Key Takeaways

Manage risk before profit: know your exit before you enter

The masters obsess over losing, not winning. All four traders (Minervini, Ryan, Zanger, and Ritchie II) converge on one non-negotiable: define your stop loss before buying a single share. Minervini caps total-equity risk per trade between 1.25% and 2.5%, and treats a 10% drop as his absolute "uncle point" he rarely reaches. Ryan risks a maximum of 1% of equity per position. Zanger keeps individual stock stops as tight as 2-3%, having learned the hard way.

Small losses are survivable; big ones are fatal. Minervini spent six losing years until he decided the goal was to make money, not be right. Once he swallowed his ego and cut losses fast, consistency arrived. The math is unforgiving: a large loss compounds against you geometrically, requiring outsized gains just to break even.

What's striking is how this inverts the amateur's instinct to fixate on upside. It echoes Daniel Kahneman's prospect theory: humans feel losses roughly twice as intensely as equivalent gains, which paradoxically makes traders hold losers too long to avoid "realizing" the pain. The masters weaponize discipline against this bias by predetermining exits when emotion is absent. The parallel to poker is exact: professionals fold most hands, protecting their stack for premium spots. One nuance worth flagging: tight stops demand precise timing, so beginners often get whipsawed out of good trades. The skill is not just cutting losses but buying at low-risk entry points where stops rarely trigger.

Chase relative strength, not cheap prices or comfortable stories

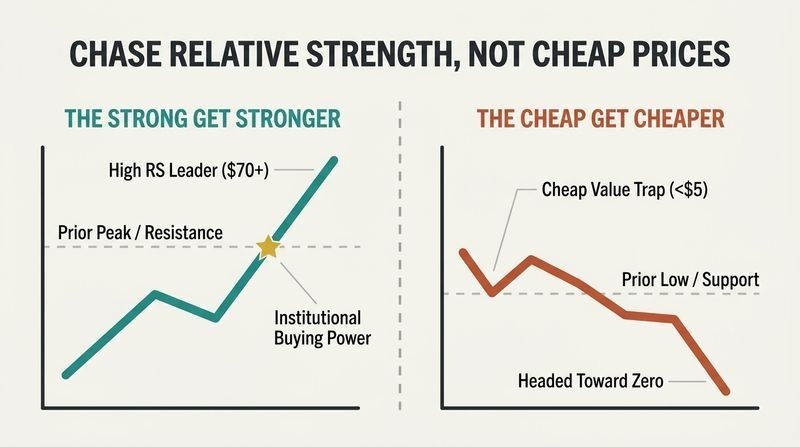

Buy the strongest stocks near new highs. Momentum trading means owning stocks already outperforming the market, measured by relative strength (RS), a ranking of a stock's price performance versus all others. Minervini screens for high RS, high alpha, and low volatility. The counterintuitive part: the best setups often look scariest, having already run up sharply and appearing expensive. Ritchie II says the higher the RS, the better.

Cheap stocks are cheap for a reason. Minervini notes the biggest historical winners began their major advances above $30 a share, and a $1 stock is far more likely to hit zero than double. He prefers fewer shares of higher-priced names above $20-30, which attract institutional buying. Zanger rarely touches stocks under $70. Low price signals weakness, not a bargain.

This directly contradicts value investing orthodoxy (Graham, Buffett), and the tension is instructive rather than contradictory: these are different games on different time horizons. Momentum is among the most robustly documented anomalies in finance, validated by Jegadeesh and Titman's 1993 research and later by Fama and French, who reluctantly added it to their factor models. Winners tend to keep winning over 3-12 month windows. The psychological difficulty is real: buying at 52-week highs feels irrational, triggering the same fear that makes people sell too early. The masters essentially outsource their judgment to the market's collective verdict, trusting institutional money flows over their own opinions or a company's narrative.

