Key Takeaways

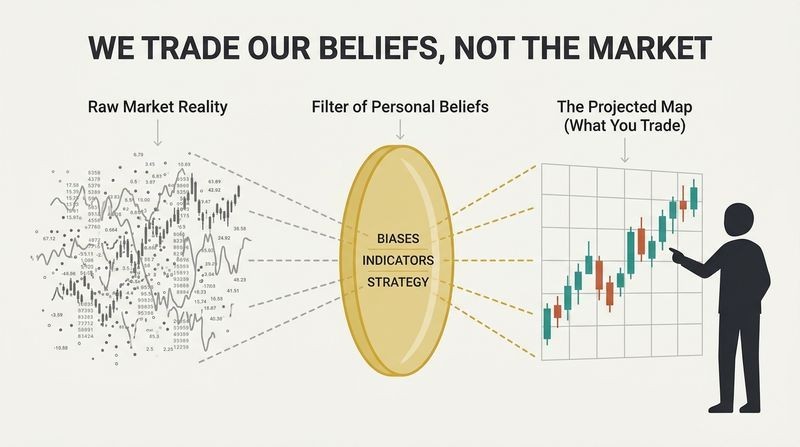

You never trade the market itself, only your beliefs about it

Van Tharp's central thesis dismantles the fantasy of a magic system. The "Holy Grail" traders chase is not a secret formula for predicting prices, it is an inner state of self-knowledge. After modeling roughly 50 top traders, Tharp found none used the same method, yet all succeeded. Why? Because each traded a system that fit their own beliefs, temperament, and objectives.

A daily bar chart is not the market. Your favorite indicator is not the market. Both are filters, distortions of raw data that you accept as reality. Since your beliefs are the only thing you can actually act on, the work of trading begins with excavating them. Tharp asks clients to write down at least 100 beliefs about themselves and 100 about markets before designing anything.

This reframing echoes constructivist psychology and Kahneman's later work on cognitive framing: humans never perceive raw reality, only mental models of it. Tharp's insight predates behavioral finance going mainstream, and it aligns with George Soros's reflexivity, the idea that participants' biased perceptions shape the market they observe. The practical power here is diagnostic. When a trader cannot follow a supposedly good system, the culprit is usually a belief conflict, not a flawed method. One limitation: knowing your beliefs does not automatically make them profitable. Tharp assumes self-awareness plus a positive expectancy edge, but markets can punish even well-examined convictions when structural regimes shift.

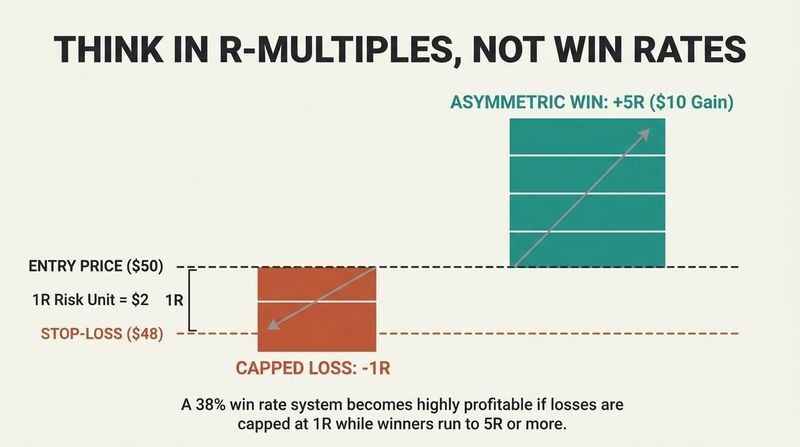

Judge every trade by its R-multiple, not whether it won

R is your initial risk, the distance between entry and your predetermined exit. Buy a stock at $50 with a stop at $48, and R equals $2. Every outcome becomes a multiple of that risk. A $10 gain is a 5R win, a $6 loss is a 3R loss. Tharp's rule: keep losses to 1R or less, and hunt for winners that are large R multiples.

This single mental shift transforms trading. A system that wins only 38% of the time can be wildly profitable if winners average 12R and losers average 0.5R. Any trading system, Tharp argues, is simply a distribution of R-multiples. Characterize it by its mean (expectancy), its spread, and how often it trades. Once you think in R, you stop obsessing over being right.

