Key Takeaways

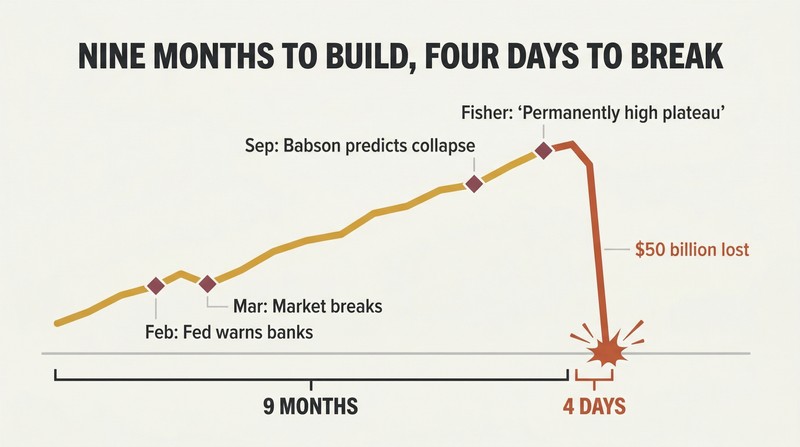

The 1929 crash took nine months to build and four days to detonate

The crash was not a bolt from the blue. Throughout 1929, the Federal Reserve tried and failed to cool speculation. In February, it issued warnings. In March, the market suffered its sharpest break in years — rescued only by a single banker's defiance. Economist Roger Babson warned of a 60-to-80-point collapse; Yale professor Irving Fisher declared stocks had reached "a permanently high plateau." Both men were household names. One was right.

By October, the machinery broke. On Black Thursday, the stock ticker fell four hours behind — traders were gambling on prices from lunch while it was dinnertime. Over four trading days, the Dow lost nearly half its value, erasing $50 billion — roughly half the entire U.S. gross national product. The crash wasn't one moment. It was a slow boil that spilled over.

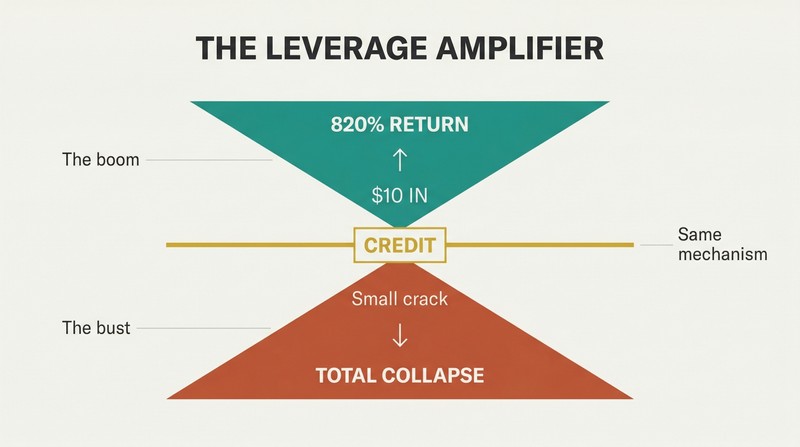

Credit is the miracle drug behind every boom and every bust

The 1920s invented the modern debt economy. In 1919, General Motors pioneered selling cars on installment plans — an assault on the American taboo against personal debt. Sears followed with payment plans for appliances. Wall Street went further: buy stock "on margin," putting up just 10% of the purchase price and borrowing the rest. By the late 1920s, margin loans had swollen from $1 billion to nearly $6 billion.

The math was intoxicating. If a $100 stock doubled, a buyer who put down $10 earned $82 after interest — an 820% return. This only worked if everyone kept faith that the market would keep rising. When confidence cracked, the leverage that amplified gains became a machine for amplifying losses, triggering cascading margin calls that devoured portfolios in hours.