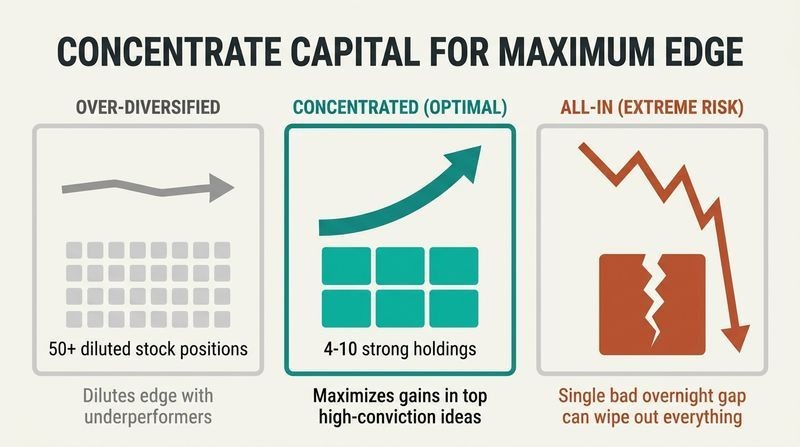

Concentrate capital in a few winners; diversification dilutes your edge

Bet big when you have conviction. Minervini argues that if you have a genuine edge, spreading money across dozens of names dilutes rather than protects you. He concentrates up to 25% of his portfolio in a single position, citing the Kelly formula and "Optimal f" (mathematical methods for sizing bets to maximize long-term growth) as justification for 25% being optimal for a 2:1 trader. Ryan runs roughly 10 positions at 10% each. Ritchie II argues owning 50 stocks guarantees a large share of underperformers, since only a small fraction of stocks truly outperform at any time.

But never risk everything on one name. Minervini nearly bought a stock that gapped down 80% overnight. Zanger went "all in" once and was nearly wiped out when Barron's exposed his stock as a fraud, sending it from $27 to $6.

This is a sharp rebuke to the diversification gospel taught in every finance textbook. Modern Portfolio Theory optimizes for risk-adjusted returns across uncorrelated assets, but that framework assumes you have no edge and cannot predict winners. The masters claim precisely the opposite. There is genuine tension here: concentration amplifies both skill and luck, and behavioral finance warns of overconfidence bias, where traders mistake a hot streak for durable skill. The saving grace is their obsessive downside management. A 25% position with a 5% stop still risks only 1.25% of equity. Concentration without ruthless stops would be reckless; concentration paired with stops is calculated aggression.

Scale position size up on wins, down on losses

Trade your biggest when you're trading your best. Rather than betting the same size always, the masters expand exposure after success and shrink it after failure. Minervini calls this ensuring you trade largest when winning and smallest when losing, which mechanically produces big gains and avoids big drawdowns. Ritchie II keeps portfolio risk near 100 basis points during losing streaks, bumping to 200-300 as traction returns. Zanger drops to a single 1% position in choppy conditions just to "stay in tune."

Pyramid on the heels of profit. Ritchie II compares it to home run hitters: you swing harder only after consistently making solid contact. New traders should wait until their account is up 25-50% before increasing size. Confidence and capital both accumulate one successful trade at a time.

This is essentially anti-martingale, the opposite of the doubling-down gambler's ruin that destroys accounts. It resembles a Bayesian updating process: each result revises your estimate of whether current market conditions favor your strategy, and you bet accordingly. There is a feedback-loop elegance here, since the market itself signals when to press. A subtle risk: markets can shift regime abruptly, so a streak of wins near a market top can lure a trader into maximum size just before a reversal. Zanger addresses this by deliberately not increasing size as the year progresses, reasoning that an extended market grows more vulnerable precisely as his account swells.

Let stocks, not market forecasts, dictate when you invest

Your own trades are the best market indicator. Instead of predicting market direction, the masters read it through their positions. Minervini takes small "pilot buys" or "toe-in-the-water" positions coming out of a correction; if they work and a second wave of stocks sets up, he steps on the gas. If his buys stall or stop out, he retreats. He claims his best market calls come precisely when he ignores the indexes and focuses on individual stocks.

Stocks lead the market. In 1990, healthcare names like Amgen barely dipped during a severe bear market, then exploded in the following bull run. Ritchie II flips the conventional top-down approach entirely: he hunts strong stocks first, then notices which groups and themes emerge, rather than starting with the market or sector.

This bottom-up empiricism is a quiet epistemological stance: distrust forecasts, trust observable behavior. It parallels the scientific method's preference for data over theory, and echoes George Soros's reflexivity, where price action itself reveals underlying reality. The approach also sidesteps a well-documented failure: market timing forecasts by economists and strategists are notoriously unreliable (Philip Tetlock's expert-prediction studies show pundits barely beat chance). By letting positions self-select through stops and follow-through, the masters build a real-time, self-correcting sensor rather than a prediction. The limitation: this works for active traders watching daily, less so for passive investors who cannot monitor and adjust continuously.