Expressing outcomes as risk multiples is quietly revolutionary because it normalizes across instruments and account sizes, making a corn trade and a stock trade directly comparable. It resembles how poker players think in terms of expected value per bet rather than individual hands. The framework also inoculates against the disposition effect, the documented tendency to sell winners too early and hold losers too long. One subtlety Tharp handles well: real losses can exceed 1R when markets gap through stops, so R is a target, not a guarantee. The concept's elegance is that it converts a chaotic activity into a measurable probability distribution you can actually study.

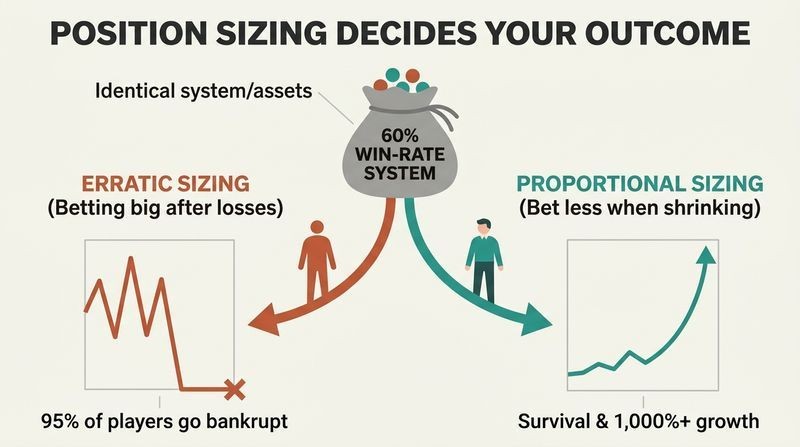

Position sizing, not stock picking, decides whether you meet your goals

Tharp coined the term "position sizing" to replace the muddled phrase "money management." It answers one question: how much? Brinson's study of 82 pension plans found that allocation decisions, not security selection, drove 91.5% of performance variability.

Tharp's marble game proves it. Players draw from a bag with a positive expectancy (it wins 80% of the time over many draws despite losing on individual pulls). Everyone gets identical draws, yet outcomes range from bankruptcy to 1,000% gains. The only variables are bet size and psychology. In Ralph Vince's experiment, 40 PhDs played a 60%-win game; only 2 made money because they bet erratically after losses. Anti-martingale sizing (betting more as equity grows, less as it shrinks) is the only approach that survives.

This is the book's most underappreciated contribution, and it maps onto the Kelly Criterion from information theory, which mathematically defines optimal bet size to maximize long-run growth without ruin. The counterintuitive punch is that brilliant people fail a positive-expectancy game purely through sizing errors, driven by the gambler's fallacy. Tharp's critique of Wall Street training is sharp: brokers, CFPs, MBAs, and CFAs receive essentially zero instruction on sizing. One gap worth noting: mutual fund managers are structurally barred from aggressive sizing by their charters, so the lesson applies far more to independent traders than to the institutions that dominate markets.

Your brain deletes the most useful market data through mental shortcuts

Information doubles roughly every year, yet the conscious mind processes only 5 to 9 chunks at a time. To cope, humans generalize, delete, and distort, using "judgmental heuristics" that quietly sabotage trading. Tharp catalogs the worst offenders:

1. Lotto bias: obsessing over entry because it feels like controlling the market

2. Representativeness bias: mistaking a bar chart or indicator for the market itself

3. Conservatism bias: ignoring evidence that contradicts a cherished pattern

4. Law of small numbers: seeing a reliable pattern in a handful of examples

5. Gambler's fallacy: expecting a reversal after a streak

William Eckhardt captured it: the eye fixates on a method's stunning successes and glosses over the grinding daily losses, leaving researchers convinced a system is far better than it is.

Tharp was applying cognitive-bias research to trading in the late 1990s, before Kahneman and Tversky's work saturated finance culture. The lotto bias deserves particular attention because it explains why the industry sells entry signals: people crave the illusion of control at the exact moment (entry) when they briefly have it, then lose all control once positioned. This connects to locus-of-control research in psychology, where perceived control reduces anxiety even when it changes nothing. The deeper implication, which Tharp presses, is that the trading media profitably feeds these biases rather than correcting them, because giving people what they want outsells giving them what they need.

Master your exits; entry barely beats a coin flip

Tharp and Market Wizard Tom Basso tested a genuinely random entry, a coin flip deciding long or short, paired with a trailing stop of three times volatility and a 1% risk sizing rule. It made money on 100% of runs across ten markets over a decade. The system's reliability was just 38%, typical for trend following.