When professors and bootblacks both trade stocks, the top is in

By summer 1929, speculation was a national pastime. Exchange superintendent William Crawford marveled that "the whole world for some reason wanted to be here." Tourists lined up for seats at brokerage customer rooms to watch quotation boards. A bootblack named Pat Bologna had $5,000 — his life savings — in National City Bank stock, based on a tip from its chairman. Groucho Marx bought $27,000 in Goldman Sachs shares on the advice of a fellow actor and Union Carbide stock on a tip from an elevator man at the Ritz.

Astrologer Evangeline Adams dispensed stock picks based on zodiac signs to 100,000 newsletter subscribers. When virtually everyone from Yale professors to vaudeville performers is all-in, there is no one left to buy — only sellers waiting to be made.

The man who saves the market today becomes its scapegoat tomorrow

Charles Mitchell's arc is the book's spine. As chairman of National City Bank — forerunner to Citigroup, responsible for a quarter of all corporate loans — "Sunshine Charlie" single-handedly stopped a market panic in March 1929 by announcing his bank would lend to speculators, directly defying the Federal Reserve. Wall Street celebrated him as a savior on par with J.P. Morgan.

But Senator Carter Glass of Virginia, co-creator of the Federal Reserve, coined a different term: "Mitchellism" — reckless lending that fueled gambling. By October 29, Mitchell was borrowing $12 million — several times his net worth — to personally buy his own bank's stock and prevent its collapse. Within four years he was arrested, publicly humiliated in Senate hearings, and fired. He lost virtually everything.

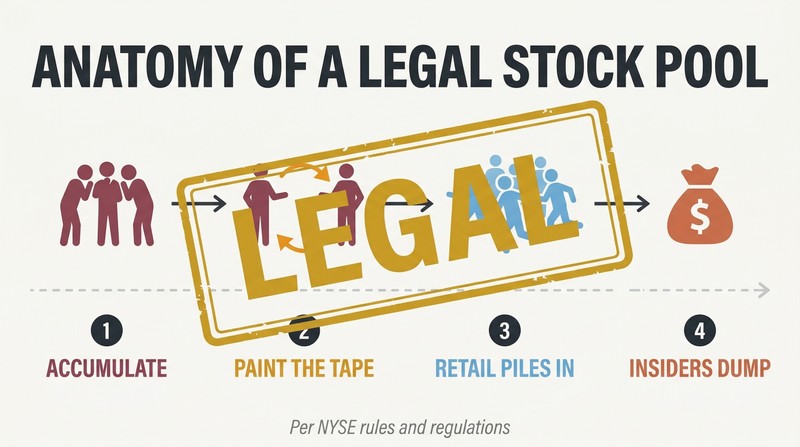

In 1929, insider stock manipulation wasn't illegal — it was standard

Stock pools operated in plain sight. A group of wealthy insiders would quietly accumulate shares, then trade among themselves — "painting the tape" — to create the illusion of momentum. When retail investors piled in, the pool dumped its shares. Michael Meehan, the official RCA specialist on the Exchange floor, ran a pool that netted $4.9 million in just over one week. Participants included auto magnate Walter Chrysler ($500,000) and former GM founder William Durant ($400,000).

The House of Morgan offered discounted stock in its Alleghany Corporation holding company to friends including former President Coolidge, Charles Lindbergh, and Bernard Baruch — an instant profit on paper. All of it was conducted "in accordance with…the rules and regulations of the New York Stock Exchange."