Volume is the fingerprint of institutional buying

Big moves need big money. Volume reveals whether mutual funds and hedge funds, not retail traders, are powering a stock. Ryan calls volume the lifeblood of a stock and wants breakout volume at least 25% above average, ideally 100-200% higher, sustained for three or more days. Minervini looks for volume eclipsing the 50-day average. Zanger built a custom audio program that plays a "coconut" sound when bids are hit and a "hammer" when asks are hit, letting him hear accumulation or distribution.

The rocket analogy. Ryan describes a breakout like a rocket launch: it needs enormous fuel (volume) to clear the launchpad, but once in orbit, it can drift higher on lighter volume. A stock making new highs on shrinking volume signals fading demand, though it is not automatically a sell.

Volume analysis rests on a sound premise: large institutions cannot disguise their footprints because moving billions requires days of accumulation. This is information leakage made visible. The rise of dark pools (private exchanges where big trades hide) prompted worry that this signal degraded, but the masters note all volume still tallies by day's end. What's worth questioning is precision: high-frequency trading and algorithmic activity now generate enormous volume that reflects no directional conviction, potentially muddying the read. Zanger's synesthetic "sound of the market" tool is a fascinating cognitive hack, offloading pattern recognition to the auditory system, which processes rhythm and anomaly faster than the eye scans numbers.

Wait for volatility to contract before the explosive breakout

Tightness precedes big moves. Minervini's signature setup is the Volatility Contraction Pattern (VCP): as a stock consolidates, its price swings grow progressively smaller from left to right while volume dries up. This "selling vacuum" means supply has been exhausted, and when demand returns, price explodes through a pivot point (the precise buy level at the edge of the consolidation). Ryan looks for a week or more of very quiet, tight price action before buying.

Only enter as the stock moves your way. None of the masters buy falling knives or bottom-fish. Minervini refuses to buy any stock below its declining 200-day moving average. He uses a party metaphor: he never wants to be first to arrive; he wants confirmation the party is already going before joining. Buy strength turning up, never weakness still falling.

The VCP formalizes an intuition Jesse Livermore voiced a century ago as the "line of least resistance." Physically, it resembles a coiled spring or the pressure buildup before a geological fault slips: energy accumulates invisibly, then releases violently. The volume dry-up is the key tell, indicating sellers have capitulated and float is locked up. One honest limitation the masters acknowledge: breakouts fail roughly half the time, even in strong names. There is no pattern that eliminates false signals, which is exactly why the entire edifice rests on tight stops. The pattern improves probability; risk management handles the inevitable misses.

Sell into strength; never let a good gain become a loss

Take profits while the stock is still rising. Counterintuitively, the masters sell into advancing prices rather than waiting for weakness. Minervini's "sell half rule" is a psychological win-win: if you're indecisive, sell half, then you're happy whether it rises (you kept some) or falls (you locked some in). He moves his stop to breakeven once a stock advances a multiple of his risk, refusing to let a decent profit turn negative.

Winners held longer than losers. Ritchie II's average losing trade lasts two to three days; his average winner runs eight to nine. This asymmetry, cutting losers fast and riding winners, is the engine of profitability. Yet none chase the exact top. Zanger warns that price targets are like shooting a winning racehorse at the starting gate, since the real winners run far past any average-based target.

The core insight is expectancy: profitability equals (win rate times average win) minus (loss rate times average loss). By slashing losers to 2-3 days and letting winners run 8-9, the masters engineer a favorable ratio even with a modest win rate. Minervini explicitly builds in failure, prioritizing the loss-to-gain ratio over batting average, a mindset borrowed from professional gambling and options market-making. The "sell half" rule is clever behavioral engineering, neutralizing regret in both directions. The tension the masters navigate daily: selling into strength caps your biggest winners, yet those rare monster runs (Zanger's few dozen movers made most of his fortune) are where life-changing money lives.

Never average down; adding to losers is how accounts blow up

Rotate capital from losers to winners. Every master forbids adding to a losing position. Ryan calls losing positions a cancer that must be cut out, not fed, and insists equity constantly rotate from losers into winners. Minervini names adding to losers the number one reason traders blow up. The only exception: adding on a pullback while building a position near the original entry, but always as the stock turns back up.

Buying more feels right but is backward. Ritchie II observes that when you own a stock at a lower price, buying more at a higher price feels wrong ("I should have bought cheaper"). But if he only added when prices fell back to his entry, he would have loaded up on his worst trades and missed his best. The pyramid goes up, never down.