The golden rule (cut losses short, let profits run) is entirely about exits. Chuck LeBeau hammered this: cutting losses is an exit, letting profits run is an exit. Yet 95% of aspiring system designers pour their energy into finding the perfect entry. LeBeau and Lucas tested common entry indicators (oscillators, moving-average crossovers) and found almost none beat random entry over 20 days.

The random-entry result is one of the most quietly subversive experiments in trading literature, because it demolishes the entire cottage industry of entry-signal newsletters and pattern-recognition software. It parallels findings in other domains where timing matters less than exposure management, such as portfolio rebalancing beating market timing. The caveat: random entry only works when yoked to disciplined exits and sizing, so it is not license for carelessness. There is also survivorship nuance. The test assumed the trader stays mechanically committed through drawdowns, which most humans psychologically cannot do. The lesson is not that entry is worthless but that its marginal value is dwarfed by exits and sizing.

Spend half your system-building time defining what you actually want

A CTA-funder told Tharp the single best advice for system developers: devote at least 50% of your time to working out objectives. Most people spend minutes, then grumble that objectives have nothing to do with trading. They are wrong. You cannot build a system without knowing its destination.

Tharp illustrates with "Sam," who wanted to make 150% in three months (a near-1,000% annualized return) while risking only 10%. That demands a 15-to-1 reward-to-risk ratio, which no method reliably delivers; 3-to-1 is considered excellent. Model trader Tom Basso, by contrast, could specify everything: expected annual return of 20 to 40%, maximum tolerable drawdown of 25%, time available per day, psychological strengths, and how he would react to ten consecutive losses.

Objective-setting is the trading equivalent of Stephen Covey's begin-with-the-end-in-mind, but Tharp gives it teeth by tying it to mathematical feasibility. The Sam anecdote exposes a universal cognitive error: people specify desired returns while ignoring the drawdown and reward-to-risk ratios those returns mathematically require. This is the same disconnect behavioral economists find in retirement planning, where savers want high returns but reject the volatility that generates them. Basso's precision (knowing his own tension registers first in his fingers) shows objectives extend into self-knowledge, not just numbers. The weakness is that beginners lack the experience to set realistic objectives, creating a chicken-and-egg problem the book only partly resolves.

Any positive-expectancy concept works if it genuinely fits you

Tharp surveys a menu of trading concepts, insisting none is superior, each simply suits different temperaments. Trend following captures long moves and never misses a major one, but markets trend only 15 to 30% of the time. Band trading buys the bottom and sells the top of a range, thriving in the 70 to 85% of sideways markets. Value trading buys assets at deep discounts to liquidation value, like companies holding Hawaiian land on their books at $150 an acre.

Other concepts include arbitrage (exploiting temporary loopholes), spreading (trading relationships between instruments), seasonal tendencies, fundamental analysis, and intermarket analysis. Even "there's an order to the universe" methods (Elliott Wave, Gann, Fibonacci) can be traded profitably, because if enough believers act on them, they become self-fulfilling.

Tharp's radical agnosticism about method is both liberating and slippery. It rests on a defensible claim: expectancy and sizing, not the concept, determine profitability. This echoes the finding that diverse hedge fund strategies can all succeed if risk-managed. Yet his tolerance for astrology-based and sunspot-correlated methods invites skepticism. His own honest data undercuts them; the March 1989 solar flare, the largest of the century, had no discernible market effect. The self-fulfilling-prophecy defense of Fibonacci levels is intellectually serious, resembling Keynesian beauty-contest dynamics where traders anticipate what others anticipate. Still, the book would be stronger distinguishing concepts with genuine structural edges from those surviving purely on collective belief.

Trade the big picture: secular bear markets can erase 18 years of gains

Tharp urges every trader to become a "mental scenario trader," tracking macro forces monthly. Writing in 2006, he flagged six: crushing U.S. debt, a secular bear market begun in 2000, globalization lifting China and India, mutual-fund fragility, shifting tax rules, and humanity's tendency to play a losing money game.

The secular-cycle insight is the sharpest. Drawing on Michael Alexander and Ed Easterling, Tharp notes markets swing between multi-decade bull and bear valuation cycles. Primary bull markets averaged 13.2% annual returns; primary bear markets averaged just 0.3% real return over roughly 18 years. Crucially, these cycles forecast valuations (P/E ratios), not prices. Easterling's engine: when inflation is low and stable, markets support P/E ratios above 20; when inflation rises or deflation appears, ratios collapse into single digits.