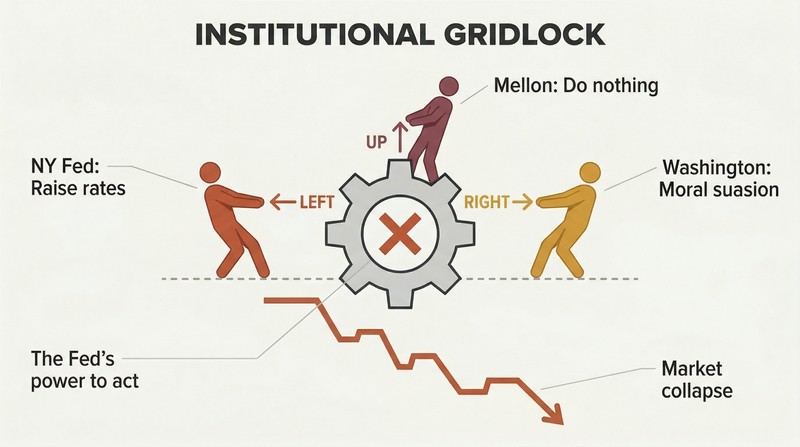

A 15-year-old Federal Reserve was too divided to prevent disaster

The Fed was split between two camps. The New York Fed, closest to Wall Street, wanted to raise interest rates to cool speculation. The Washington board preferred "moral suasion" — politely asking investors to stop gambling. Neither approach worked because neither was applied with conviction. The board rejected New York's rate hike proposal in February 1929, then issued toothless warnings that the market shrugged off within days.

Meanwhile, Treasury Secretary Andrew Mellon — who had resigned from at least 51 corporate directorships to take the job — believed the government should stay out entirely. When the crash came, his advice to President Hoover was chilling: "Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate." The institutional machinery built to prevent catastrophe was paralyzed by ideological gridlock.

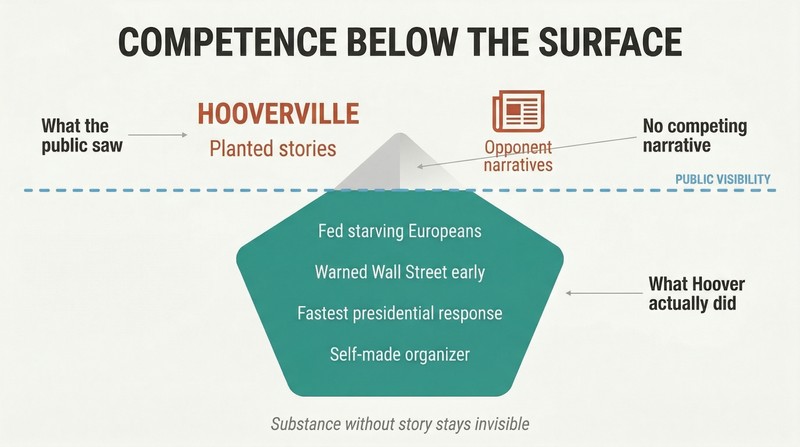

Hoover could engineer solutions but couldn't sell hope to a nation

Herbert Hoover was arguably the most qualified person ever to hold the presidency — self-made mining millionaire, humanitarian hero who fed starving Europeans after World War I, brilliant organizer. But he was a catastrophic communicator who refused to court reporters or rally public emotion. He held press conferences with pre-approved quotes and issued gray, technical statements devoid of empathy.

His opponents exploited the vacuum. Democrat John Raskob secretly hired journalist Charley Michelson to plant damaging stories about Hoover in newspapers nationwide. The coinage "Hooverville" for homeless encampments stuck because Hoover offered no competing narrative. The deeper irony: Hoover actually anticipated the crash, privately warned Wall Street, and moved faster than any previous president to address economic turmoil. None of it mattered because he couldn't make people feel it.

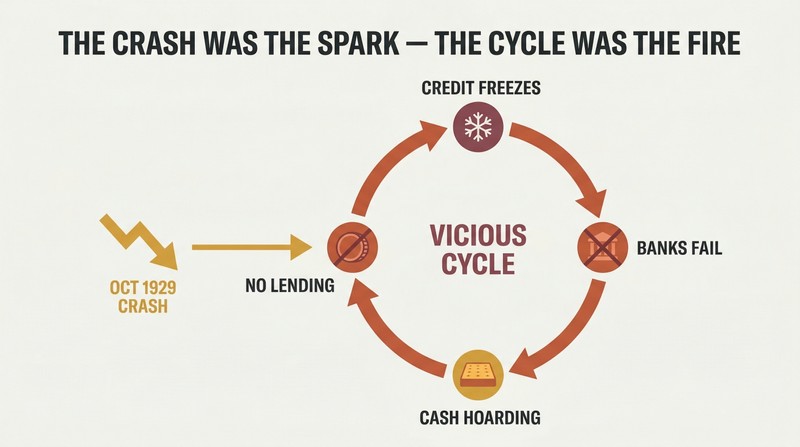

The crash didn't cause the Depression — the credit freeze did

After October 1929, credit vanished. The crash wiped out the collateral backing loans. When nothing seems reliable to lend against, only the foolish lend. Americans pulled cash from savings accounts and stuffed it into mattresses — that really happened. Economist John Maynard Keynes later identified this as the "paradox of thrift": when everyone saves simultaneously, the economy contracts because nobody spends.