Averaging down feels virtuous because it lowers your cost basis and aligns with "buy low." But it is precisely the mechanism behind catastrophic blowups, from Nick Leeson sinking Barings Bank to Long-Term Capital Management. The behavioral culprit is the sunk-cost fallacy fused with loss aversion: doubling down converts an admission of error into a bet on being right eventually. Ritchie II's reframe is psychologically astute, exposing how our backward-looking, anchoring instinct sabotages forward decisions. The counterpoint from value investing is that a lower price on a fundamentally sound asset is a better deal, but that logic assumes you can value the asset independently of price, which momentum traders explicitly refuse to do.

Study your own trades as obsessively as you study charts

Post-analysis turned careers around. Minervini credits reviewing past trades as what transformed his early results; he marks entries and exits on charts and hunts for common denominators in his mistakes. Ryan screenshots every purchase with his reasoning and market conditions, then dissects where he was right and wrong. Ritchie II logs every trade by strategy, enabling him to run drawdown simulations and distinguish normal losing streaks from a genuinely broken approach.

Most traders avoid the mirror. Ritchie II notes struggling traders won't examine their results because it's painful to confront poor performance. But the data reveals patterns of strength and weakness invisible any other way. His father's line captures it: knowledge and talent matter, but discipline gets the job done. The truth about your trading lives in your records.

This is the trading equivalent of deliberate practice, the concept Anders Ericsson identified as separating elite performers from mere veterans: not repetition, but repetition with rigorous feedback loops targeting specific weaknesses. Most traders, like most amateurs in any field, plateau because they practice without honest self-assessment. The avoidance Ritchie II describes is a documented phenomenon: people systematically dodge information that threatens self-image (the "ostrich effect" in behavioral economics). Building a personal trading database converts vague intuition into falsifiable hypotheses, letting a trader ask whether a drawdown exceeds statistical norms (signaling a real problem) or fits expected variance (signaling patience). It is arguably the least glamorous and most decisive edge discussed.

The small investor's speedboat beats the institution's cruise ship

The game is not rigged against you. Minervini flatly rejects the excuse that markets favor the big players. The individual investor holds a structural advantage: liquidity and speed. A hedge fund managing billions must accumulate and unload positions over days or weeks, like turning a cruise ship, while the individual maneuvers like a speedboat, entering and exiting in seconds. Ryan calls "rigged" an excuse for underperformance and a sign someone has given up.

Start small and compound. All four insist you can get rich starting with a modest account. Zanger turned $10,775 into $18 million in 18 months after rebuilding from selling his car to cover a $225 debt. Ritchie II grew a small account over 1,000% in five years. Low commissions and abundant information have leveled the field.

There is real substance to the nimbleness argument. Academic studies confirm that fund performance often decays as assets under management balloon, because large size incurs market-impact costs (your own buying moves the price against you) and forces managers into more liquid, efficiently-priced large caps. The masters exploit small, inefficiently-priced names institutions cannot touch. That said, the "not rigged" claim deserves nuance the masters partly concede elsewhere: high-frequency front-running and market-maker stop-hunting are real frictions. The honest synthesis is that markets are neither rigged nor perfectly fair, but the individual's agility genuinely offsets the institution's information and capital advantages, provided the individual actually does the work.

Commit to one strategy; talent matters less than disciplined repetition

Style drift kills more traders than bad strategies. Minervini compares committing to a strategy to a marriage: constant cheating with new methods dooms it. He estimates the learning curve at two to five years and insists most traders fail even when handed a winning system because they can't endure the difficult stretches and abandon it. His approach rests on the timeless law of supply and demand, which he says won't break unless gravity does.

Nature versus nurture. The masters largely side with nurture. Ritchie II admits no special talent beyond good memory and discipline. Ryan lists the required traits: discipline, focus, humility, and willingness to take risk. Minervini's final word borrows a phrase: it's not the gun, it's the gunner. Ritchie II boils success down to three Ms: a market, a method, and myself, all working together.

The commitment thesis aligns with the 10,000-hour framing popularized by Gladwell, though Ericsson's original research stressed quality of practice over raw hours. What the masters add is the emotional endurance dimension often omitted from skill-acquisition literature: the hardest part is not learning the method but surviving the psychological valley where a sound strategy temporarily underperforms. This is where most quit, mistaking normal variance for failure, the exact error Ritchie II's trade-tracking guards against. The "three Ms" framework is a useful reminder that self-mastery is co-equal with market knowledge and technique. Notably, Ritchie II grounds his in faith, illustrating how a stable identity outside trading paradoxically grants the freedom to fail and thus to succeed.

