourages embracing challenges as growth opportunities, leading to better decision-making and resilience.

About the Author

Other books by Van K. Tharp

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.