The scale of destruction was staggering. By 1933, nearly 11,000 banks had failed permanently. Unemployment hit 23.6%, with thirteen million Americans out of work. The Dow dropped 80% from its 1929 peak. The Smoot-Hawley tariff, which raised duties to nearly 60%, collapsed global trade by 60% within a year. Each problem fed the next in a vicious cycle that lasted a decade.

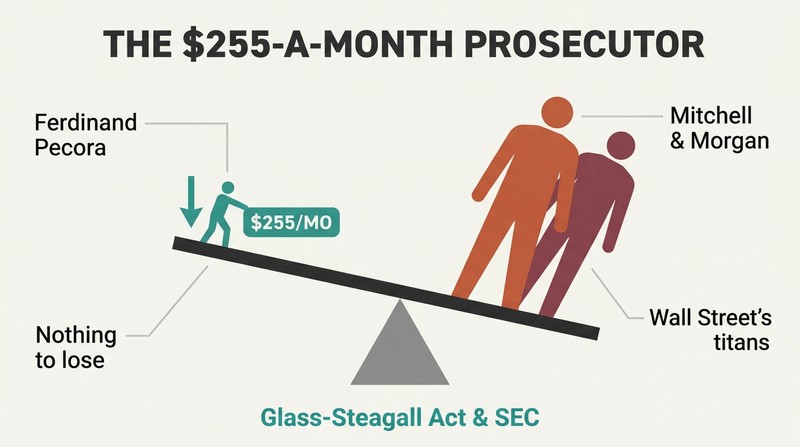

A $255/month prosecutor toppled the titans of Wall Street

Ferdinand Pecora was an unlikely weapon. A Sicilian immigrant's son who couldn't afford to finish college on his first try, Pecora was hired as a last resort by a Senate committee with six weeks left in its session. His salary: $255 a month. He zeroed in on Charles Mitchell, forcing admissions that National City had sold stock to employees at crash prices while executives received forgivable loans, and that Mitchell had sold shares to his wife to evade taxes.

When Pecora turned to J.P. Morgan, he revealed that not a single partner had paid income taxes in 1931 or 1932. Jack Morgan — who privately called Pecora a "dirty little wop" — squirmed as the partnership's secret agreement was read aloud for the first time. The hearings built the political momentum for the Glass-Steagall Act and the creation of the Securities and Exchange Commission.

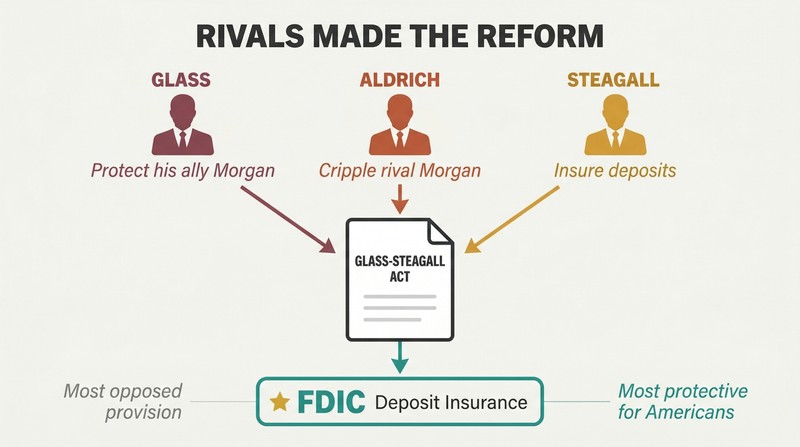

Glass-Steagall passed because Wall Street rivals weaponized reform

The law that separated commercial and investment banking wasn't purely idealistic. Senator Carter Glass initially designed his bill to exempt private firms like J.P. Morgan — whose partner Russell Leffingwell was his close friend and confidant. But Winthrop Aldrich, the Rockefeller-backed new head of Chase, convinced Roosevelt to expand the bill to cover all firms — a calculated move to cripple his rival Morgan.