Analysis

Momentum Masters is an anthology interview, not a thesis-driven treatise, which is both its strength and its challenge to summarize. Four elite traders (Minervini, Ryan, Zanger, and Ritchie II) answer 130 reader-submitted questions in roundtable format, so insights arrive scattered across ten topical sections rather than built into an argument. The value lies in triangulation: where four independent operators with different styles (Ryan and Minervini favor small and mid caps, Zanger prefers large and mega caps, Ritchie II runs a multi-strategy book) converge, you glimpse durable principles rather than idiosyncratic quirks.

The deep structure beneath the surface disagreements is a coherent philosophy of asymmetric risk. Every masters' answer, whatever the topic, reduces to one governing idea: control the downside ruthlessly and the upside handles itself. Position sizing, stop placement, scaling up on wins, never averaging down, selling into strength, and holding winners longer than losers are all expressions of engineering positive expectancy. The traders essentially treat trading as a probabilistic craft, akin to professional poker or options market-making, where the goal is not being right often but being large when right and small when wrong.

The book's intellectual honesty is notable. The masters repeatedly concede that breakouts fail half the time, that they cannot pick tops, and that they endured years of losses. This candor separates it from the survivorship-biased guru genre. Its limitations: it offers little for passive or fundamental investors, assumes daily market engagement, and its momentum edge, while academically validated by Jegadeesh, Titman, Fama, and French, is crowded and subject to sharp reversals that can devastate the undisciplined. The recurring meta-lesson, voiced most clearly by Minervini and Ritchie II, is that psychology and self-knowledge, not secret setups, ultimately determine outcomes. Discipline, as Ritchie II's father put it, gets the job done.

People Also Read

FAQ

1. What is "Momentum Masters: A Roundtable Interview with Super Traders" by Mark Minervini about?

- Roundtable Q&A with Top Traders: The book features 130 real-world trading questions answered in a roundtable format by four renowned traders: Mark Minervini, David Ryan, Dan Zanger, and Mark Ritchie II.

- Focus on Momentum Trading: It centers on momentum stock trading, covering everything from stock selection and technical analysis to risk management and trading psychology.

- No Biographical Filler: The book is strictly Q&A, with no lengthy biographies or storytelling—just actionable trading insights.

- Comparative Insights: The format allows readers to compare and contrast the approaches of each trader on every topic, highlighting both differences and shared principles.

2. Why should I read "Momentum Masters" by Mark Minervini and what makes it unique?

- Direct Answers from Super Traders: You get unfiltered, practical advice from four traders with proven, audited track records of extraordinary returns.

- Real Questions from Real Traders: All questions were submitted by actual traders, ensuring the content addresses genuine challenges and knowledge gaps.

- Side-by-Side Comparison: The roundtable format lets you see how top traders think differently (and similarly) about the same issues, helping you refine your own approach.

- No Fluff, All Substance: The book is designed for readers who want actionable trading strategies and principles, not entertainment or motivational filler.

3. What are the key takeaways from "Momentum Masters" by Mark Minervini?

- Discipline and Risk Management: Cutting losses quickly, never averaging down, and always trading with a plan are universal rules among the masters.

- Concentration Over Diversification: To achieve outsized returns, focus on your best ideas rather than spreading yourself thin across many stocks.

- Technical and Fundamental Synergy: While technical analysis is primary, strong fundamentals (especially earnings and sales growth) are crucial for big winners.

- Adaptability and Self-Analysis: Continual post-analysis, learning from mistakes, and adapting to market conditions are essential for long-term success.

4. Who are the "Momentum Masters" featured in Mark Minervini's book, and what are their credentials?

- Mark Minervini: U.S. Investing Champion, author, and creator of the SEPA® methodology, with a 36,000% return over five years.

- David Ryan: Protégé of William O’Neil, three-time U.S. Investing Champion, and former institutional money manager.

- Dan Zanger: Turned $10,775 into $18 million in 18 months, recognized for his expertise in chart patterns and technical analysis.

- Mark Ritchie II: Achieved a 100% return in less than six months, with over 1,000% total return since 2010, and known for his disciplined, data-driven approach.

5. How do the "Momentum Masters" in Mark Minervini's book select stocks with big potential?

- Relative Strength and Price Action: Minervini and Ritchie II focus on stocks with high relative strength and strong price trends.

- Growth and Fundamentals: Ryan emphasizes growth stocks with strong earnings and sales profiles, using tools like MarketSmith and IBD.

- Volume and Liquidity: Zanger prefers stocks with high daily volume and clear, powerful chart patterns, avoiding thinly traded names for large positions.