The valuation-cycle framework has aged reasonably well and aligns with Robert Shiller's cyclically adjusted P/E research, which shows starting valuations powerfully predict decade-forward returns. Tharp's decoupling of the economy from the stock market is empirically sound and counterintuitive: from 1966 to 1981 GDP grew 9.6% annually while stocks languished. Some predictions were less prescient; the forecast of runaway dollar collapse and inflation did not unfold as sketched, and the mutual-fund redemption crisis from retiring boomers was muted. The enduring lesson is methodological rather than predictive: build systems aware of the regime you inhabit, and hold beliefs loosely enough to update them with monthly data.

Opportunity times expectancy beats a high expectancy alone

Tharp calls this "expectunity," expectancy multiplied by how often you trade. A system with a dazzling 2.58R expectancy that trades once a month may lose to a modest 0.4R day-trading system that fires five times daily. Consider his four archetypes: the long-term trend follower, the standard trend follower, the high-probability short-term trader, and the market maker who captures the bid-ask spread on 80% of trades with just 0.15R expectancy.

Run the math including opportunity, and the market maker's total daily R dwarfs the others. At 0.25% risk per trade, he could theoretically make 13% daily versus the trend follower's 0.03%. This is why floor traders with tiny edges but enormous trade frequency can outperform patient position traders with beautiful expectancies.

Expectunity is essentially throughput thinking applied to trading, the same principle behind Eliyahu Goldratt's theory of constraints in manufacturing: a small margin repeated at high velocity beats a large margin achieved rarely. It also explains the rise of high-frequency trading firms that profit from vanishingly thin edges captured millions of times. The crucial hidden cost Tharp flags is psychological and transactional: high-frequency approaches multiply commissions, slippage, and the chances of a costly mental error. A single mistake costing 2R, made weekly, can wipe out an entire year of a good system's profits. Velocity amplifies both edge and error, which is why frequency demands near-perfect discipline.

Deploy multiple exit types simultaneously, keeping each one simple

Exits fall into four families: those that cut a loss while reducing initial risk (timed stops, trailing stops), those that maximize profit (volatility trailing stops, moving-average stops), those that protect accumulated gains (profit objectives, percent-retracement stops), and psychological exits.

The percent-retracement stop shines. The Oxford Club imposed a 25% trailing stop on all recommendations and produced a 2.5R expectancy. The math explains why 25% beats 50%: recover from a 24% drawdown requires a 33% gain, but a 49% drawdown demands nearly 100% just to break even. Tharp warns against one seductive but destructive practice: scaling out of positions (selling portions as price rises). It guarantees you hold full size during your worst losses and minimal size during your biggest wins, the exact inverse of the golden rule.

The asymmetry of drawdown recovery is arithmetic that traders ignore at their peril, and it generalizes far beyond markets into any compounding system, including reputation and health. Tharp's attack on scaling out is provocative and correct in pure expectancy terms, yet it collides with practitioner psychology: banking partial profits reduces the emotional volatility that causes abandonment of good systems. There is a genuine tension between mathematical optimality and behavioral sustainability. The psychological-exit category (stepping away during divorce, illness, or exhaustion) is underrated wisdom rarely found in technical trading books, acknowledging that the trader's mental state is itself a risk variable requiring active management.

Your results equal your system's expectancy minus your mistakes

Borrowing from poker champion Dan Harrington, Tharp defines the trader's final equation: long-run results equal the sum of your system's edge less the sum of your errors. A mistake, precisely, means not following your own rules. Trading without any plan is therefore one continuous mistake.

Common mistakes include chasing exciting trades, needing to be right (taking profits too fast, refusing losses), risking too much, and repeating errors by blaming external forces. The cost compounds brutally: imagine a system generating 80R per year, but you make two mistakes monthly, each costing roughly 3R. That is 72R in mistakes, nearly erasing the edge. When a normal drawdown hits, the mistake-laden trader abandons a perfectly good system.