Even deposit insurance was an accident of politics. Both Glass and Roosevelt opposed government guarantees on bank deposits, fearing moral hazard. Representative Henry Steagall of Alabama insisted on including it. Glass called it dangerous; Roosevelt called it rewarding bad banks. But Steagall had the votes. The provision that most protected ordinary Americans — the FDIC — was the one its namesake sponsors fought hardest against.

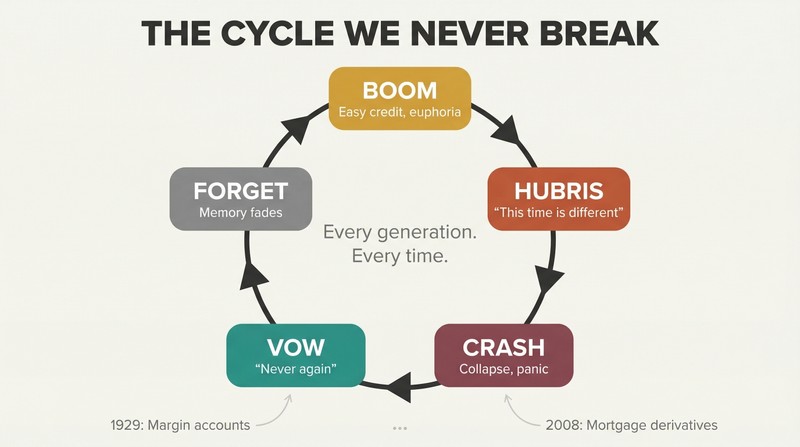

Every generation believes it learned from the last crash — and hasn't

The titans of 1929 were not unusually corrupt or stupid. Thomas Lamont, the Morgan partner who was perhaps the smartest banker in America, wrote President Hoover an 18-page letter on October 19, 1929, assuring him that "corrective action…need not at this time be contemplated." That same day the market crashed 8%. Irving Fisher, one of America's greatest economists, kept insisting stocks were cheap as prices halved.

The specific instruments change — from 1920s margin accounts to 2008 mortgage derivatives — but the psychology is identical. Sorkin's implicit argument is that 1929's cast of characters looks disturbingly like our own era: celebrity CEOs treated as oracles, divided regulators, easy credit, and an unshakable public conviction that this time really is different. The antidote, he argues, is not regulation alone but humility.

Analysis

Sorkin's 1929 represents a distinctive historiographical approach: applying the granular, fly-on-the-wall narrative technique of financial journalism (pioneered in his own Too Big to Fail about the 2008 crisis) to archival material nearly a century old. The result is less an economic history than a psychological portrait — a study of how intelligent, experienced people talk themselves into catastrophe.

The book's most important analytical contribution is restoring moral complexity to a story usually told as a parable of greed punished. Almost nothing the major players did was illegal at the time. Stock pools, insider tips, preferential share allocations, self-dealing between bank affiliates — all were standard practice, conducted within exchange rules. This is far more unsettling than a simple corruption narrative. It suggests that the rules themselves were written by insiders for insiders, and that the boundary between legitimate finance and manipulation is drawn by whoever holds the pen.

Sorkin's access to previously sealed Federal Reserve board minutes adds genuinely new evidence to the historical record, particularly regarding Mitchell's March 1929 intervention. The conventional narrative — that Mitchell recklessly defied the Fed — turns out to be more nuanced: New York Fed governor George Harrison privately encouraged Mitchell's actions, then let him absorb the political backlash alone. This pattern of private complicity and public scapegoating recurs throughout the narrative.