- Avoiding Bottom-Fishing: All agree that buying stocks in uptrends and avoiding attempts to catch falling knives is key to success.

6. What is the Volatility Contraction Pattern (VCP) and why is it important in "Momentum Masters" by Mark Minervini?

- Signature Setup: The VCP is Minervini’s core technical setup, identifying a series of tightening price ranges (volatility contractions) within a base.

- Line of Least Resistance: It signals that supply is drying up, setting the stage for an explosive breakout when demand overwhelms remaining sellers.

- Low-Risk Entry: The VCP allows traders to enter with tight stops and high reward-to-risk ratios, maximizing gains while minimizing losses.

- Universally Applicable: While Minervini popularized it, the other masters also look for similar contraction and tightness before major moves.

7. How do the "Momentum Masters" in Mark Minervini's book approach position sizing and portfolio concentration?

- Concentration for Big Gains: Minervini and Ryan advocate concentrating capital in your best ideas, sometimes up to 25% of the portfolio in a single stock.

- Dynamic Sizing: Position size is adjusted based on market conditions, recent trading success, and the quality of the setup.

- Risk Per Trade: Most masters risk 1% or less of total equity per trade, scaling up only when trades are working.

- Avoiding Over-Diversification: Broad diversification is seen as diluting performance rather than protecting against risk.

8. What are the main risk management principles in "Momentum Masters" by Mark Minervini?

- Always Use Stops: Every trade has a predetermined exit point, whether based on technical levels or a fixed percentage loss.

- Keep Losses Small: Never let a loss get out of control; small, frequent losses are preferable to rare, large ones.

- No Averaging Down: Adding to losing positions is universally discouraged, as it compounds mistakes and risk.

- Position Sizing and Sleep Factor: Trade sizes are kept within levels that allow the trader to sleep well at night, avoiding emotional decision-making.

9. How do the "Momentum Masters" in Mark Minervini's book manage trades after entry, including scaling in/out and handling winners?

- Scaling In and Out: Most start with partial positions and add as the trade works, scaling out into strength or if the stock shows weakness.

- Profit Protection: Once a trade is profitable, stops are moved up to protect gains, often to breakeven or higher.

- Letting Winners Run: The best trades are held as long as they continue to act well, but profits are taken into strength to avoid round-tripping gains.

- No Fixed Targets: While some use multiples of risk as guidelines, most rely on price action and technical signals to exit.

10. What psychological and behavioral advice do the "Momentum Masters" in Mark Minervini's book offer for trading success?

- Discipline is Non-Negotiable: Sticking to your plan and rules, especially in cutting losses, is the foundation of long-term success.

- Self-Analysis and Adaptation: Regular post-analysis of trades helps identify strengths and weaknesses, leading to continuous improvement.

- Managing Emotions: Guarding against overtrading, revenge trading, and style drift is crucial; trade smaller when confidence is low.

- Patience and Commitment: Success takes years of practice, learning from mistakes, and unwavering commitment to your chosen strategy.

11. What are the most important fundamental and technical criteria for stock selection in "Momentum Masters" by Mark Minervini?

- Earnings and Sales Growth: Accelerating quarterly earnings and sales are key drivers of big stock moves.

- Relative Strength and Uptrends: Stocks should be in strong uptrends, outperforming the market and their peers.

- Volume Confirmation: Breakouts should be accompanied by above-average volume, signaling institutional buying.

- Avoiding Low-Quality Setups: Stocks with poor fundamentals, low liquidity, or extended from bases are generally avoided.

12. What are the top five trading rules or best quotes from "Momentum Masters" by Mark Minervini and the other masters, and what do they mean?

- "Think risk first." Always know your exit before you enter a trade; protecting capital is more important than chasing gains.

- "Never average down." Adding to losers is the fastest way to blow up an account; cut losses quickly instead.

- "Move money from losers to winners." Rotate capital out of underperformers and into stocks that are working.

- "Let the market guide you." Don’t impose your opinions; let price action and your criteria dictate your trades.

- "Study your results regularly." Post-analysis is essential for identifying what works and what doesn’t, leading to continuous improvement.

These 12 questions and answers cover the core concepts, strategies, and philosophies found in "Momentum Masters: A Roundtable Interview with Super Traders" by Mark Minervini, providing a comprehensive overview for both new and experienced traders.

Download PDF

Download EPUB

.epub digital book format is ideal for reading ebooks on phones, tablets, and e-readers.