This equation elegantly relocates the locus of failure from the market to the trader, aligning with the radical-responsibility ethic that runs through the book. It resonates with deliberate-practice research: experts improve by ruthlessly analyzing their own errors rather than external conditions. Tharp's preliminary estimate that the average mistake costs 2R to 5R is admittedly rough, but the directional insight is powerful. The framework's therapeutic edge is real; treating a bad outcome that followed your rules as a success (worth patting yourself on the back twice) severs the toxic link between correctness and profit. The blind spot: some rule-breaking is adaptive intuition, and rigidly punishing all deviation could suppress genuine expertise.

Take total responsibility, because you attract and create your results

Tharp's deepest and most personal lesson: look to yourself as the source of everything that happens, in markets and in life. He shares his own costliest error, trusting a client who turned out to be a con artist. Rather than sue or blame, he asks what he did to attract that person and how to prevent a recurrence, noting that some fellow victims had been conned three times before by others because they never changed.

His marble-game demonstration drives it home. He has one audience member draw an entire losing streak, then asks who blames that person for their losses. Many raise hands, revealing they learned nothing; they went broke through their own poor position sizing, not the marble-drawer's bad luck.

This closing insight bridges trading and Stoic philosophy, specifically Epictetus's dichotomy of control: focus energy only on what you govern, your own judgments and actions. It also anticipates the growth-mindset research of Carol Dweck, where attributing outcomes to controllable factors drives improvement while blaming external forces breeds helplessness. The marble game is a brilliant experiential proof that people externalize responsibility even when the causal chain is transparently internal. A fair critique: taken to an extreme, radical self-responsibility can shade into blaming victims of genuine fraud or systemic forces. Tharp's point is pragmatic rather than metaphysical, though: assuming responsibility is the only stance that lets you actually change your future behavior.

Analysis

Van Tharp's 1998 classic (revised 2007) is a framework-driven trading manual disguised as a psychological treatise, and that disguise is its genius. Where competitors sell entry signals, Tharp argues that entry is the least important variable in trading, a claim he backs with the audacious random-entry experiment. The book's true architecture rests on three pillars: expectancy (systems as R-multiple distributions), position sizing (the how-much question that drives over 90% of performance variance), and personal psychology (the trader as the ultimate variable). Its enduring value lies in reframing trading from prediction to probability management.

The book is difficult to summarize because it is simultaneously abstract (Holy Grail metaphor, belief examination) and technical (volatility stops, adaptive moving averages, four sizing models). Tharp also structures much of it as anthology, inviting guest experts to explain concepts he does not personally trade, which produces breadth at the cost of depth. The comparison chapter following seven fictional traders through five real 2006 market situations is a pedagogical masterstroke, concretizing how identical setups yield different valid actions depending on the trader's beliefs.

Intellectually, Tharp sits at the intersection of behavioral finance (before it was fashionable), the Kelly Criterion tradition of bet sizing, and neuro-linguistic programming's modeling methodology. His strongest contributions have aged well: expectancy thinking, R-multiples, and anti-martingale sizing are now standard vocabulary. His weakest moments involve uncritical tolerance of astrological and sunspot methods, though his intellectual honesty (publishing data that undermines them) is admirable.

The book's limitation is scope creep into self-help mysticism ("you attract your results") that some empirically minded readers will resist. Yet the core message is rigorous and countercultural: stop trying to be right, build a positive-expectancy edge, size positions to survive worst-case streaks, and treat every loss that followed your rules as a success. For traders drowning in signal-chasing, it remains a durable corrective.

Review Summary

Trade Your Way to Financial Freedom receives mixed reviews. Readers appreciate its insights on risk management, position sizing, and trading psychology. Many find it comprehensive and valuable for developing trading systems. However, some criticize its repetitive content, outdated information, and lack of practical application. The book's emphasis on exits and expectancy is praised, while its writing style and organization are sometimes criticized. Overall, it's considered a solid resource for traders, especially those new to the field, despite its flaws.

People Also Read

FAQ

What's Trade Your Way to Financial Freedom about?

- Self-Discovery Focus: The book emphasizes understanding oneself as the key to trading success. It guides readers through self-assessment to align their trading system with personal beliefs and objectives.

- System Development: It offers a structured approach to creating a trading system, including steps for conceptualizing and evaluating it, drawing on Van K. Tharp's extensive coaching experience.

- Psychological Insights: The book delves into the psychological aspects of trading, addressing biases and mental traps that can hinder performance, and encourages a mindset conducive to success.

Why should I read Trade Your Way to Financial Freedom?