The book implicitly challenges the standard progressive narrative of Glass-Steagall as democratic reform triumphing over oligarchy. Glass himself secretly consulted with Morgan partners while drafting the bill, and the provision most protective of ordinary Americans — deposit insurance — was imposed against the wishes of both the bill's author and President Roosevelt. Reform, Sorkin shows, is as much a product of factional warfare among elites as it is of popular pressure. Winthrop Aldrich weaponized banking reform specifically to damage his rival J.P. Morgan — a reminder that even beneficial regulation can emerge from self-interested motives.

Review Summary

People Also Read

Glossary

Mitchellism

Reckless bank lending to speculatorsTerm coined by Senator Carter Glass to describe Charles Mitchell's practice of extending National City Bank credit to stock speculators in defiance of Federal Reserve policy. Glass used it as shorthand for the broader Wall Street practice of prioritizing speculative profits over the Fed's mission to maintain financial stability.

Moral suasion

Fed's verbal discouragement of speculationThe Federal Reserve Board's 1929 strategy of issuing public statements and advisory warnings to discourage banks from lending money to stock speculators, rather than raising interest rates directly. The approach was a compromise between the Washington board (which opposed rate hikes) and the New York Fed (which favored them). It proved largely ineffective, as markets quickly shrugged off the warnings.

Call money

Short-term loans callable anytimeShort-term loans, often overnight, secured against stocks or bonds, which the lender could demand repayment on ('call') at any moment. New York banks made these loans to brokers, corporations, and foreign banks. Call money rates fluctuated wildly during 1929, spiking to 20% during panics. When rates surged, brokers had to demand more cash from their margin customers or liquidate their positions.

Investment trust

Leveraged pooled investment fundA publicly traded fund that raised money from investors to buy baskets of stocks and bonds, financed with layers of preferred shares and debt. New trusts were sometimes launched to buy shares of existing trusts, piling leverage upon leverage. By the late 1920s, they had proliferated enormously. Investors were drawn by the prestigious names behind them—Morgan, Goldman Sachs—but the structures amplified both gains and losses.

Stock pool

Insider group manipulating share pricesA group of investors who combined resources to covertly buy up shares in a company over weeks, then commenced trades among themselves to artificially inflate the price. When outside investors noticed the rising momentum and bought in, the pool 'pulled the plug' and dumped its shares at a profit. Pools were legal under 1920s exchange rules and involved the biggest names on Wall Street, including J.P. Morgan and National City Bank.

Painting the tape

Fake trading to simulate demandA manipulation technique used within stock pools where members traded shares among themselves to create the appearance of heavy buying activity and rising prices on the ticker tape. The artificial volume attracted outside investors who believed genuine demand was driving the stock higher. The term derives from the paper ticker tape that printed stock prices in brokerage offices across the country.

Babson Break

Market drop from crash predictionThe approximately 3% market plunge on September 5, 1929, triggered by economist Roger Babson's public warning that 'sooner or later a crash is coming which will take in the leading stocks and cause a decline of from 60 to 80 points in the Dow Jones barometer.' Babson had been making similar warnings for two years, but this time his words reached the Dow Jones ticker and spread rapidly through Wall Street.

Big Six

Six bankers pooling crash resourcesThe group of six major bank leaders—Thomas Lamont (J.P. Morgan), Charles Mitchell (National City), Albert Wiggin (Chase), William Potter (Guaranty Trust), Seward Prosser (Bankers Trust), and George Baker Jr. (First National)—who met on Black Thursday, October 24, 1929, at J.P. Morgan's offices and committed $240 million to try to stabilize the market by buying stocks that had no bids.

Wash sale

Sham sale for tax deductionSelling securities to a related party—such as a spouse—to create a tax-deductible loss on paper, with the implicit or explicit intention of buying the shares back later. Charles Mitchell sold 18,300 shares of National City Bank stock to his wife Elizabeth in December 1929 to offset his income and avoid paying taxes. He was later arrested for tax evasion over the transaction but acquitted at criminal trial.

Pecora hearings

Senate investigation exposing Wall StreetThe 1932–1934 Senate Banking and Currency Committee investigation led by chief counsel Ferdinand Pecora, a former New York prosecutor hired for $255 per month. The hearings exposed insider dealings at National City Bank and J.P. Morgan, including tax avoidance by partners, preferential stock offerings to insiders, and manipulation of the RCA stock pool. The revelations built public momentum for the Glass-Steagall Act and the creation of the Securities and Exchange Commission.

FAQ

1. What is 1929: Inside the Greatest Crash in History – and How It Shattered a Nation by Andrew Ross Sorkin about?

- Comprehensive crash narrative: The book provides a detailed, human-centered account of the 1929 stock market crash, exploring the events, personalities, and consequences that shaped the era.

- Focus on key figures: Sorkin profiles influential bankers, politicians, and speculators, examining their motivations and actions before, during, and after the crash.

- Historical context and aftermath: The narrative situates the crash within the broader economic, political, and social environment of the late 1920s and early 1930s, including the Great Depression and regulatory reforms.

- Lessons and legacy: The book reflects on the enduring impact of the crash on American society, financial regulation, and the recurring nature of financial crises.

2. Why should I read 1929: Inside the Greatest Crash in History – and How It Shattered a Nation by Andrew Ross Sorkin?

- Rich historical insight: The book offers a deeply researched, nuanced chronicle that goes beyond statistics to reveal the human stories and institutional dynamics behind the crash.

- Understanding financial crises: Sorkin draws parallels between 1929 and modern crises, providing valuable lessons on market psychology, speculation, and regulatory failures.

- Humanizing history: By focusing on the personal stories and decisions of key actors, the book makes complex financial history accessible and relatable.

- Context for regulation: Readers gain a clearer understanding of how major reforms like the Glass–Steagall Act originated from the events and abuses of this era.

3. Who are the main characters in 1929: Inside the Greatest Crash in History – and How It Shattered a Nation by Andrew Ross Sorkin, and what roles did they play?

- Charles E. Mitchell: President of National City Bank, he aggressively promoted stocks and extended credit, becoming a central figure in both the boom and the blame after the crash.

- Thomas Lamont: Senior partner at J.P. Morgan, he played a key role in market stabilization efforts and advised presidents during the crisis.

- Carter Glass: Senator and architect of the Federal Reserve and Glass–Steagall Act, he led investigations into Wall Street abuses and pushed for banking reforms.

- Jesse Livermore and Richard Whitney: Livermore was a legendary trader who profited from the crash, while Whitney, a NYSE leader, tried to stabilize the market but later fell from grace due to embezzlement.

- Herbert Hoover: U.S. President during the crash, his policies and responses are examined for their impact on the unfolding crisis.

4. What were the main causes of the 1929 stock market crash according to Andrew Ross Sorkin?

- Speculative excess and margin buying: Rampant speculation fueled by easy credit and margin loans inflated stock prices far beyond their real value.

- Lax regulation and banking practices: Banks extended risky loans and blurred the lines between commercial and investment banking, creating systemic vulnerabilities.

- Economic imbalances: The consumer economy was built on debt, with uneven prosperity and underlying weaknesses in agriculture and industry.

- Federal Reserve’s limited intervention: The Fed’s inconsistent policies and internal conflicts failed to curb speculation or provide effective crisis management.

5. How did Charles Mitchell and National City Bank contribute to the 1929 crash, as described by Andrew Ross Sorkin?

- Aggressive market intervention: Mitchell used National City Bank’s resources to buy back its own stock and prop up prices, risking the bank’s solvency.

- Promotion of margin buying: The bank extended credit to ordinary Americans, making stock speculation accessible and fueling the bubble.

- Public confidence and controversy: Mitchell’s actions made him both a hero and a target, drawing criticism for encouraging risky speculation.

- Banking innovation and risk: National City’s practices exemplified the era’s financial innovation, but also its recklessness.

6. What role did the Federal Reserve and government officials play during the 1929 crash and its aftermath in Sorkin’s account?

- Federal Reserve’s inconsistent response: The Fed tried to tighten credit but failed to control speculative lending and hesitated to ease conditions during the crash.

- Internal conflicts: Disagreements between the New York Fed and the Washington board hampered decisive action.