- Comprehensive Framework: The book provides a detailed framework for developing a personalized trading system, suitable for both beginners and experienced traders.

- Expert Insights: Van K. Tharp shares valuable lessons and strategies from his experience coaching traders, helping readers avoid common pitfalls.

- Focus on Psychology: Emphasizing psychological factors, the book helps readers understand the importance of mindset and emotional control for consistent trading results.

What are the key takeaways of Trade Your Way to Financial Freedom?

- You Are the Key: Understanding your beliefs, strengths, and weaknesses is crucial for developing a trading system that works for you.

- Expectancy and Position Sizing: These are critical components of a successful trading strategy, helping traders manage risk and maximize profits.

- Bias Awareness: Recognizing judgmental biases can lead to more informed and rational trading decisions.

What are the best quotes from Trade Your Way to Financial Freedom and what do they mean?

- "You cannot trade the markets...": This quote emphasizes that trading is subjective and influenced by personal beliefs, highlighting the need for alignment with your strategy.

- "Investment success requires internal control...": It underscores the importance of psychological discipline in trading, focusing on managing emotions and decisions.

- "The essence of a good trading system...": This quote stresses the importance of personalization in trading systems, aligning with your personality and objectives for better results.

How does Van K. Tharp define expectancy in Trade Your Way to Financial Freedom?

- Definition of Expectancy: Expectancy is the average impact of each trade relative to the initial risk, helping traders understand potential profitability.

- Calculation of Expectancy: It involves calculating the average profit from winning trades minus the average loss from losing trades, divided by the average loss.

- Significance of Expectancy: A positive expectancy indicates a likely profitable trading system, essential for long-term success.

What is the significance of position sizing in Trade Your Way to Financial Freedom?

- Risk Management: Position sizing is crucial for managing risk, determining how much capital to allocate to each trade.

- Influences Trading Outcomes: Proper position sizing helps withstand losing streaks and allows for larger profits while minimizing losses.

- Tailored to Objectives: Tharp encourages tailoring position sizing strategies to individual goals and risk tolerance for better performance.

How does Trade Your Way to Financial Freedom address psychological factors in trading?

- Understanding Biases: The book explores how psychological biases can distort decision-making, encouraging traders to mitigate their effects.

- Emotional Control: Emphasizing emotional discipline, it teaches traders to manage emotions during loss or volatility.

- Self-Discovery: Focus on self-discovery helps traders understand their psychological strengths and weaknesses, aligning their system with their mental state.

How can I develop a trading system based on the principles in Trade Your Way to Financial Freedom?

- Follow the Steps: Tharp outlines steps for developing a trading system, including self-assessment and defining objectives.

- Test and Evaluate: Emphasizes testing and evaluating your system, analyzing results, and making necessary adjustments.

- Focus on Fit: Ensure the system aligns with your beliefs, strengths, and weaknesses for success and sustainability.

What are some common trading strategies discussed in Trade Your Way to Financial Freedom?

- Trend Following: Involves identifying and trading in the direction of market trends, effective if executed consistently.

- Value Investing: Buying undervalued assets and selling overvalued ones, with insights on determining value effectively.

- Fundamental Analysis: Evaluating supply and demand in the market to make informed decisions based on conditions.

What is the concept of R-multiples in Trade Your Way to Financial Freedom?

- Definition of R-Multiples: Represents the initial risk taken in a trade, providing a consistent performance evaluation method.

- Performance Measurement: Allows traders to assess system effectiveness relative to risk taken, offering a clear performance picture.

- Expectancy Calculation: Expectancy is calculated as the mean of the R-multiple distribution, aiding in understanding average returns.

How does Trade Your Way to Financial Freedom suggest handling losses in trading?

- Cut Losses Short: Emphasizes the importance of cutting losses to preserve capital, crucial for a sustainable strategy.

- Use Protective Stops: Discusses using protective stops to limit potential losses, based on strategy and risk tolerance.

- Mental Preparation: Encourages mental preparation for worst-case scenarios, fostering confidence and resilience.

How can I apply the concepts from Trade Your Way to Financial Freedom to my trading?

- Develop a Trading Plan: Create a comprehensive plan incorporating beliefs, objectives, and strategies from the book.

- Practice Position Sizing: Implement position sizing models to manage risk effectively, adjusting based on equity and trade risks.

- Focus on Psychology: Work on psychological resilience, learning from experiences, and managing emotions for disciplined trading.

About the Author

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.