- Government’s cautious approach: President Hoover downplayed the crisis and preferred voluntary cooperation over direct intervention.

- Political tensions: Figures like Carter Glass blamed bankers and pushed for reforms, while others resisted regulatory changes.

7. What were investment trusts and stock pools, and how did they contribute to the crash according to 1929 by Andrew Ross Sorkin?

- Leverage and speculation: Investment trusts pooled investor money to buy stocks, often using multiple layers of debt, amplifying risk and market leverage.

- Market manipulation: Stock pools involved coordinated buying and selling to create artificial demand and manipulate prices, attracting unwary investors.

- Regulatory gaps: These practices were legal but deceptive, contributing to inflated stock prices and market instability.

- Participation by major institutions: Leading banks and financiers, including National City and J.P. Morgan, were involved in these schemes.

8. What was the significance of the Pecora hearings in 1929: Inside the Greatest Crash in History – and How It Shattered a Nation?

- Senate investigation into Wall Street: Led by Ferdinand Pecora, the hearings exposed widespread abuses, conflicts of interest, and unethical practices among bankers.

- Public revelation of misconduct: Testimonies revealed secret loans, insider trading, and excessive executive compensation, shocking the public.

- Catalyst for reform: The hearings fueled demands for regulatory changes, including the Glass–Steagall Act.

- Symbol of accountability: Pecora’s relentless questioning marked a new era of government oversight and diminished Wall Street’s unchecked power.

9. What is the Glass–Steagall Act, and how did it change the banking industry according to Andrew Ross Sorkin?

- Separation of banking functions: The Act mandated the division of commercial banking from investment banking to reduce conflicts of interest and speculative risks.

- Creation of deposit insurance: It introduced federal insurance for bank deposits, restoring public confidence in the banking system.

- Response to public outrage: The law directly addressed the abuses revealed by the crash and the Pecora hearings.

- Long-term impact: Glass–Steagall fundamentally altered Wall Street’s structure and shaped American finance for decades.

10. How did the 1929 crash impact American society, politics, and culture according to 1929 by Andrew Ross Sorkin?

- Economic devastation: The crash triggered widespread bank failures, unemployment, and hardship, leading to the Great Depression.

- Political fallout: The crisis undermined the Hoover administration and spurred the rise of Roosevelt’s New Deal and major regulatory reforms.

- Cultural and psychological effects: Public attitudes toward wealth, risk, and capitalism shifted, inspiring literature and calls for change.

- Urban-rural divide: Prosperity was uneven, with rural areas suffering more, deepening social tensions.

11. What are the key lessons and enduring themes from 1929: Inside the Greatest Crash in History – and How It Shattered a Nation by Andrew Ross Sorkin?

- Human nature and market cycles: Booms and busts are driven by psychology—greed, fear, optimism, and herd behavior—which are perennial and hard to control.

- Limits of regulation and foresight: Systemic vulnerabilities and short-term incentives often overwhelm regulatory efforts and prudent judgment.

- Importance of humility: Sorkin argues that humility is the antidote to “irrational exuberance,” as no system is foolproof and history often repeats.

- Legacy of reform and resilience: The crash led to significant reforms and demonstrated the resilience of American society and capitalism.

12. What are the most notable quotes from 1929: Inside the Greatest Crash in History – and How It Shattered a Nation by Andrew Ross Sorkin, and what do they mean?

- On experience and learning: “The ordinary human being does not live long enough to draw any substantial benefit from his own experience. And no one, it seems, can benefit by the experiences of others.” —Albert Einstein, highlighting the challenge of learning from history.

- On bankruptcy: Ernest Hemingway’s line, “How did you go bankrupt? Two ways. Gradually, then suddenly,” encapsulates how economic confidence and crises unfold.

- On speculation: Carter Glass’s statement, “Stock trading is gambling wit matched against gambling wit. It does not contribute a thing to the happiness or the welfare of the country,” reflects the era’s critical view of speculation.

- On debt and optimism: Debt is described as “a powerfully optimistic force,” bringing future wealth into the present but also fueling risk and eventual collapse.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.